|

|

|

|

|||||

|

|

|

Over the last six months, Remitly’s shares have sunk to $13.33, producing a disappointing 17.3% loss - a stark contrast to the S&P 500’s 9.6% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is now an opportune time to buy RELY? Find out in our full research report, it’s free.

With Amazon founder Jeff Bezos as an early investor, Remitly (NASDAQ:RELY) is an online platform that enables consumers to safely and quickly send money globally.

As a fintech company, Remitly generates revenue growth by increasing both the number of users on its platform and the number of transactions they execute.

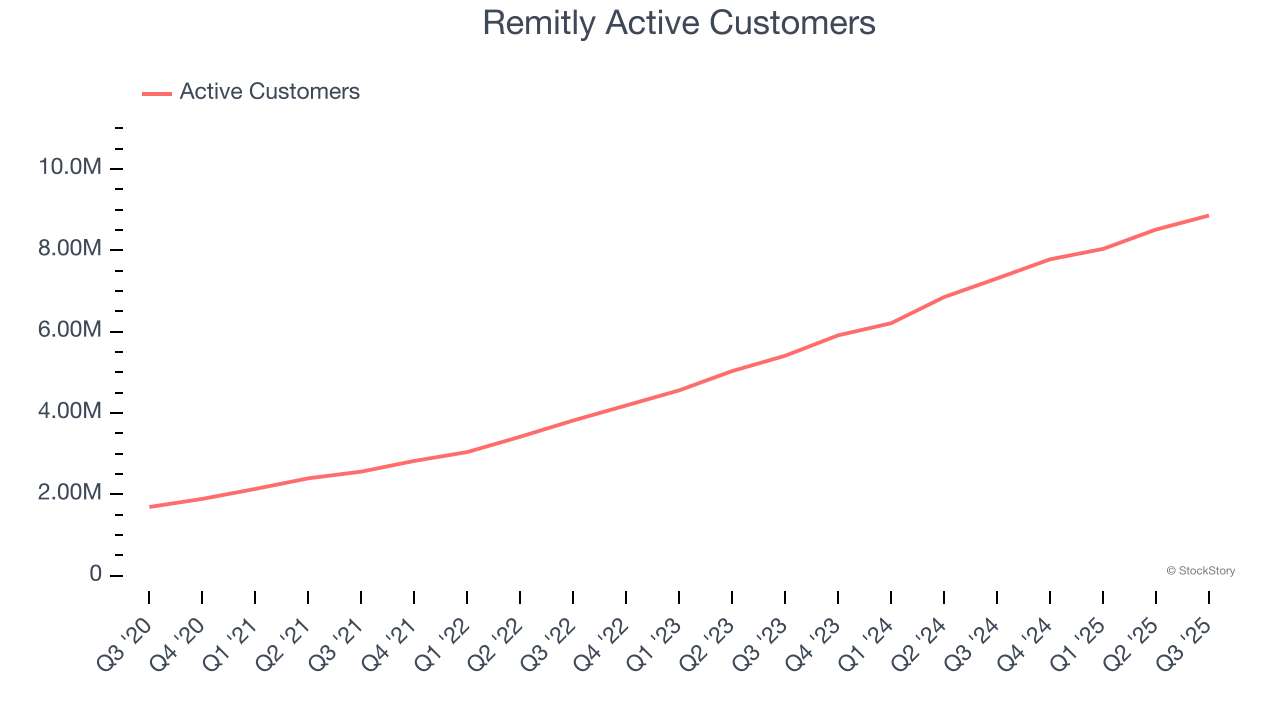

Over the last two years, Remitly’s active customers, a key performance metric for the company, increased by 31.9% annually to 8.86 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

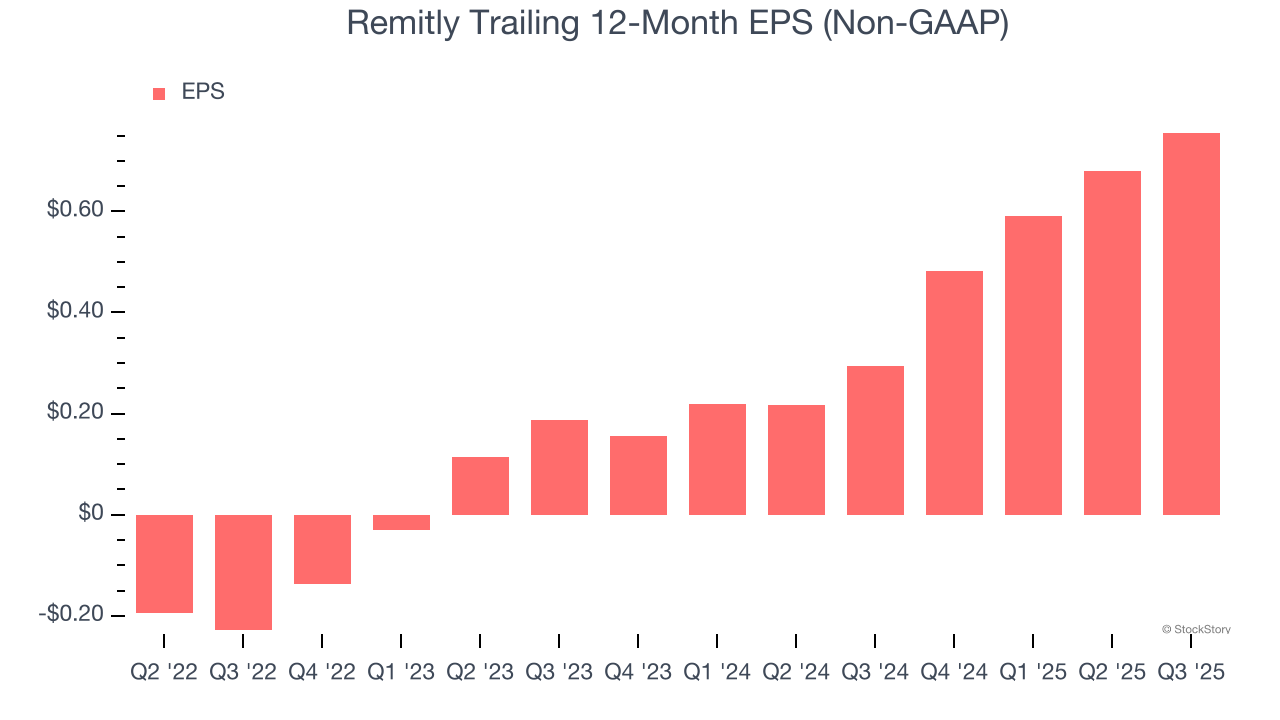

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Remitly’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

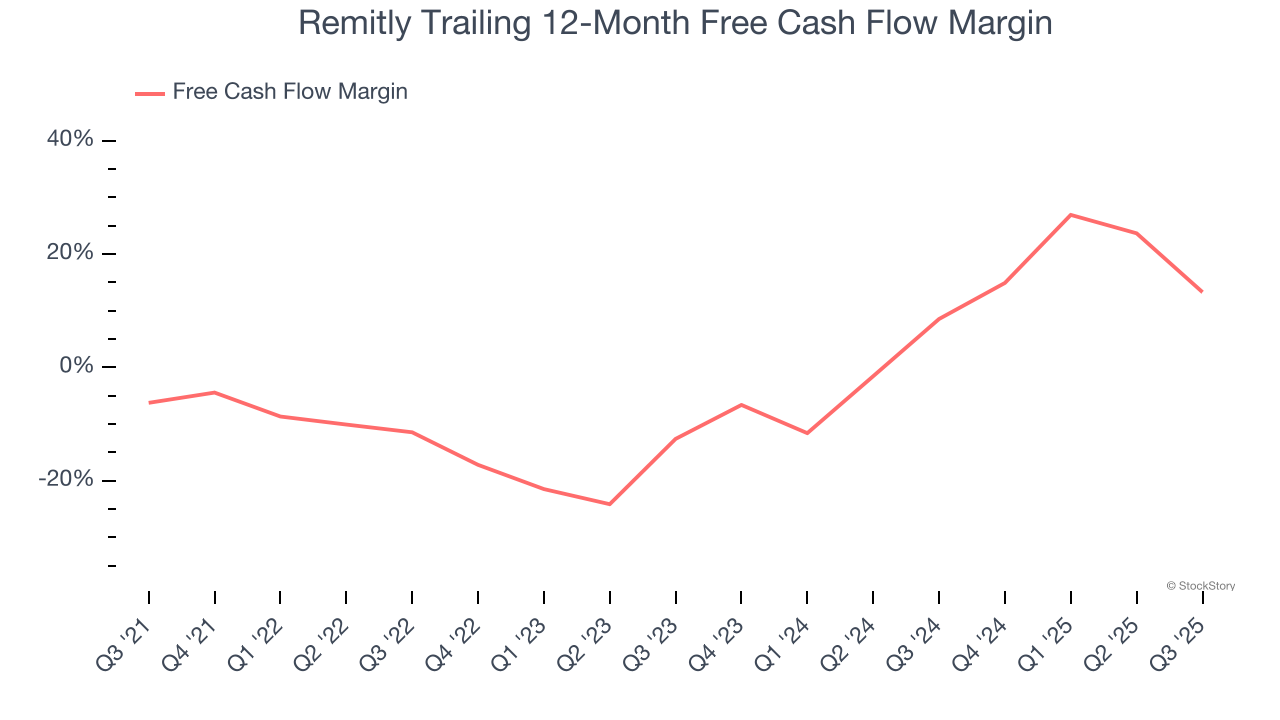

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Remitly’s margin expanded by 24.7 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Remitly’s free cash flow margin for the trailing 12 months was 13.3%.

These are just a few reasons why we think Remitly is a great business. After the recent drawdown, the stock trades at 8.7× forward EV/EBITDA (or $13.33 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| May-12 | |

| May-12 | |

| May-07 | |

| May-07 | |

| May-06 | |

| Apr-29 | |

| Apr-29 | |

| Apr-23 | |

| Apr-22 | |

| Apr-16 | |

| Apr-10 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite