|

|

|

|

|||||

|

|

|

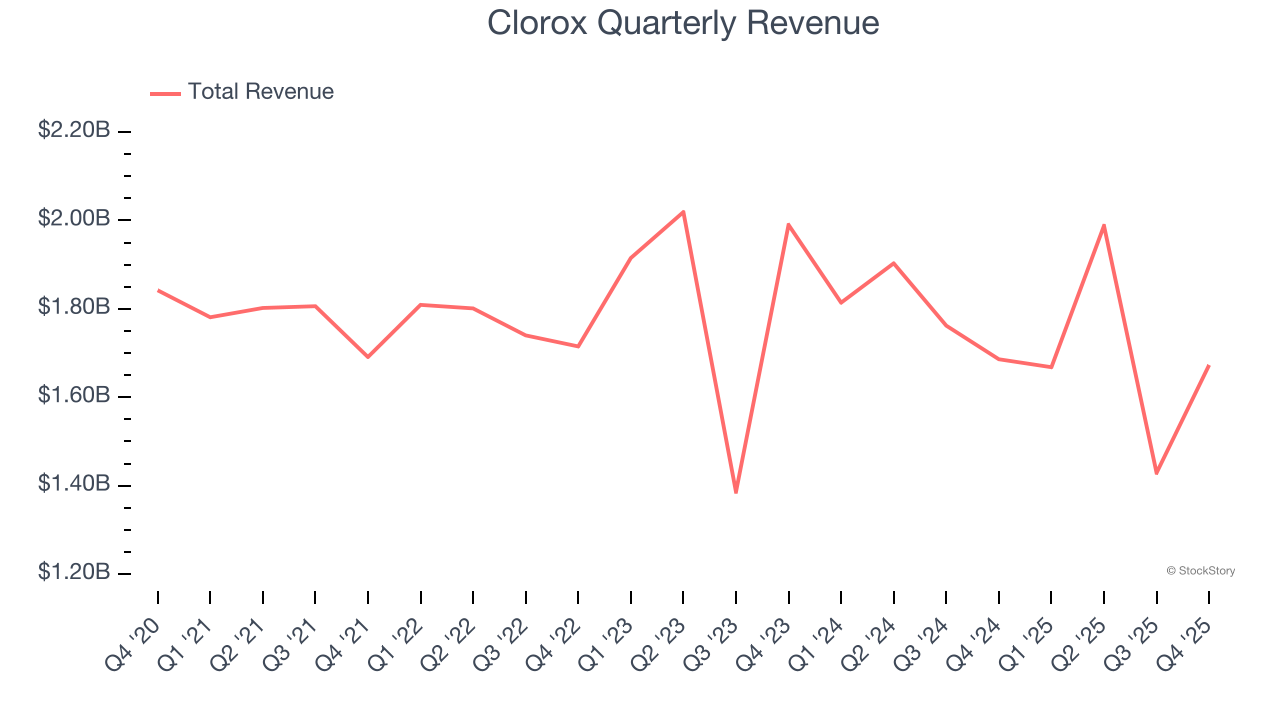

Consumer products giant Clorox (NYSE:CLX) reported Q4 CY2025 results topping the market’s revenue expectations, but sales were flat year on year at $1.67 billion. Its non-GAAP profit of $1.39 per share was 3% below analysts’ consensus estimates.

Is now the time to buy Clorox? Find out by accessing our full research report, it’s free.

"Our second‑quarter results were generally in line with our expectations and reflect continued progress against our strategic priorities. These results support our ability to reaffirm our fiscal year outlook in what remains a challenging and volatile environment," said Chair and CEO Linda Rendle.

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE:CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $6.76 billion in revenue over the past 12 months, Clorox is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. For Clorox to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Clorox’s revenue declined by 1.5% per year over the last three years, a tough starting point for our analysis.

This quarter, Clorox’s $1.67 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products will catalyze better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

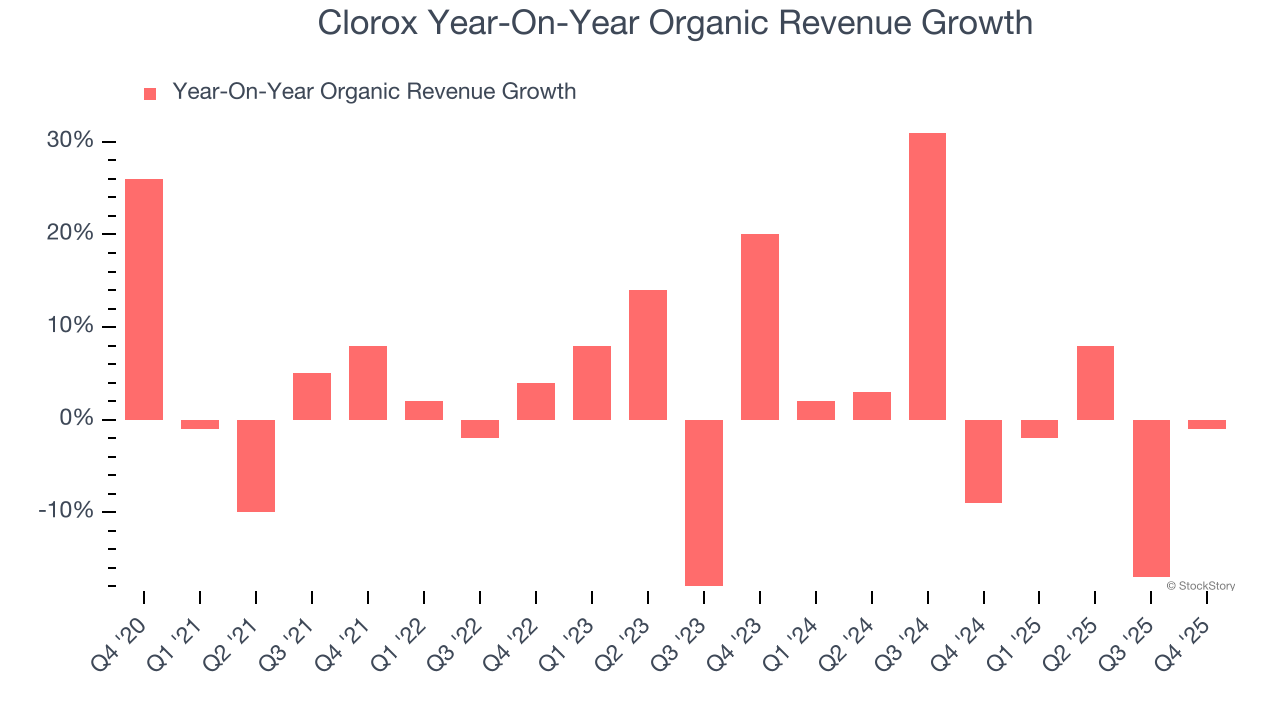

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Clorox’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 1.9%.

In the latest quarter, Clorox’s organic sales fell by 1% year on year. This decline was a reversal from its historical levels. We’ll keep a close eye on the company to see if this turns into a longer-term trend.

It was encouraging to see Clorox beat analysts’ organic revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed and its gross margin fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. Investors were likely hoping for more, and shares traded down 3.4% to $111.05 immediately after reporting.

So do we think Clorox is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-10 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 |

Clorox Projects Tough Fiscal Year with Inflation, Value-Seeking Customers

CLX

The Wall Street Journal

|

| Aug-03 | |

| Aug-03 | |

| Aug-02 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-20 | |

| Jul-15 | |

| Jul-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite