|

|

|

|

|||||

|

|

|

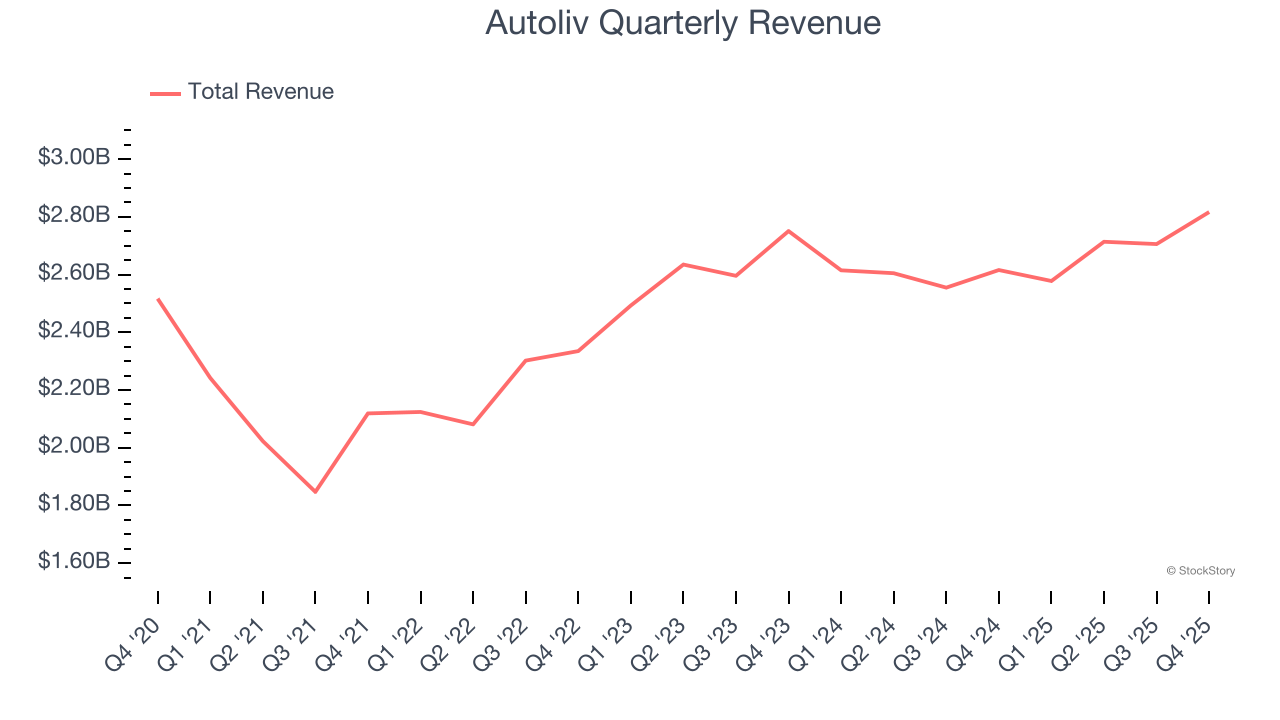

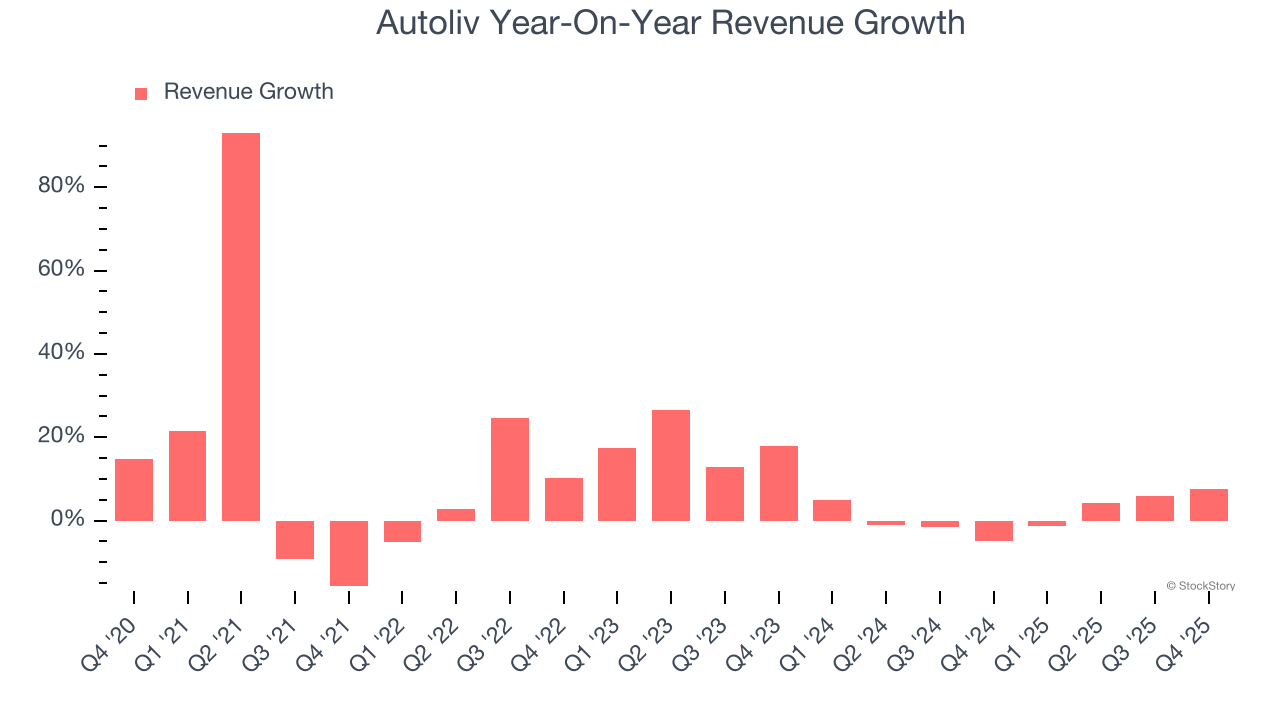

Automotive safety systems provider Autoliv (NYSE:ALV) announced better-than-expected revenue in Q4 CY2025, with sales up 7.7% year on year to $2.82 billion. Its non-GAAP profit of $3.19 per share was 10.7% above analysts’ consensus estimates.

Is now the time to buy Autoliv? Find out by accessing our full research report, it’s free.

With products estimated to save over 30,000 lives annually in traffic accidents worldwide, Autoliv (NYSE:ALV) develops and manufactures passive safety systems for vehicles, including airbags, seatbelts, and steering wheels that protect occupants during crashes.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Autoliv’s 7.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Autoliv’s recent performance shows its demand has slowed as its annualized revenue growth of 1.6% over the last two years was below its five-year trend. We also note many other Automobile Manufacturing businesses have faced declining sales because of cyclical headwinds. While Autoliv grew slower than we’d like, it did do better than its peers.

This quarter, Autoliv reported year-on-year revenue growth of 7.7%, and its $2.82 billion of revenue exceeded Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

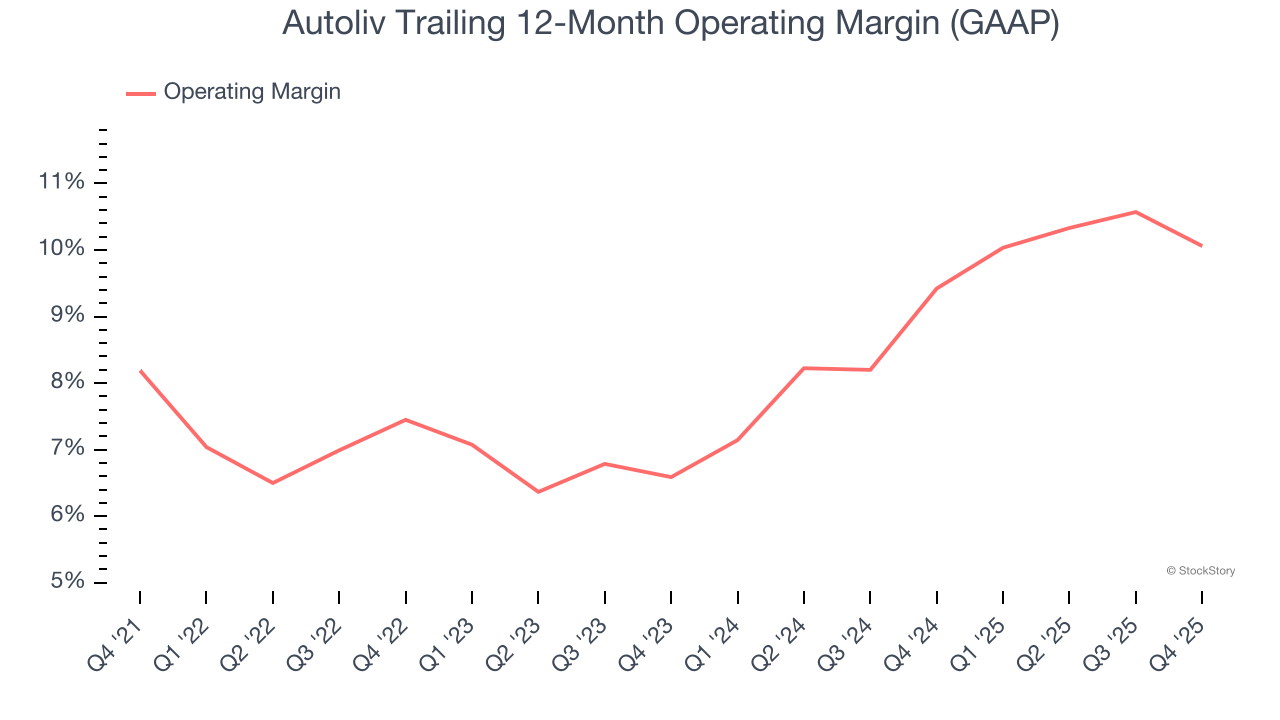

Autoliv has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.4%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Autoliv’s operating margin rose by 1.9 percentage points over the last five years, as its sales growth gave it operating leverage. Its expansion was impressive, especially when considering the cycle turned in the wrong direction and most of its Automobile Manufacturing peers observed plummeting revenue and margins.

This quarter, Autoliv generated an operating margin profit margin of 11.3%, down 2.2 percentage points year on year. Since Autoliv’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

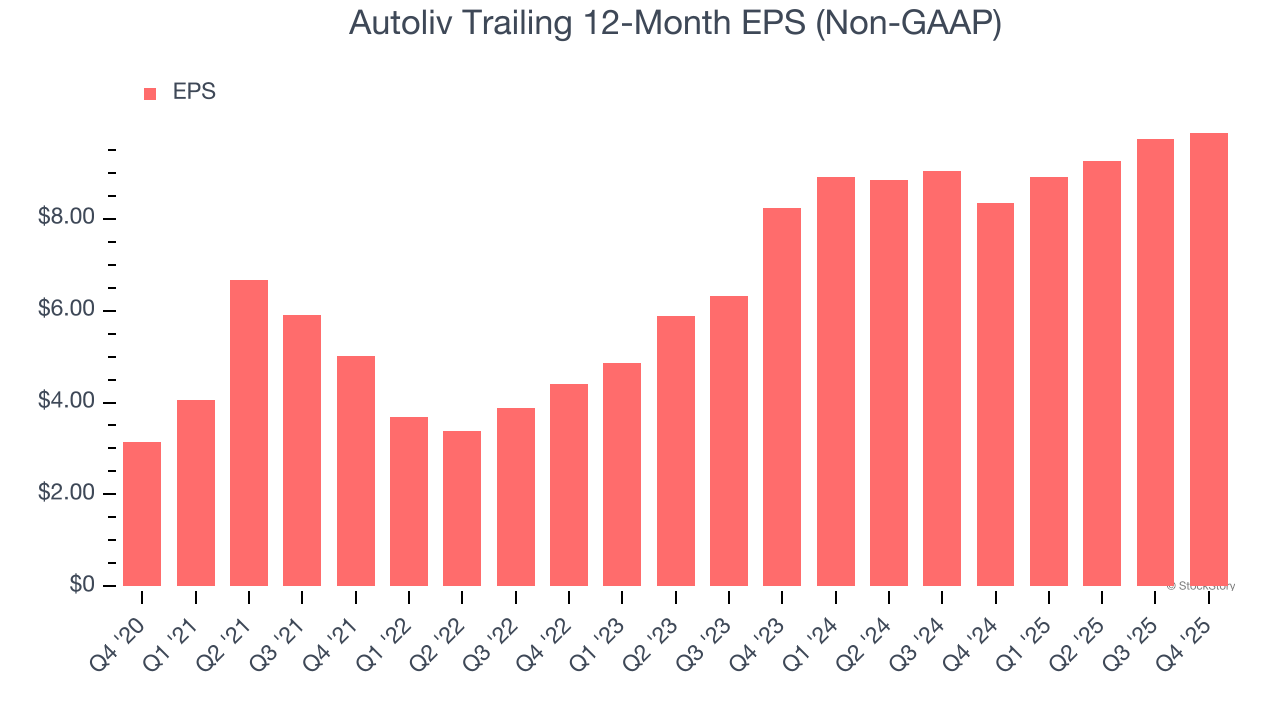

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Autoliv’s EPS grew at an astounding 25.7% compounded annual growth rate over the last five years, higher than its 7.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

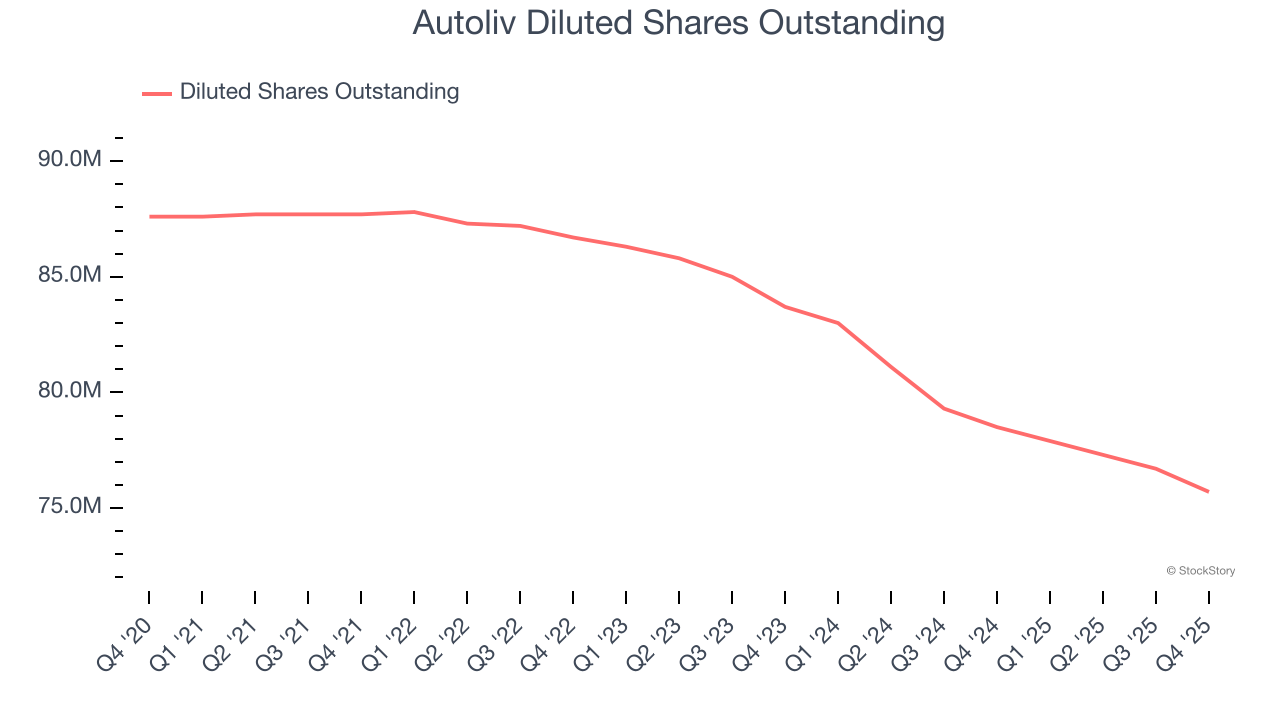

Diving into the nuances of Autoliv’s earnings can give us a better understanding of its performance. As we mentioned earlier, Autoliv’s operating margin declined this quarter but expanded by 1.9 percentage points over the last five years. Its share count also shrank by 13.6%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Autoliv, its two-year annual EPS growth of 9.5% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Autoliv reported adjusted EPS of $3.19, up from $3.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Autoliv’s full-year EPS of $9.87 to grow 10.4%.

It was good to see Autoliv beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 6.8% to $117.90 immediately following the results.

So should you invest in Autoliv right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jun-30 | |

| May-11 | |

| May-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite