|

|

|

|

|||||

|

|

|

ASML Holding ASML is strategically increasing its gross margin. In 2023, the company posted a gross margin of 50.5%. In 2024, ASML posted a gross margin of 51.3%, and now ASML expects its 2025 gross margin to be between 54% and 56%, with a 2030 projection stating a gross margin of 56% to 60%.

ASML plans to achieve this by driving a shift in product mix toward more advanced logic and dynamic random access memory (DRAM) as these applications demand heavier use of advanced lithography systems. As the market for extreme ultraviolet lithography products scales, ASML is expected to benefit from the economies of scale, driving gross margin up.

ASML Holding discussed on its third-quarter 2025 earnings call that its strong productivity roadmap for low-numerical aperture (NA) systems and the launch of High-NA will support further reductions in technology costs and enable more multi-patterning layers to be converted into a single EUV exposure, particularly for advanced DRAM nodes.

ASML is in the middle of a shift that is taking place in the advanced chip manufacturing space, as companies move from complex multi-patterning with deep ultraviolet (DUV) toward single-exposure EUV for simplifying production, improving yield, lowering process complexity, and supporting advanced scaling.

ASML will gain from a near-monopoly in extreme ultraviolet (EUV) technology crucial for the world’s most advanced chips at 3nm and below. This gives the company the benefits of extraordinary pricing power and strategic importance. Major customers like TSMC, Samsung and Intel rely on ASML’s systems to stay ahead in chip innovation.

ASML Holding is the leading player in the lithography-based manufacturing and a near-monopoly in the EUV market. However, in the broader wafer fabrication equipment space, it competes against Lam Research LRCX and Applied Materials AMAT.

Lam Research is an established wafer fabrication equipment manufacturer that is established in the memory space. Lam Research’s memory segment, accounting for both Dynamic Random Access Memory and Non-Volatile Memory divisions, is gaining traction on the back of AI. Lam Research is also winning multiple clients as DRAM manufacturers are using its latest conductor etch tool, Akara.

Applied Materials specializes in Gate-All-Around transistors at 2nm and below, Backside power delivery, Advanced wiring and interconnect, HBM stacking and hybrid bonding and 3D device metrology, which are indispensable for manufacturing next-generation semiconductor chips. Recent launches like Xtera epi, Kinex hybrid bonding, PROVision 10 eBeam will add to AMAT’s growth story.

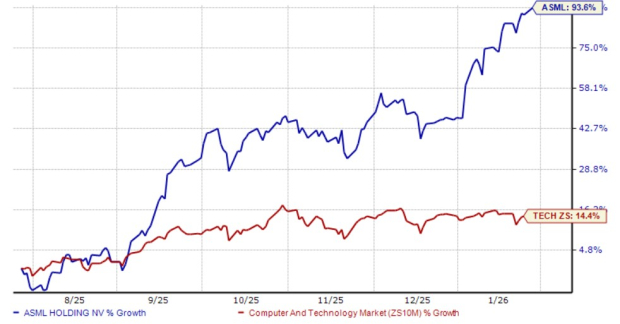

Shares of ASML have gained 93.6% in the past six months compared with the Computer and Technology sector’s growth of 14.4%.

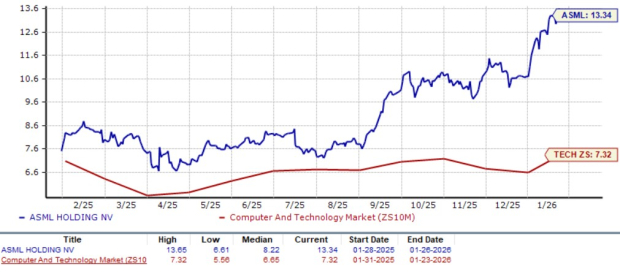

From a valuation standpoint, ASML trades at a forward price-to-sales ratio of 13.34X, higher than the sector’s average of 7.32X.

The Zacks Consensus Estimate for ASML’s fiscal 2025 and 2026 earnings implies year-over-year growth of 40.7% and 7.7%, respectively. The consensus estimate for fiscal 2025 and 2026 has been revised upward in the past seven days.

ASML currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 5 hours | |

| 10 hours | |

| 10 hours | |

| 11 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite