|

|

|

|

|||||

|

|

|

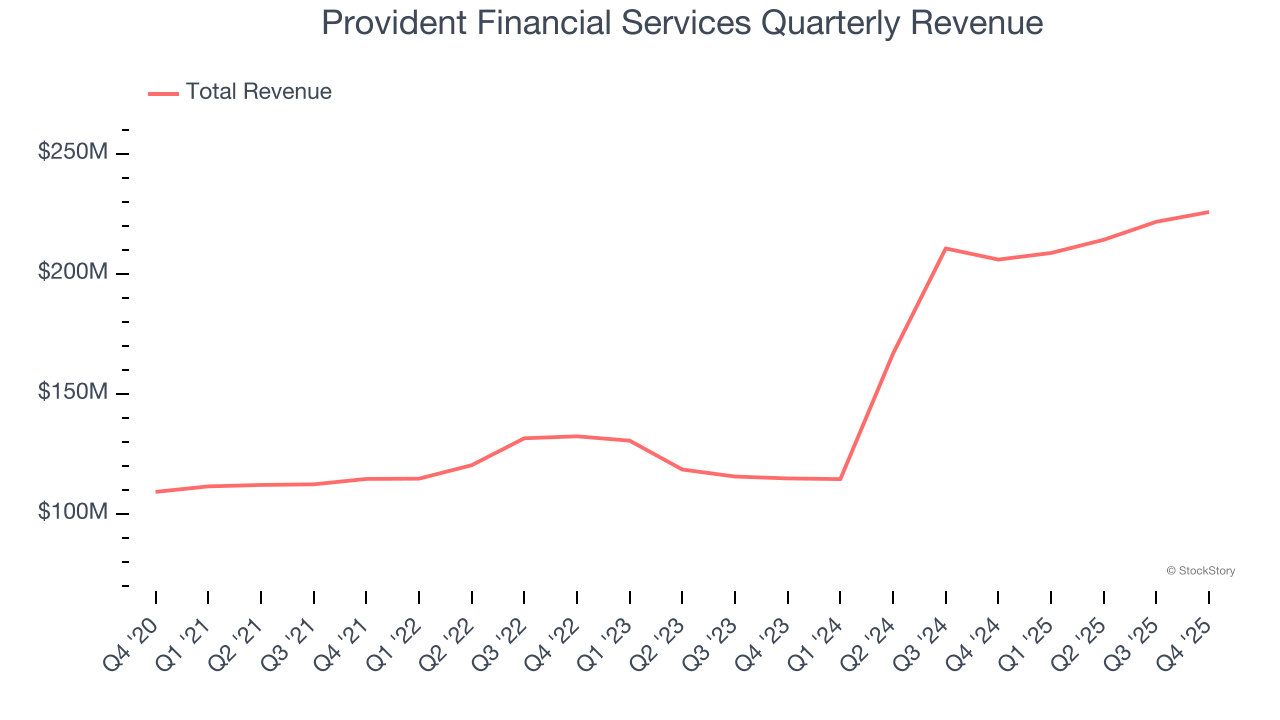

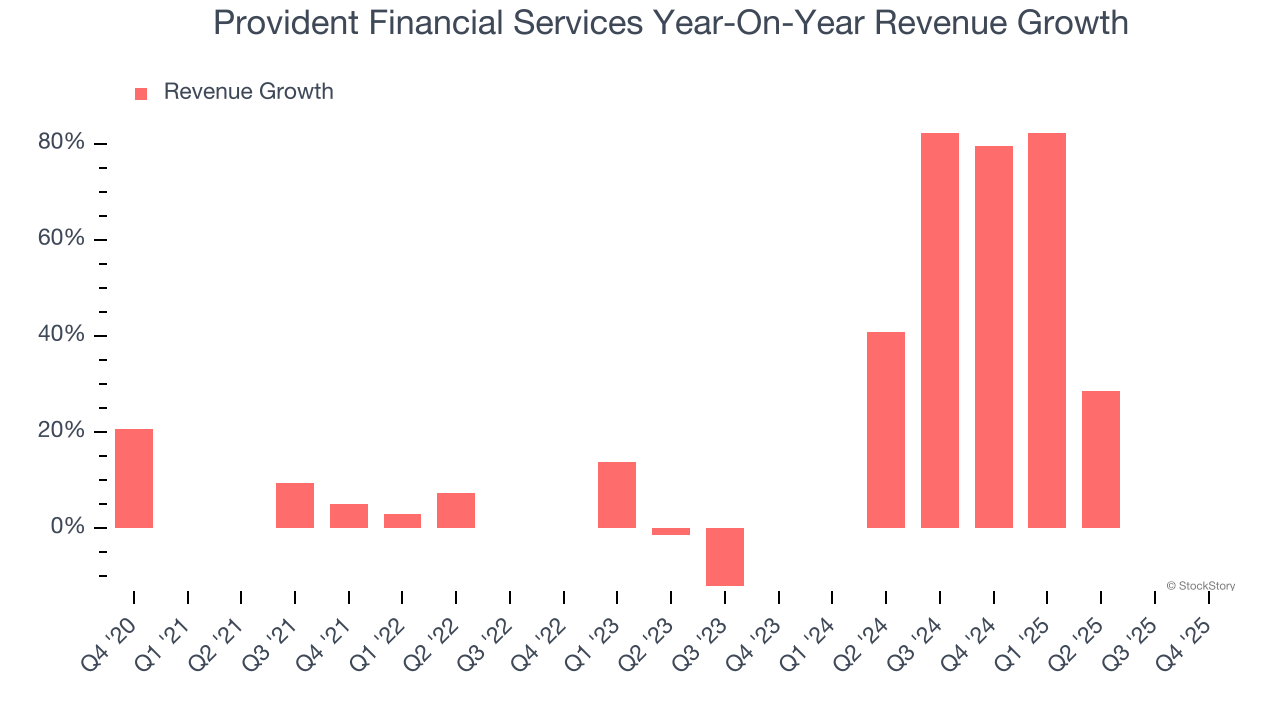

Regional bank Provident Financial Services (NYSE:PFS) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 9.6% year on year to $225.7 million. Its GAAP profit of $0.64 per share was 15.1% above analysts’ consensus estimates.

Is now the time to buy Provident Financial Services? Find out by accessing our full research report, it’s free.

Anthony J. Labozzetta, President and Chief Executive Officer commented, “Provident Bank finished 2025 with a third consecutive quarter of record revenues, notable momentum across all our business lines and strong profitability. Organic growth remains our top priority, supported by a loan pipeline that has consistently been over $2.5 billion for the past four quarters, and several investments we have made to sustain growth in non-interest income. Our organization continues to focus on several strategic initiatives to help profitably grow our business, including growing our market share in middle market banking, insurance and wealth management. Looking ahead to 2026, we expect continued earnings per share growth and to compound tangible book value, while also making the necessary investments to sustain our momentum over the long-term."

Founded in 1839 and serving communities across New Jersey, Pennsylvania, and New York, Provident Financial Services (NYSE:PFS) operates a regional bank providing commercial, residential, and consumer lending alongside wealth management and insurance services.

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Thankfully, Provident Financial Services’s 17.7% annualized revenue growth over the last five years was excellent. Its growth beat the average banking company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Provident Financial Services’s annualized revenue growth of 34.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Provident Financial Services reported year-on-year revenue growth of 9.6%, and its $225.7 million of revenue exceeded Wall Street’s estimates by 1%.

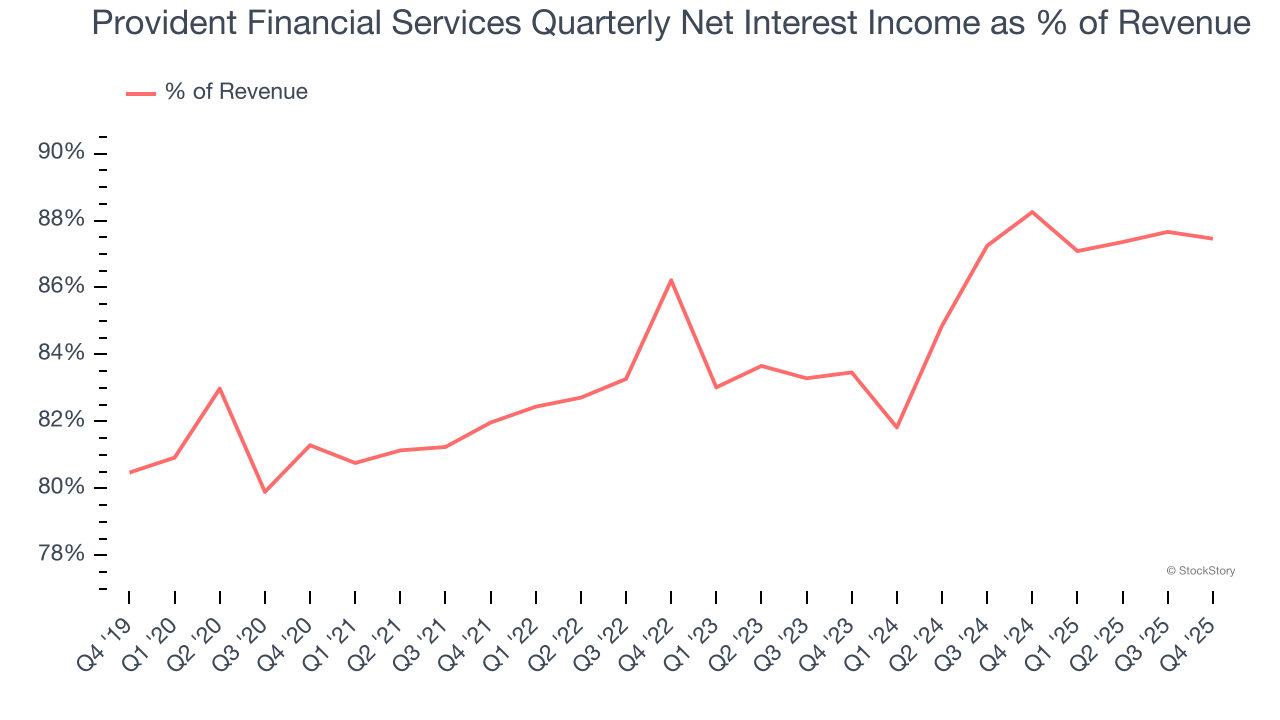

Net interest income made up 84.2% of the company’s total revenue during the last five years, meaning Provident Financial Services barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

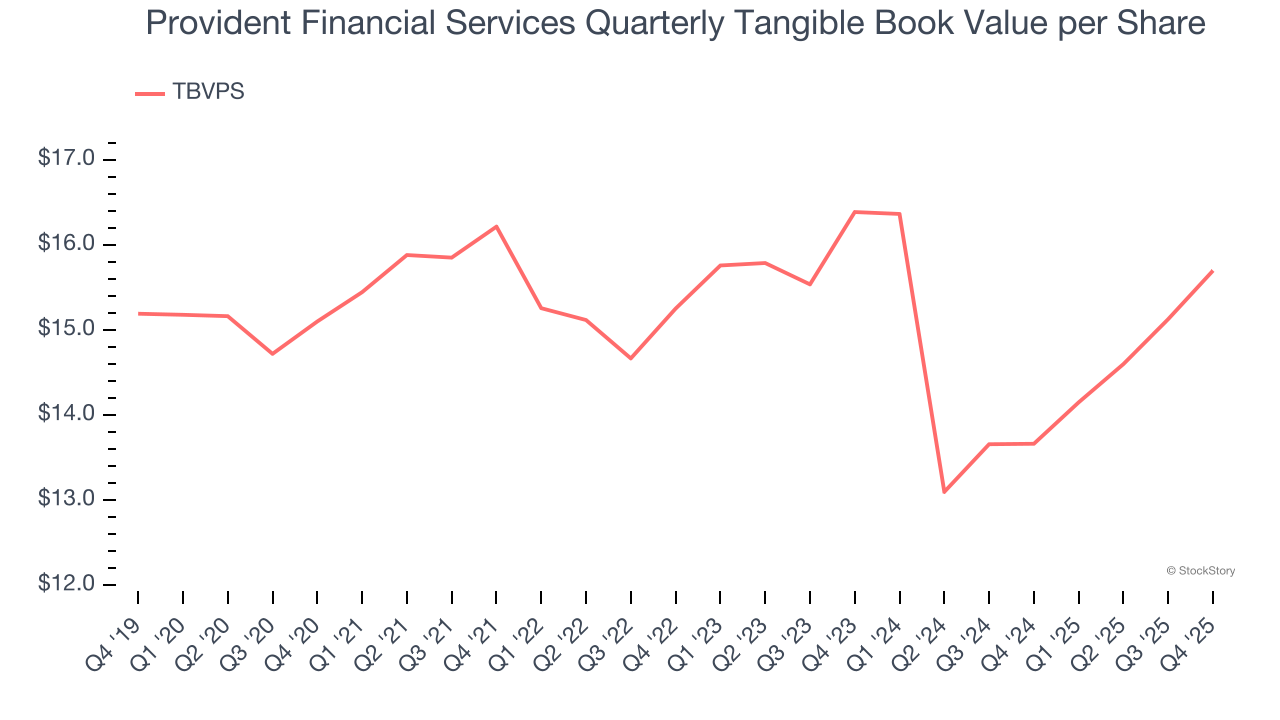

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Provident Financial Services’s TBVPS was flat over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 2.1% annually over the last two years ($16.39 to $15.70 per share).

Over the next 12 months, Consensus estimates call for Provident Financial Services’s TBVPS to grow by 8.9% to $17.10, paltry growth rate.

It was good to see Provident Financial Services beat analysts’ EPS expectations this quarter. We were also happy its tangible book value per share narrowly outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $21.02 immediately following the results.

Sure, Provident Financial Services had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-22 | |

| Jul-15 | |

| Jul-01 | |

| Jun-23 | |

| Jun-17 | |

| Jun-04 | |

| May-27 | |

| May-14 | |

| May-04 | |

| Apr-30 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-28 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite