|

|

|

|

|||||

|

|

|

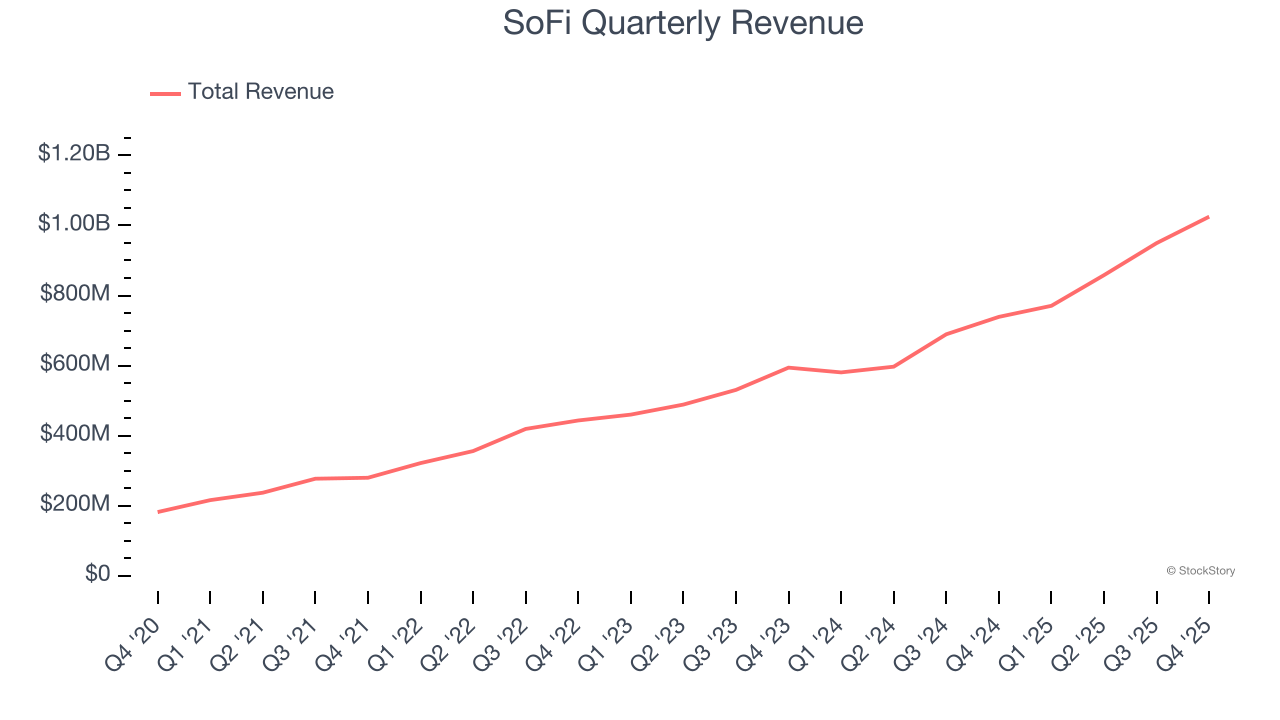

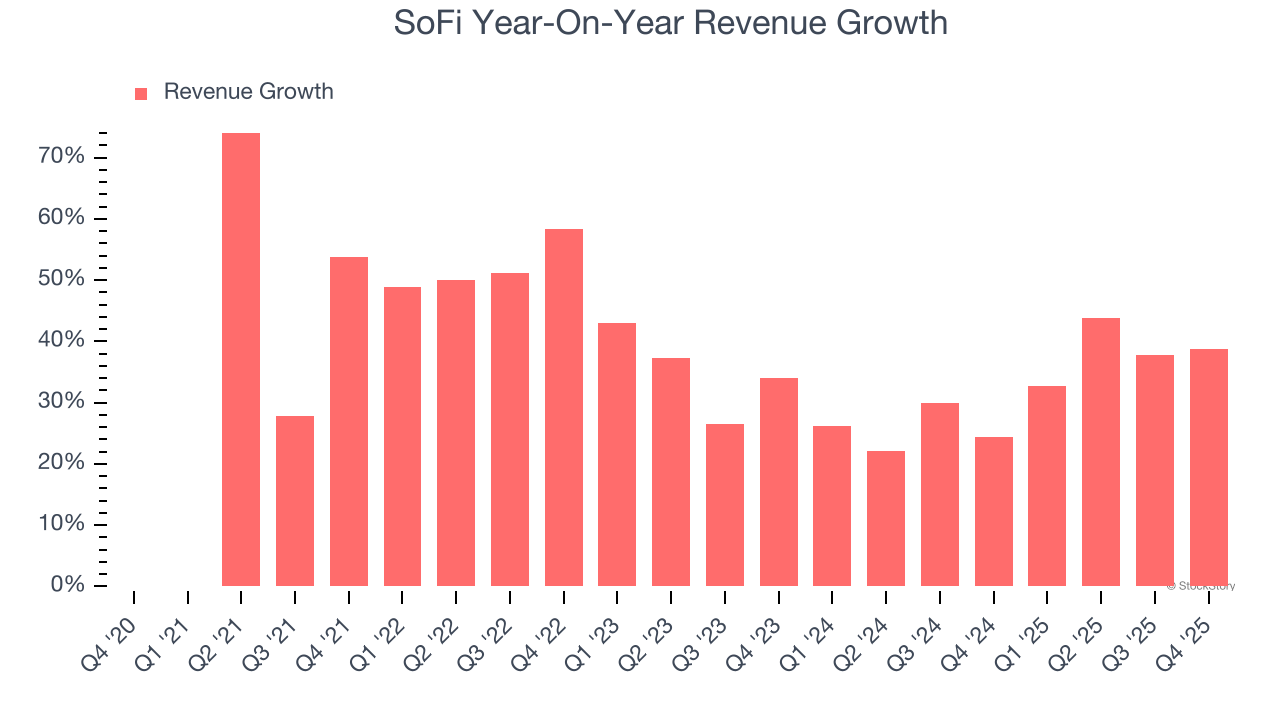

Digital financial services company SoFi Technologies (NASDAQ:SOFI) announced better-than-expected revenue in Q4 CY2025, with sales up 38.7% year on year to $1.03 billion. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $1.04 million was less impressive, coming in 99.9% below expectations. Its non-GAAP profit of $0.13 per share was 16.1% above analysts’ consensus estimates.

Is now the time to buy SoFi? Find out by accessing our full research report, it’s free.

Starting as a student loan refinancing company founded by Stanford business school students in 2011, SoFi Technologies (NASDAQ:SOFI) operates a digital financial platform offering lending, banking, investing, and other financial services to help members borrow, save, spend, invest, and protect their money.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, SoFi grew its revenue at an incredible 42.1% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. SoFi’s annualized revenue growth of 31.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, SoFi reported wonderful year-on-year revenue growth of 38.7%, and its $1.03 billion of revenue exceeded Wall Street’s estimates by 4%. Company management is currently guiding for a 99.9% year-on-year decline in sales next quarter.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

We were impressed by SoFi’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also glad its revenue and EPS both outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 5.7% to $25.70 immediately after reporting.

SoFi may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 |

Best high-yield savings interest rates today, March 31, 2026 (Earn up to 4% APY)

SOFI

Yahoo Personal Finance

|

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-28 |

Best high-yield savings interest rates today, March 28, 2026 (Earn up to 4% APY)

SOFI

Yahoo Personal Finance

|

| Mar-27 | |

| Mar-26 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite