|

|

|

|

|||||

|

|

|

This week’s reporting docket is headlined by many notable companies, a list that includes beloved Mag 7 member Apple AAPL. Shares have had a negative showing in 2026 so far, down roughly 5% and underperforming relative to the S&P 500.

But can the tech titan’s results push some life back into shares? Let’s take a closer look at revisions and a few other key metrics to keep an eye on.

The EPS outlook for the tech titan has remained stable and positive over recent months, with the current Zacks Consensus EPS estimate of $2.65 up 1.1% since the beginning of last November. Sales revisions have followed a similar path, with the $137.4 billion consensus estimate up 1.2% over the same period.

As shown below, the company’s top line has shown steady improvement over recent years, with its high-flying growth days largely behind it. The stock commonly reflects a ‘safer’ tech play given its size and maturity, partly explaining why it generally trades at rich valuation multiples despite not posting outsized growth. Shares currently trade at a 30.0X forward 12-month earnings multiple, reflecting a 30% premium relative to the S&P 500.

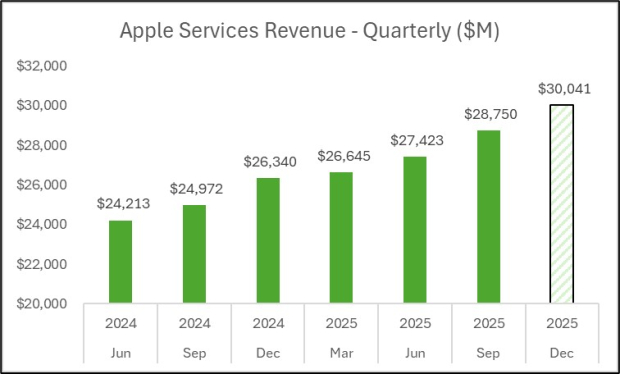

A key metric to watch in the release is Apple’s Services results, which have regularly been robust and reached record levels throughout recent periods. Apple’s Services segment represents all the recurring, non-hardware revenue tied to its ecosystem, such as Apple Music, Apple Pay, App Store, and Apple TV+, for a few examples.

Our consensus Services estimate stands just at $30.0 billion, reflecting a 14% YoY climb. Below is a chart illustrating AAPL’s Services revenues on a quarterly basis, with our consensus estimate also blended in.

Keep in mind that Alphabet GOOGL and AAPL announced a multi-year collaboration under which the next generation of Apple Foundation Models will be based on Google's Gemini models and cloud technology.

Notably, AAPL has yet to have its big AI moment. The reaction to Apple Intelligence so far has been mixed at best, with several highly anticipated features, like an improved Siri, delayed during the initial rollout.

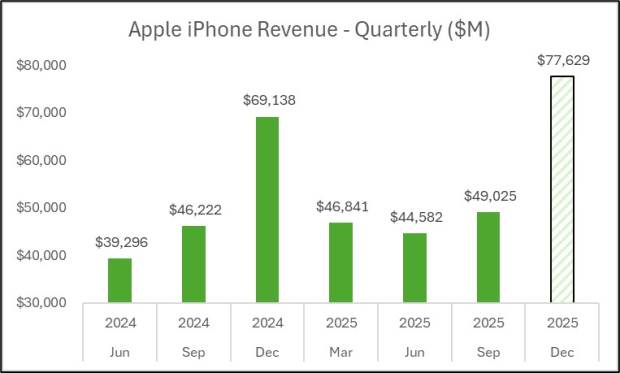

We’ll undoubtedly hear a lot about the collaboration during the earnings call, especially given the current sentiment surrounding its AI ventures. Of course, this leads back to iPhone sales, which we forecast to reach $77.6 billion throughout the period. The iPhone still remains the largest sales contributor, but the Services segment’s growth has helped reduce the reliance on this critical segment.

Below is a chart illustrating the company’s iPhone sales on a quarterly basis, with our consensus estimate also blended in. iPhone sales spike during the period due to the September launch.

Bottom Line

Beloved Apple AAPL is gearing up to reveal its next set of quarterly results this week, with many other notable companies slated to report.

Analysts have kept their revisions positive and stable, a key development heading into the release. While shares are a bit rich, the company has historically traded at a steep multiple given its consistent and cash-generating nature. Below is a chart illustrating its free cash flow on a quarterly basis.

Investors should keep a close eye on commentary surrounding the recent deal with Alphabet GOOGL given its weak AI story so far, with iPhone and Services results also reflecting key metrics.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite