|

|

|

|

|||||

|

|

|

Over the last six months, Sixth Street Specialty Lending’s shares have sunk to $21.95, producing a disappointing 7.7% loss - a stark contrast to the S&P 500’s 10% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Sixth Street Specialty Lending, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we're sitting this one out for now. Here are two reasons you should be careful with TSLX and a stock we'd rather own.

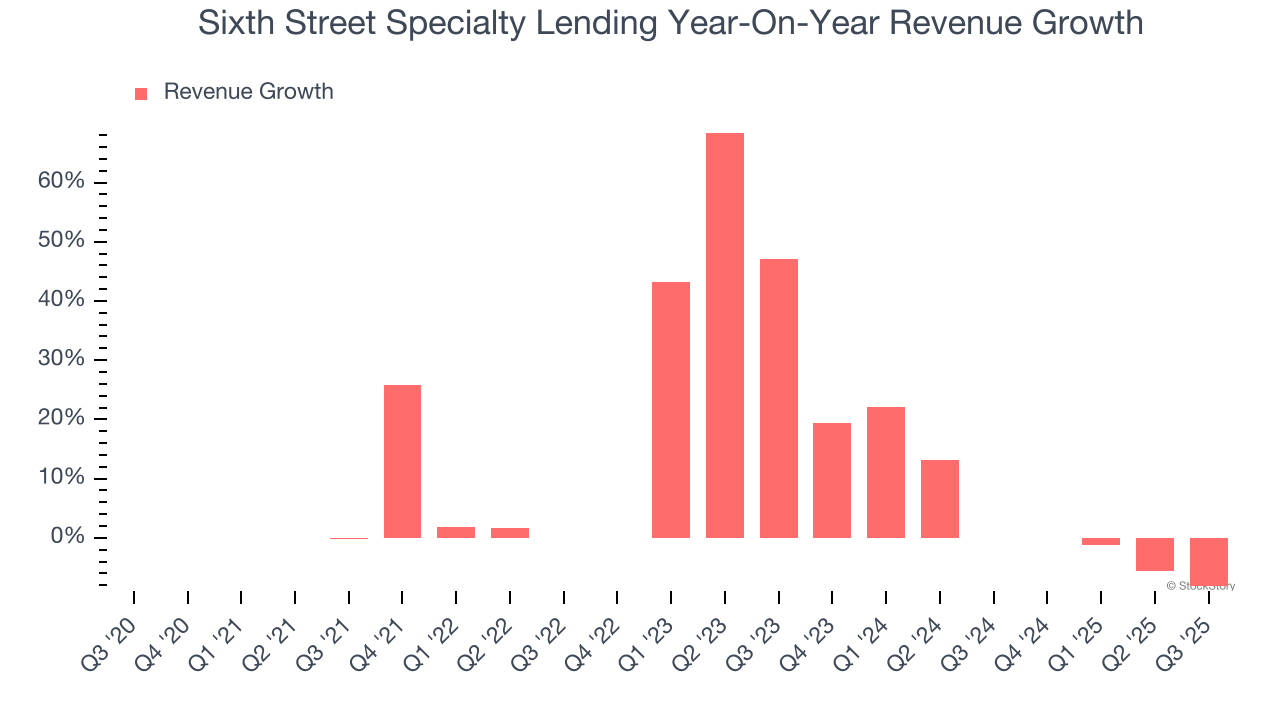

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Sixth Street Specialty Lending’s recent performance shows its demand has slowed as its annualized revenue growth of 5.3% over the last two years was below its five-year trend.

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sixth Street Specialty Lending’s EPS grew at a weak 1% compounded annual growth rate over the last five years, lower than its 11.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We see the value of companies driving economic growth, but in the case of Sixth Street Specialty Lending, we’re out. After the recent drawdown, the stock trades at 11× forward P/E (or $21.95 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-02 | |

| May-07 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-24 | |

| Apr-07 | |

| Apr-02 | |

| Mar-17 | |

| Feb-20 | |

| Feb-19 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite