|

|

|

|

|||||

|

|

|

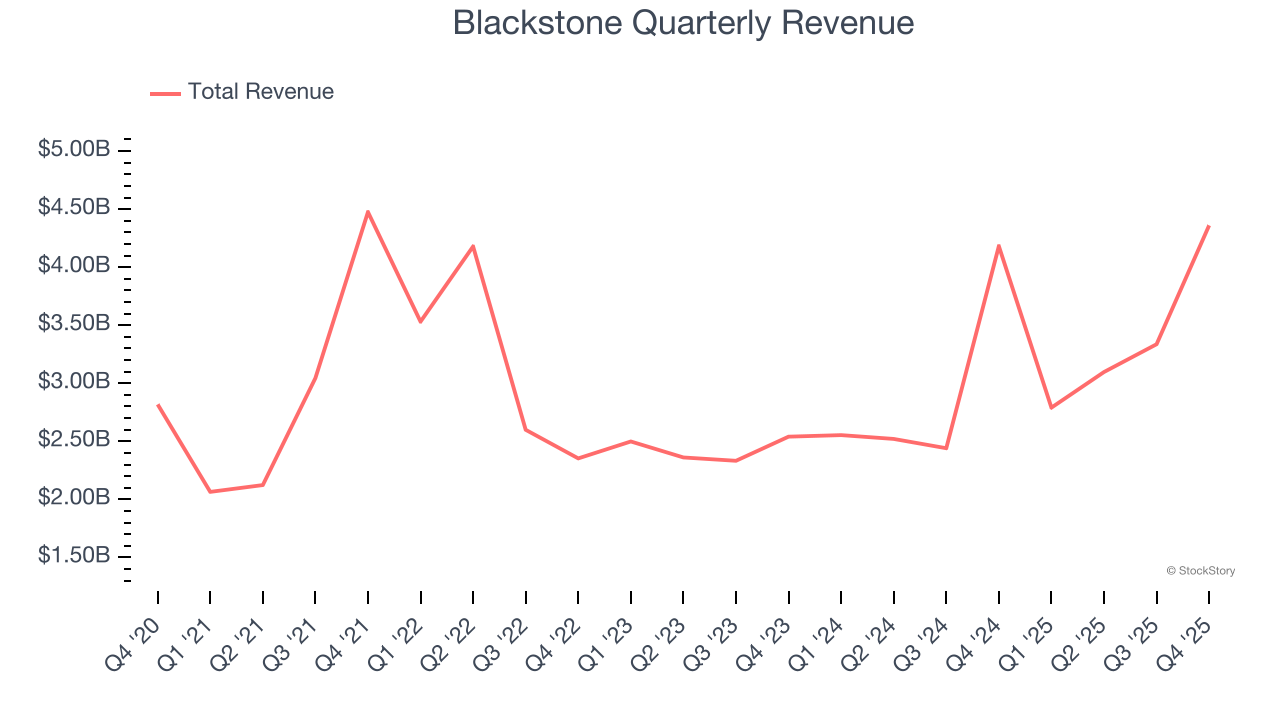

Alternative investment manager Blackstone (NYSE:BX) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 4.3% year on year to $4.36 billion. Its GAAP profit of $1.30 per share was 15.8% below analysts’ consensus estimates.

Is now the time to buy Blackstone? Find out by accessing our full research report, it’s free.

With over $1 trillion in assets under management and investments spanning real estate, private equity, credit, and hedge funds, Blackstone (NYSE:BX) is a global alternative asset manager that invests capital on behalf of pension funds, sovereign wealth funds, and other institutional investors.

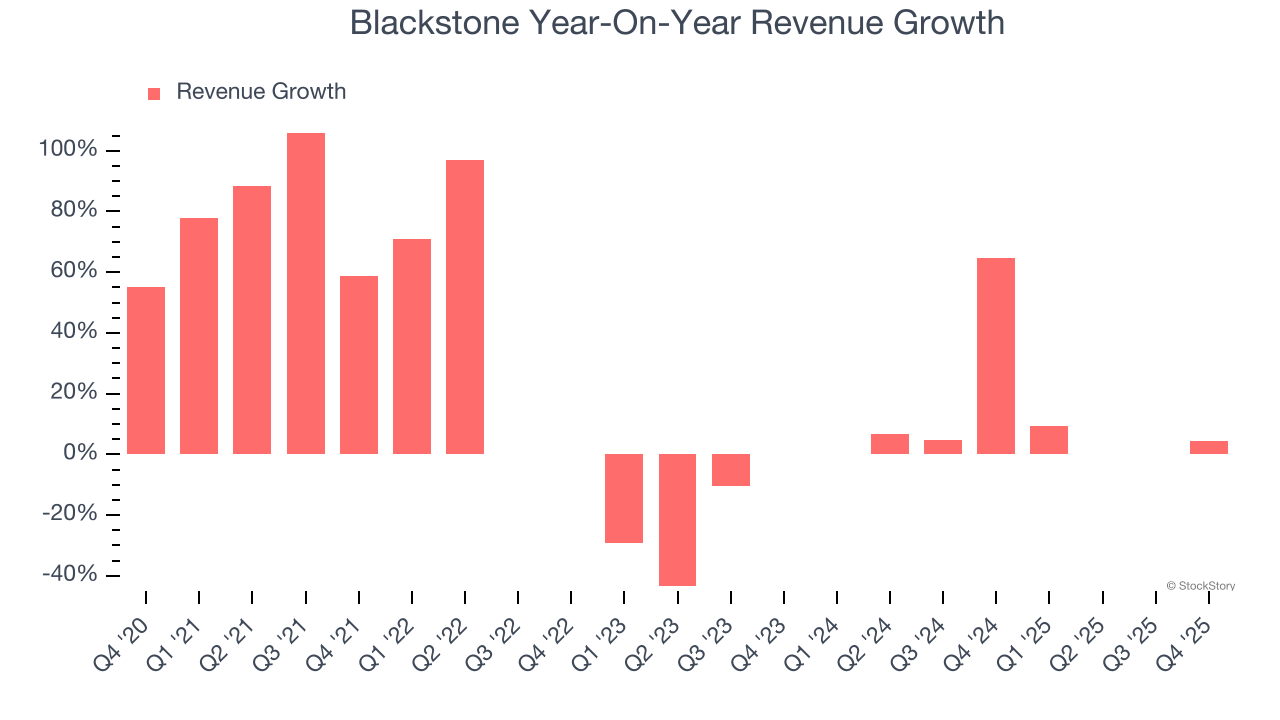

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Blackstone grew its revenue at an impressive 15.6% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Blackstone’s annualized revenue growth of 18.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Blackstone reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 17.2%.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

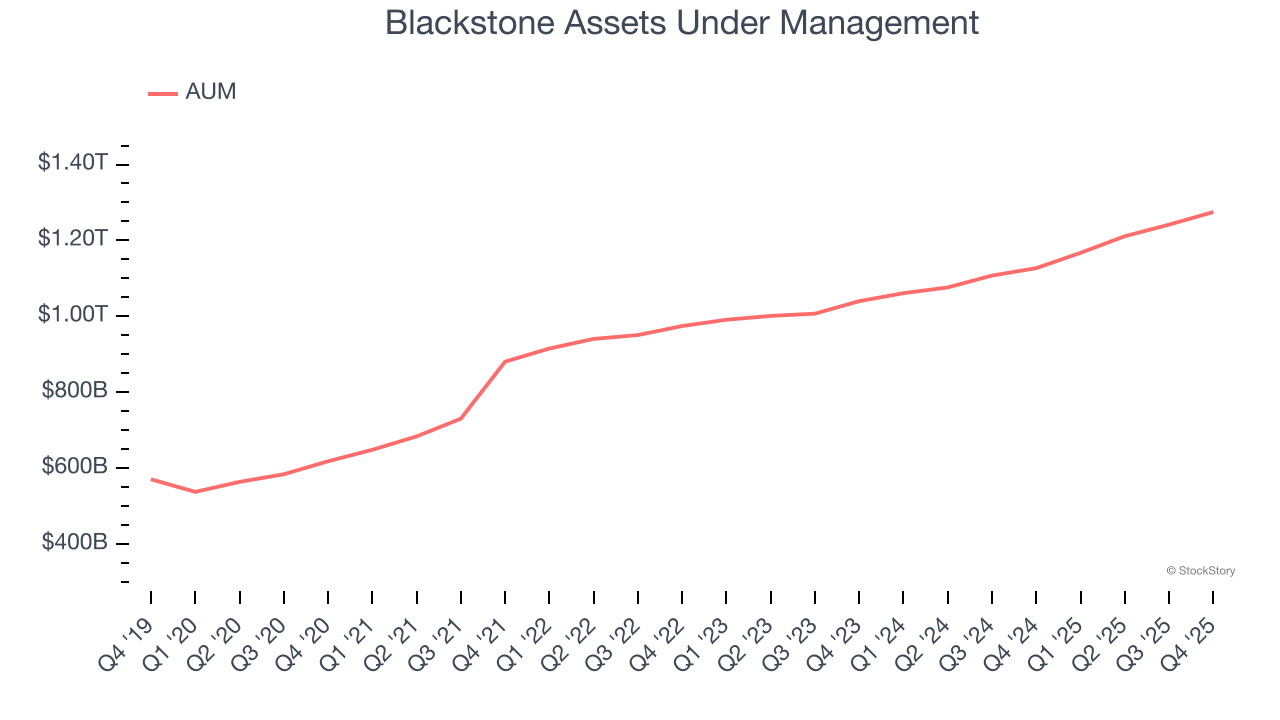

Assets Under Management (AUM) is the cornerstone of a financial firm's investment division, representing all client capital under its stewardship. Management fees on this AUM create reliable, recurring revenue that maintains stability even when investment performance struggles, though prolonged poor returns can eventually affect asset retention and growth.

Blackstone’s AUM has grown at an annual rate of 16.3% over the last five years, better than the broader financials industry and faster than its total revenue. When analyzing Blackstone’s AUM over the last two years, we can see that growth decelerated to 10.1% annually. Fundraising or short-term investment performance were net detractors to the company over this shorter period since assets grew slower than total revenue. That said, assets aren't the be-all and end-all due to their unpredictable and cyclical nature.

In Q4, Blackstone’s AUM was $1.27 trillion, meeting analysts’ expectations. This print was 13.1% higher than the same quarter last year.

We were impressed by how significantly Blackstone blew past analysts’ fee-related earnings expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.3% to $148.68 immediately following the results.

Blackstone had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| 1 hour | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite