|

|

|

|

|||||

|

|

|

Shares of Corcept Therapeutics CORT were up 13.7% on Jan. 22, after the company announced that the phase III ROSELLA study, which evaluated its pipeline candidate, relacorilant in combination with nab-paclitaxel for treating patients with platinum-resistant ovarian cancer, met its overall survival (OS) primary endpoint.

Data from the ROSELLA study showed that treatment with relacorilant plus nab-paclitaxel chemotherapy led to a 35% reduction in the risk of death compared to nab-paclitaxel alone in the given patient population.

Patients who were treated with relacorilant plus nab-paclitaxel achieved a median OS of 16 months compared to 11.9 months in patients who received nab-paclitaxel alone. The combo of relacorilant plus nab-paclitaxel was generally well tolerated, with a safety profile similar to what is already known. Relacorilant delivered clinical benefits without increasing the safety burden for patients treated with it.

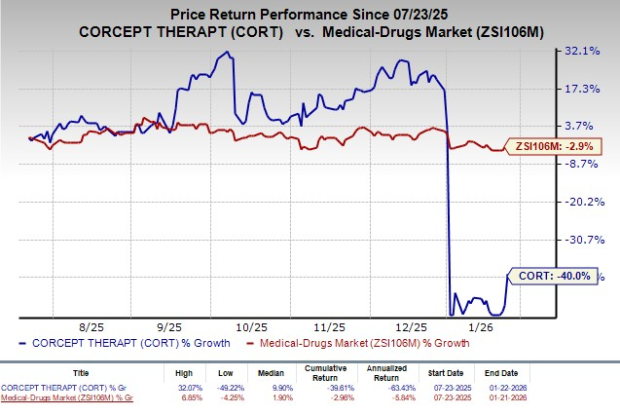

In the past six months, shares of Corcept have plunged 40% compared with the industry’s decline of 2.9%.

Last April, Corcept announced that the ROSELLA study met its primary endpoint of improved progression-free survival, as assessed by a blinded independent central review (PFS-BICR). Per management, data from the ROSELLA study suggested that the combo of relacorilant plus nab-paclitaxel has the potential to become a new standard of care for patients with platinum-resistant ovarian cancer.

Both the dual primary endpoints of PFS and OS were achieved without the need for biomarker selection or added safety burden.

The FDA accepted the new drug application (“NDA”) seeking approval for relacorilant in combination with nab-paclitaxel for treating patients with platinum-resistant ovarian cancer in September 2025. A decision from the regulatory body is expected on July 11, 2026.

Corcept recently submitted a marketing authorization application to the European Medicines Agency, seeking approval for relacorilant to treat patients with platinum-resistant ovarian cancer. A decision in Europe is expected later in 2026.

Corcept is also evaluating relacorilant plus nab-paclitaxel and Roche’s RHHBY Avastin (bevacizumab) in the phase II BELLA study for treating patients with platinum-resistant ovarian cancer.

Previously, management stated that the BELLA study would help in understanding whether combining relacorilant with two medicines — nab-paclitaxel and RHHBY’s Avastin — offers patients an additional treatment option or not.

Relacorilant is also being studied for treating other solid tumors, including platinum-sensitive ovarian, endometrial, cervical, pancreatic and prostate cancers.

Corcept recently suffered a major setback when the FDA issued a complete response letter (“CRL”) to the NDA seeking approval for relacorilant to treat patients with hypercortisolism (Cushing’s syndrome). Shares of the company tanked on this news.

This NDA was based on positive data from the GRACE study and confirmatory evidence from the phase III GRADIENT study, as well as long-term extension studies and a phase II study in hypercortisolism.

Per the FDA, even though the GRACE study met its primary endpoint and the GRADIENT study supported the findings, the agency could not determine that relacorilant’s benefits outweigh its risks without additional evidence of effectiveness from Corcept. The CRL likely delayed the potential approval of relacorilant, which could have helped the company reduce its heavy dependence on the sole-marketed drug, Korlym, for growth.

Korlym is approved for treating Cushing's syndrome or endogenous hypercortisolism. In the first nine months of 2025, Korlym recorded sales of $559.3 million, up around 13.4% year over year.

Having already encountered a roadblock with relacorilant in Cushing’s syndrome, investor attention now turns to the upcoming FDA decision in platinum-resistant ovarian cancer.

Corcept Therapeutics Incorporated price | Corcept Therapeutics Incorporated Quote

Corcept currently carries a Zacks Rank #5 (Strong Sell).

Some better-ranked stocks in the biotech sector are Alkermes ALKS and Immunocore IMCR, both sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Over the past 60 days, estimates for Alkermes’ 2026 earnings per share (EPS) have increased from $1.54 to $1.91. Shares of ALKS have gained 24.9% over the past six months.

Alkermes’ earnings beat estimates in three of the trailing four quarters, while missing the same on the remaining occasion, with the average surprise being 4.58%.

Over the past 60 days, Immunocore’s loss per share estimates for 2026 have decreased from 97 cents to 90 cents. Shares of IMCR have lost 2.3% over the past six months.

Immunocore’s earnings beat estimates in three of the trailing four quarters, while missing the same on the remaining occasion, with the average surprise being 53.96%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jun-29 | |

| Jun-29 | |

| Jun-26 | |

| Jun-17 | |

| Jun-17 | |

| Jun-15 | |

| Jun-12 | |

| Jun-06 | |

| Jun-04 | |

| Jun-03 | |

| May-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite