|

|

|

|

|||||

|

|

|

FedEx has been on fire lately. In the past six months alone, the company’s stock price has rocketed 42.3%, reaching $318.63 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy FedEx, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the momentum, we're cautious about FedEx. Here are three reasons there are better opportunities than FDX and a stock we'd rather own.

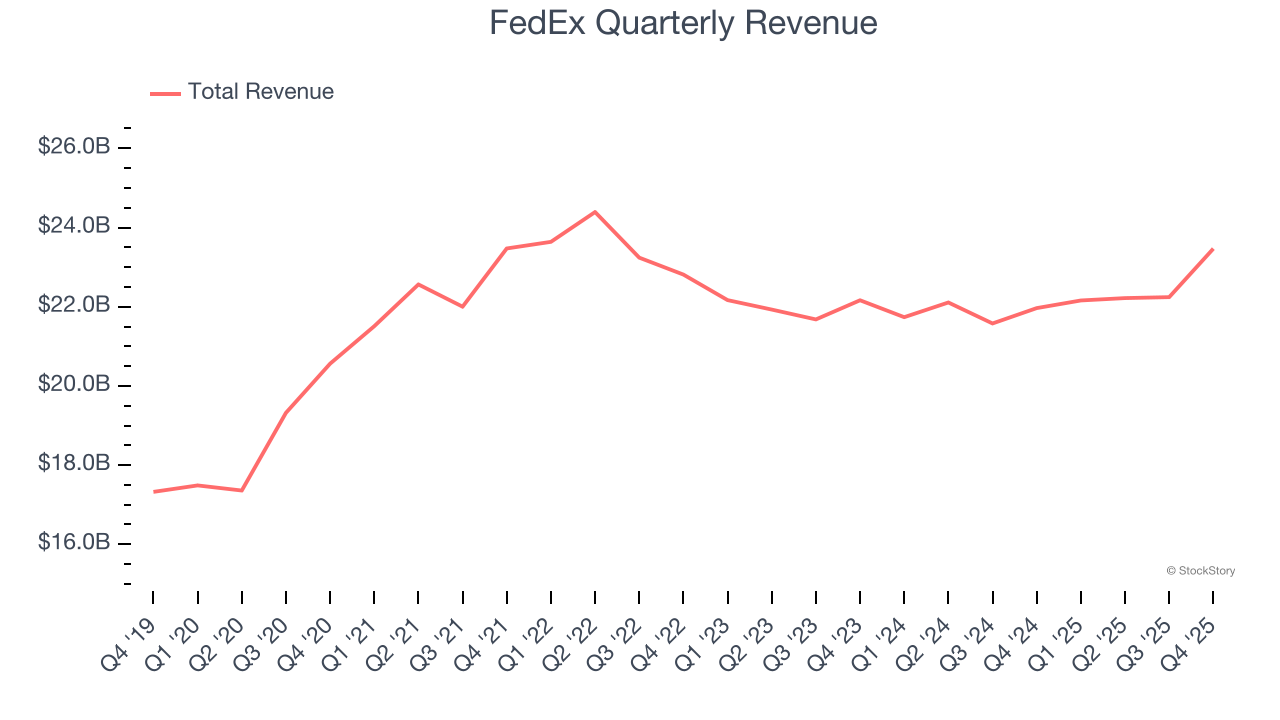

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, FedEx’s sales grew at a sluggish 3.8% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

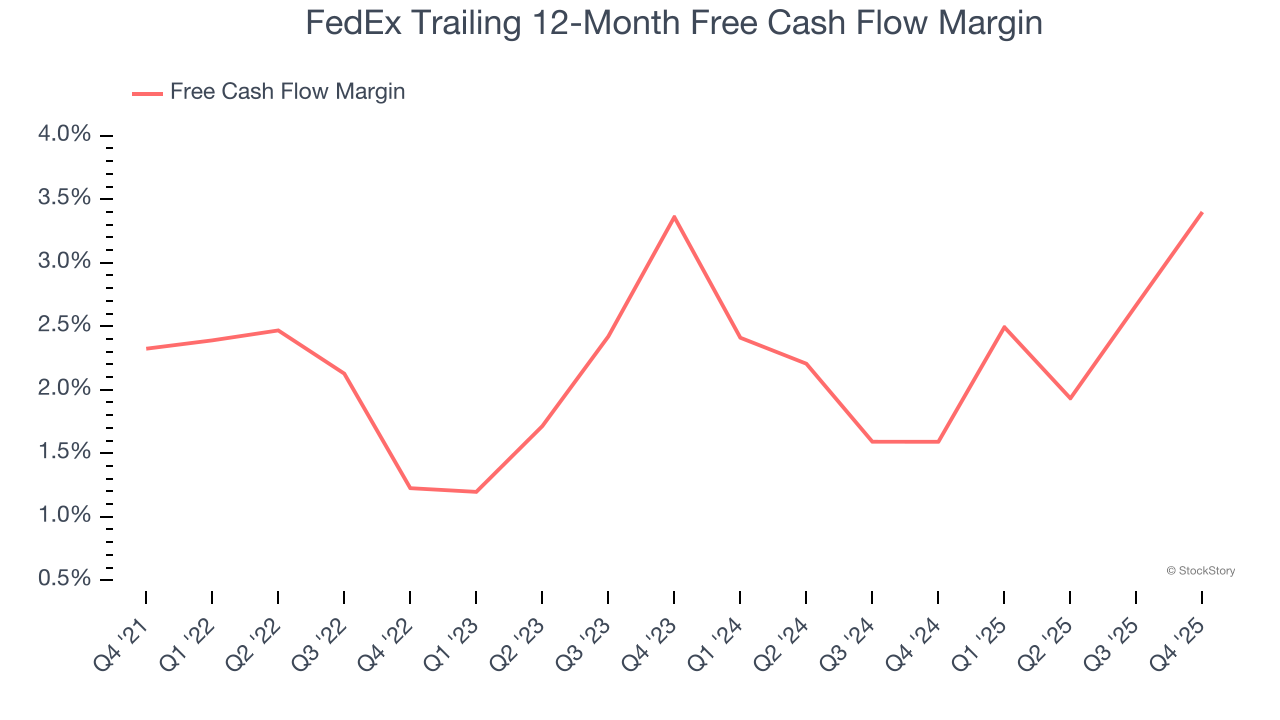

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

FedEx has shown poor cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.4%, lousy for an industrials business.

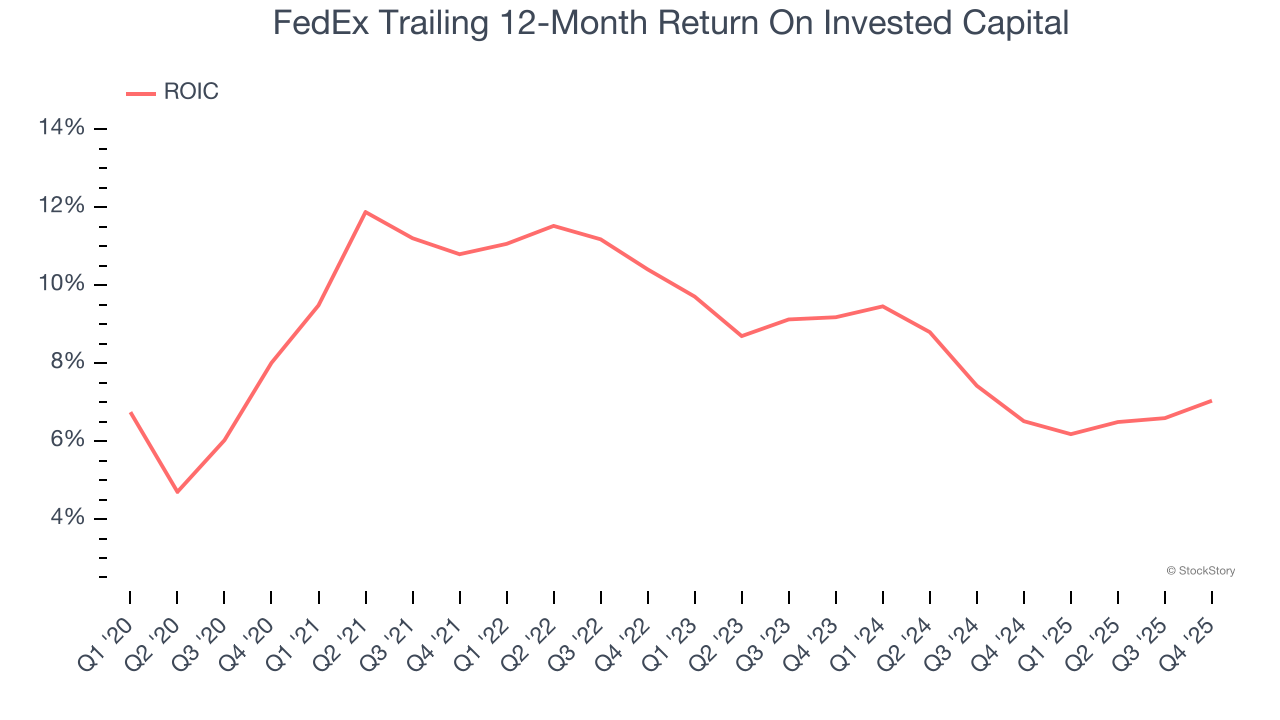

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, FedEx’s ROIC averaged 3.8 percentage point decreases each year. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

FedEx doesn’t pass our quality test. Following the recent surge, the stock trades at 16.2× forward P/E (or $318.63 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 9 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| Mar-17 | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-15 |

CEOs of top airlines demand Congress restore funding to Homeland Security and pay airport workers

FDX

Associated Press Finance

|

| Mar-15 | |

| Mar-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite