|

|

|

|

|||||

|

|

|

Over the past six months, Freshworks’s stock price fell to $11.38. Shareholders have lost 18.2% of their capital, which is disappointing considering the S&P 500 has climbed by 9.5%. This might have investors contemplating their next move.

Following the pullback, is now an opportune time to buy FRSH? Find out in our full research report, it’s free.

Starting as a customer service solution before expanding into a comprehensive software suite, Freshworks (NASDAQ:FRSH) provides AI-powered software-as-a-service solutions that help companies manage customer service, IT support, sales, and marketing functions.

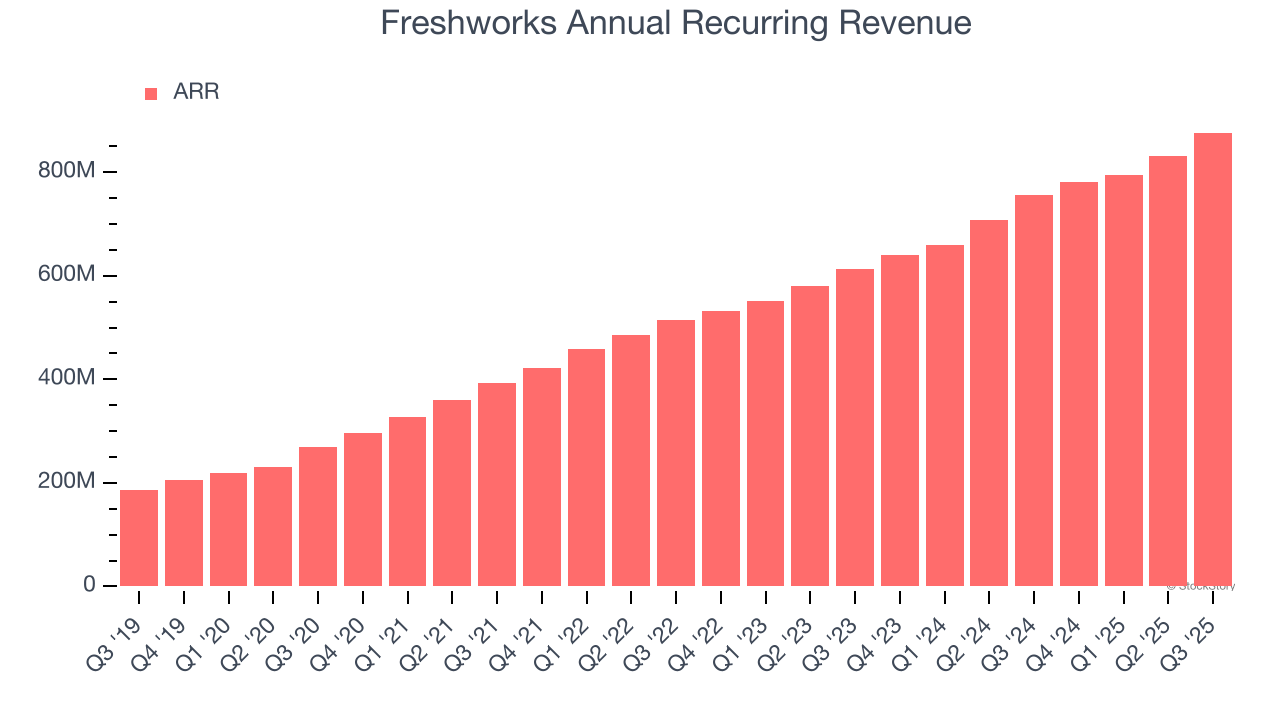

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Freshworks’s ARR punched in at $876.7 million in Q3, and over the last four quarters, its year-on-year growth averaged 19%. This performance was solid, reflecting the company’s ability to maintain strong customer relationships and secure longer-term commitments. Its growth also contributes positively to Freshworks’s predictability and valuation, as investors typically prefer businesses with recurring revenue.

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

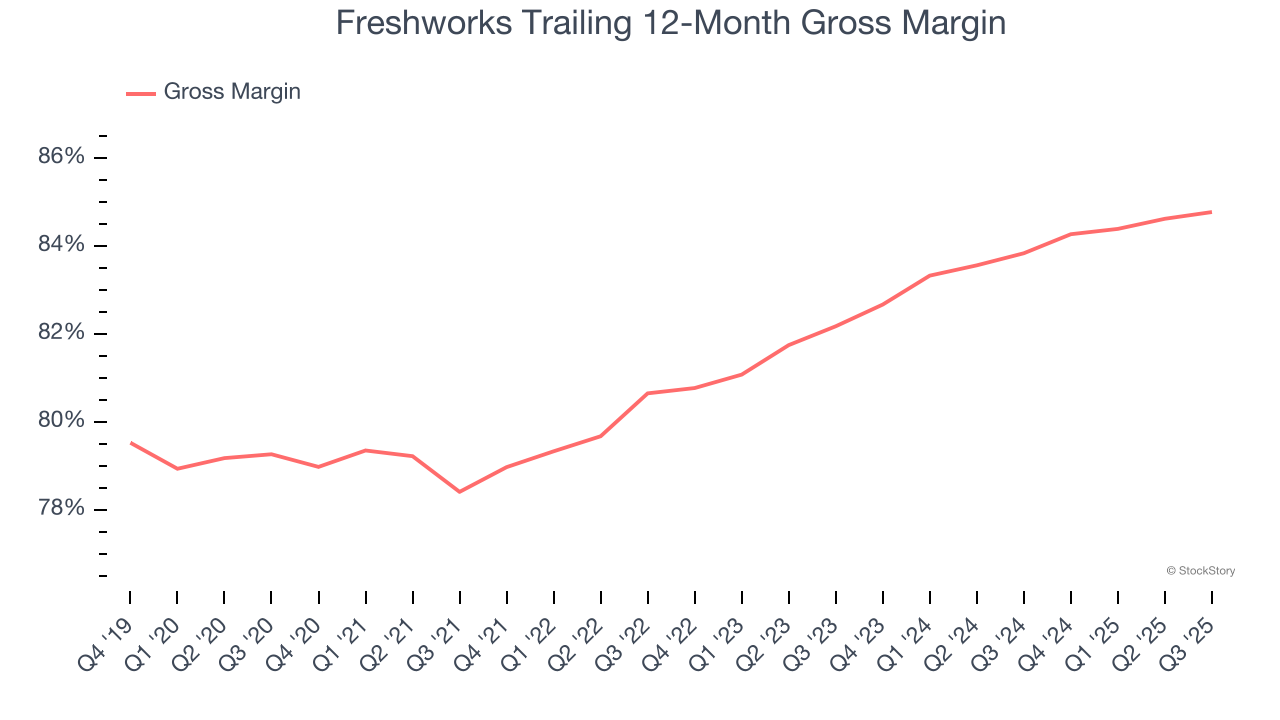

Freshworks’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 84.8% gross margin over the last year. Said differently, roughly $84.77 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Freshworks has seen gross margins improve by 2.6 percentage points over the last 2 year, which is very good in the software space.

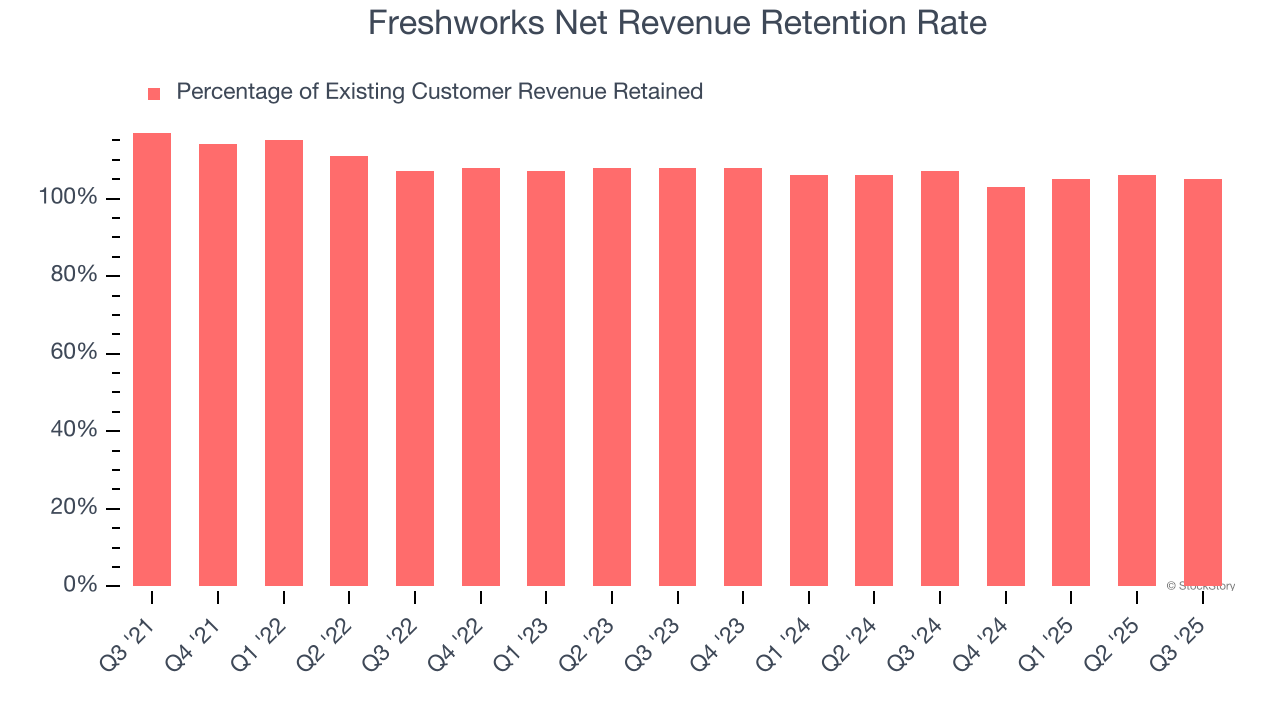

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Freshworks’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 105% in Q3. This means Freshworks would’ve grown its revenue by 4.8% even if it didn’t win any new customers over the last 12 months.

Freshworks has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

Freshworks’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 3.6× forward price-to-sales (or $11.38 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-29 | |

| Jul-28 | |

| Jul-23 | |

| Jul-08 | |

| Jun-30 | |

| May-27 | |

| May-20 | |

| May-14 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-09 | |

| Apr-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite