|

|

|

|

|||||

|

|

|

Flowserve has been on fire lately. In the past six months alone, the company’s stock price has rocketed 43.6%, setting a new 52-week high of $78.61 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy FLS? Or are investors being too optimistic? Find out in our full research report, it’s free.

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE:FLS) manufactures and sells flow control equipment for various industries.

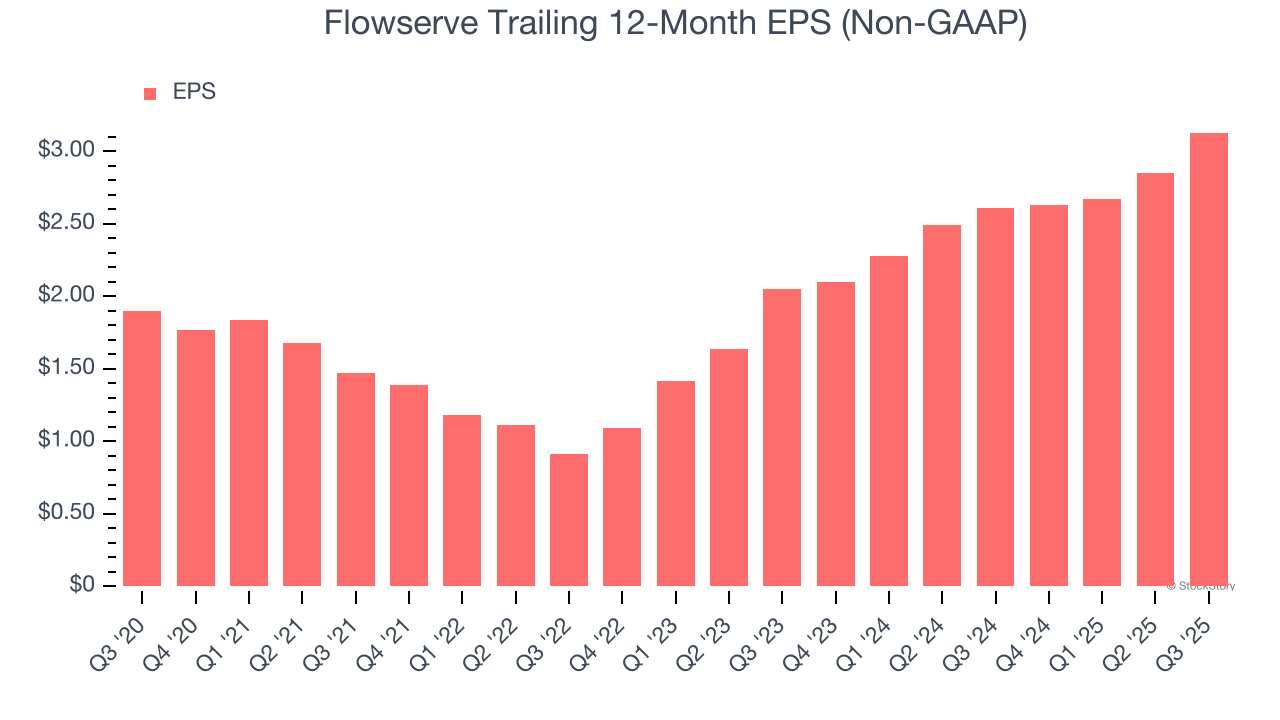

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Flowserve’s EPS grew at a solid 10.5% compounded annual growth rate over the last five years, higher than its 4.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

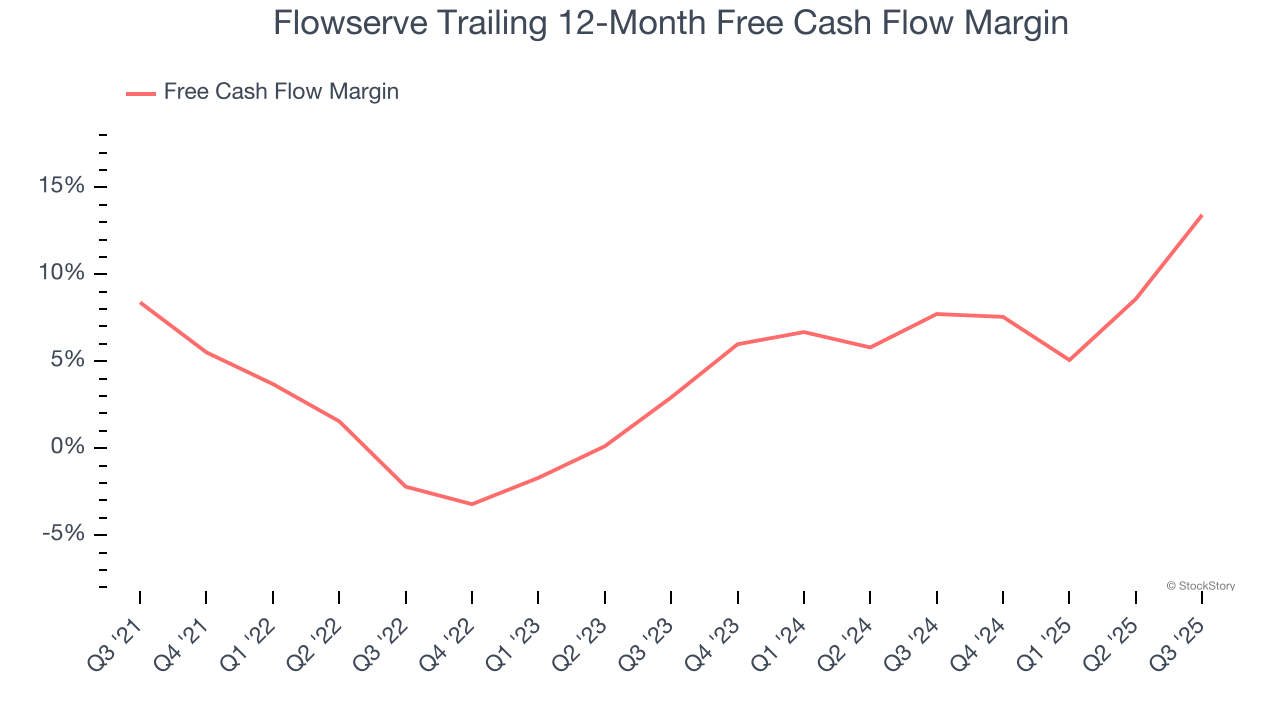

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Flowserve’s margin expanded by 5 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Flowserve’s free cash flow margin for the trailing 12 months was 13.4%.

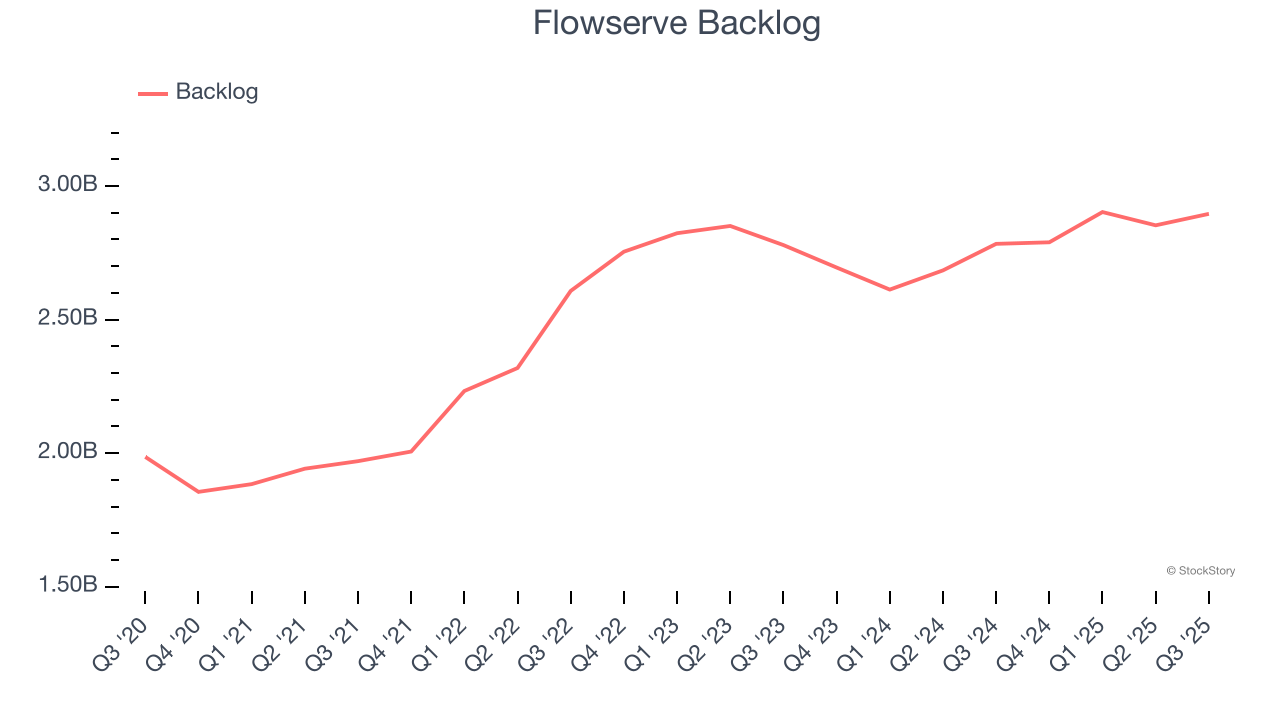

In addition to reported revenue, backlog is a useful data point for analyzing Gas and Liquid Handling companies. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Flowserve’s future revenue streams.

Flowserve’s backlog came in at $2.90 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 1.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

Flowserve has huge potential even though it has some open questions, and with the recent surge, the stock trades at 19.9× forward P/E (or $78.61 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Aug-05 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-15 | |

| Jun-30 | |

| Jun-30 | |

| Jun-24 | |

| Jun-24 | |

| May-28 | |

| May-28 | |

| May-14 | |

| May-05 | |

| Apr-30 | |

| Apr-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite