|

|

|

|

|||||

|

|

|

Figma was a hot IPO that's seen its share price sink over the past few months.

The company is producing strong sales, with third-quarter revenue growing 38% year over year.

Figma's customer acquisition and retention are excellent, but the business wasn't profitable in Q3.

Shares of design software developer Figma (NYSE: FIG) experienced incredible success when they went public last July, debuting at $33 per share before skyrocketing to a 52-week high of $142.92 in August.

Since then, the stock has reversed course big time. Shares hit a 52-week low of $26.79 on Jan. 21, dropping below the IPO price. This may be a great opportunity to scoop up Figma stock. Or could reasons exist to hold off?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Answering those questions requires a deeper dive into Figma's business.

Image source: Getty Images.

Figma is striving to reinvent design software, and one of the ways it's doing so is by incorporating artificial intelligence. For instance, the company acquired AI design start-up Weavy in October.

Weavy, now called Figma Weave, combines several leading AI models with professional editing tools to streamline the design process and enable designers to use AI as a collaborator to quickly achieve their creative visions.

The company's proprietary AI tool, Figma Make, is seeing 30% of customers providing annual recurring revenue (ARR) of $100,000 or more using it on a weekly basis, and usage is growing.

CFO Praveer Melwani explained the company's growth strategy on a November call with analysts, saying, "We deepened our investments in Q3 to build for the AI native workflows of the future." The approach is working, as evidenced by Figma's strong customer growth and retention.

In the third quarter of 2025, the company added more than 1,000 customers with ARR of $10,000 or more. In addition, Figma's net dollar retention rate for clients with ARR of at least $10,000 was 131%, which indicates these high-value customers are expanding their spending.

The company's success in acquiring and retaining customers is driving sales growth. In Q3, Figma achieved record revenue of $274.2 million, a 38% year-over-year increase. In fact, sales have grown every quarter since Q1 of 2024, when revenue totaled $156.2 million.

Figma expects that trend to continue. It anticipates Q4 revenue to come in between $292 million and $294 million, representing 35% year-over-year growth at the midpoint.

The company also boasts an outstanding balance sheet. It exited Q3 with total assets of $2.1 billion, of which over $1.5 billion was cash, cash equivalents, and marketable securities. Total liabilities were $684.7 million, but $473.6 million of that was deferred revenue, representing upfront customer payments that will be recognized as sales after services are delivered.

Despite strong revenue growth, Figma suffered a massive Q3 net loss of $1.1 billion due to stock-based compensation costs related to its IPO. In the second quarter, however, the company was profitable, posting net income of $28.2 million. This suggests Figma can return to profitability in subsequent quarters.

Even with the possibility of a near-term rebound to profitability, the company's large Q3 net loss, coupled with a sky-high stock valuation, has led to a steadily falling share price since the initial IPO spike. Consequently, the situation warrants an evaluation of the stock's current value.

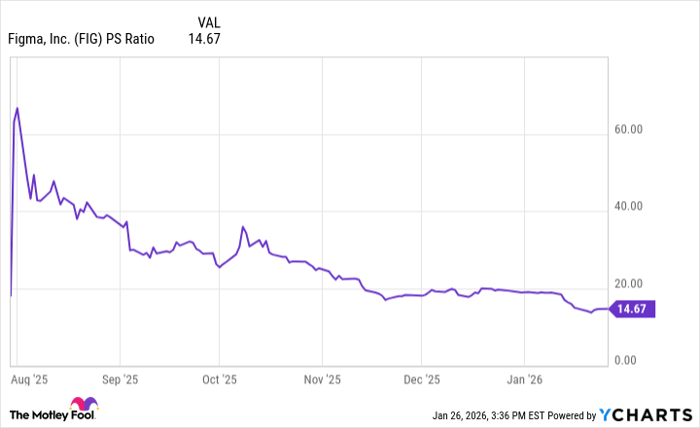

Given Figma wasn't profitable in Q3, its share price valuation can be assessed using the price-to-sales ratio (P/S), which measures how much investors are paying for every dollar of revenue generated over the trailing 12 months.

Data by YCharts.

The chart shows Figma's sales multiple exceeded 60 not long after the IPO, but has steadily declined since then. Now, the stock's P/S ratio of about 15 is far more reasonable.

Given the lower valuation, Figma looks like a compelling stock to buy. Its sales growth is poised to continue. Its excellent customer acquisition and retention numbers demonstrate that clients find its products valuable.

Figma's approach to AI, where the tech is an enabler rather than a replacement for human designers, is a sensible strategy given AI's limitations. Figma looks like it's making the right moves for long-term business success amid the rise of AI.

Before you buy stock in Figma, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Figma wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $450,256!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,171,666!*

Now, it’s worth noting Stock Advisor’s total average return is 942% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 31, 2026.

Robert Izquierdo has positions in Figma. The Motley Fool has positions in and recommends Figma. The Motley Fool has a disclosure policy.

| Jul-16 | |

| Jul-15 | |

| Jul-10 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jun-27 | |

| Jun-26 | |

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| Jun-22 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite