|

|

|

|

|||||

|

|

|

New: Instantly spot drawdowns, dips, insider moves, and breakout themes across Maps and Screener.

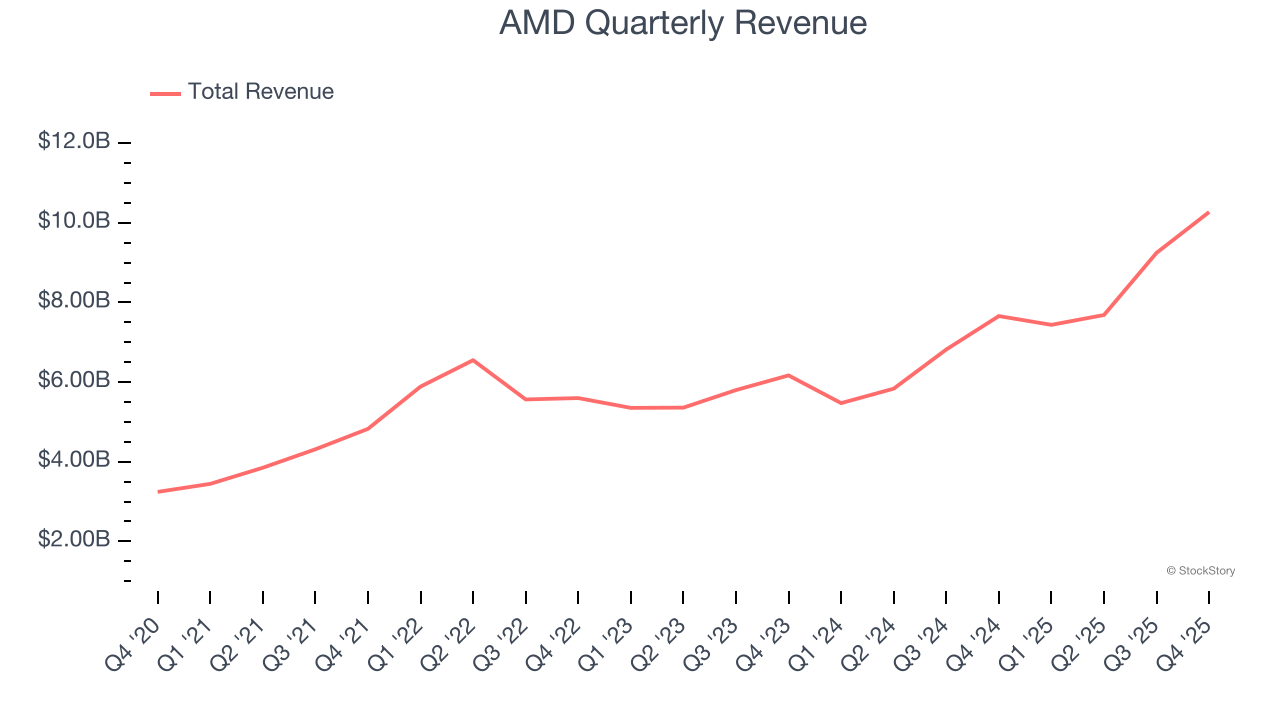

Computer processor maker AMD (NASDAQ:AMD) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 34.1% year on year to $10.27 billion. On top of that, next quarter’s revenue guidance ($9.8 billion at the midpoint) was surprisingly good and 4.3% above what analysts were expecting. Its non-GAAP profit of $1.53 per share was 16% above analysts’ consensus estimates.

Is now the time to buy AMD? Find out by accessing our full research report, it’s free.

“2025 was a defining year for AMD, with record revenue and earnings driven by strong execution and broad-based demand for our high-performance and AI platforms,” said Dr. Lisa Su, AMD chair and CEO.

Founded in 1969 by a group of former Fairchild semiconductor executives led by Jerry Sanders, Advanced Micro Devices (NASDAQ:AMD) is one of the leading designers of computer processors and graphics chips used in PCs and data centers.

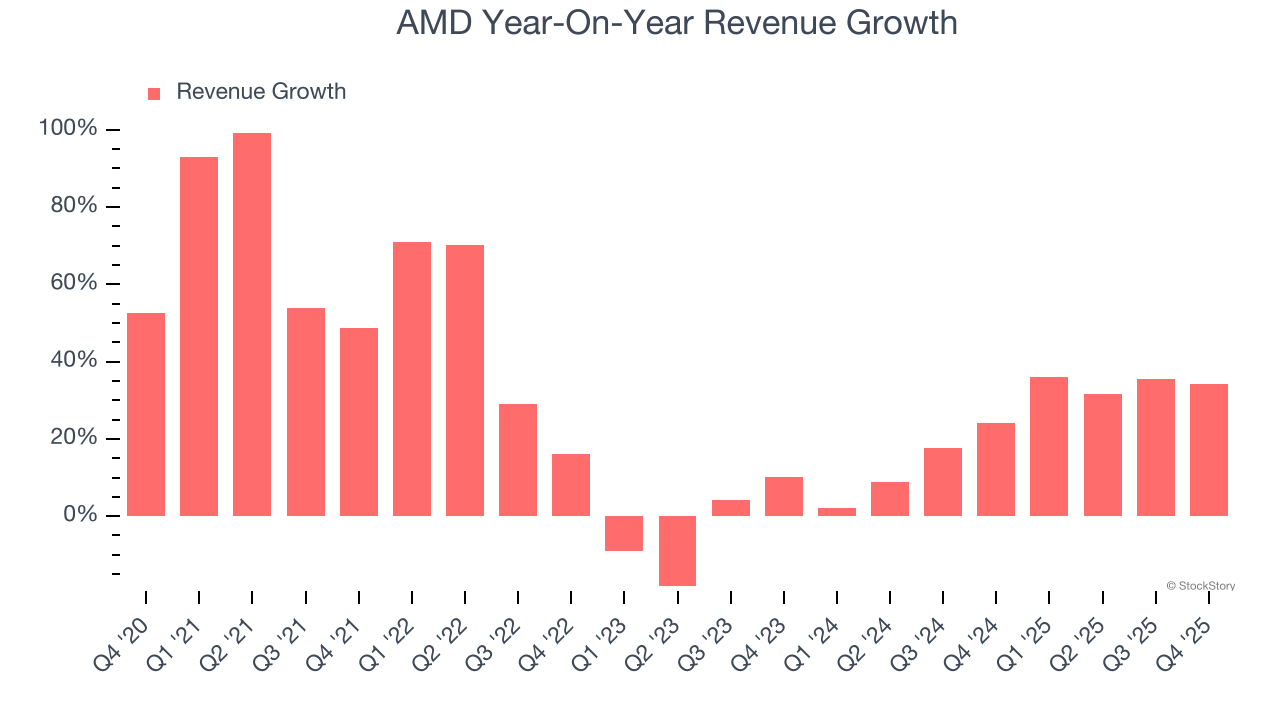

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, AMD’s 28.8% annualized revenue growth over the last five years was incredible. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers, a great starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. AMD’s annualized revenue growth of 23.6% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, AMD reported wonderful year-on-year revenue growth of 34.1%, and its $10.27 billion of revenue exceeded Wall Street’s estimates by 6%. Beyond the beat, this marks 10 straight quarters of growth, showing that the current upcycle has had a good run - a typical upcycle usually lasts 8-10 quarters. Company management is currently guiding for a 31.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 31.4% over the next 12 months, an improvement versus the last two years. This projection is eye-popping for a company of its scale and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

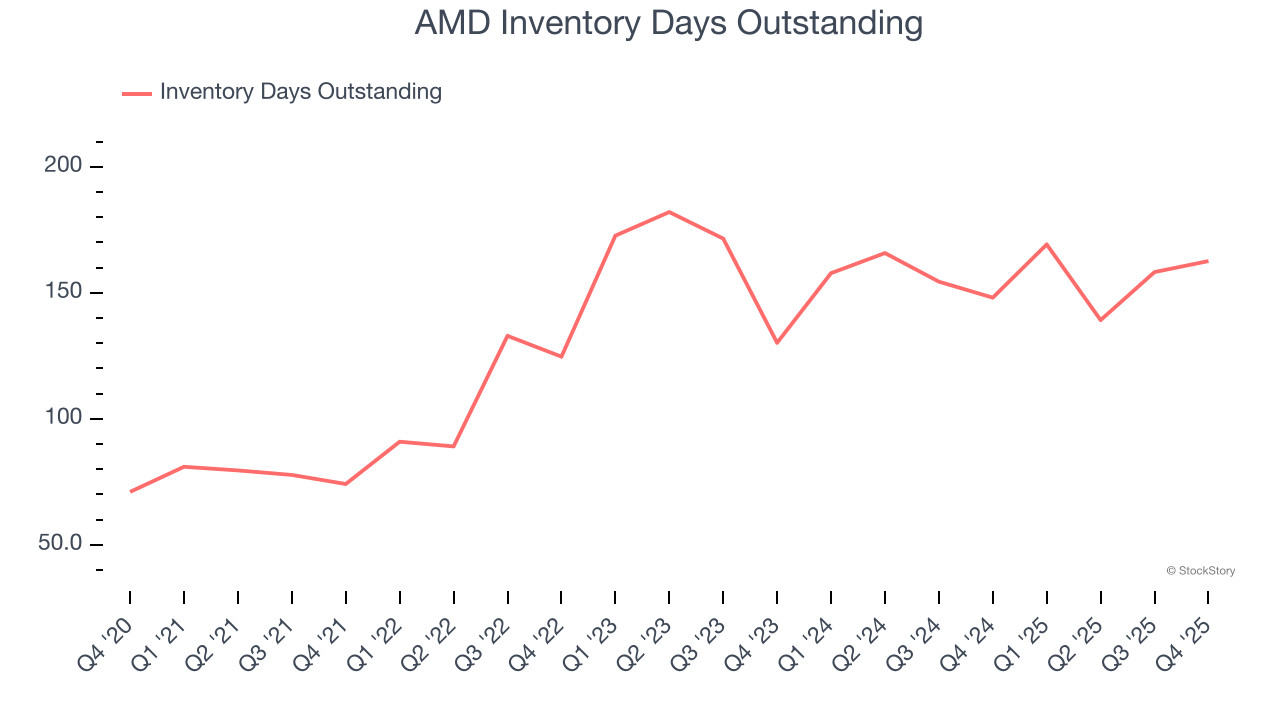

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, AMD’s DIO came in at 163, which is 30 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

It was good to see AMD beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its inventory levels increased. Zooming out, we think this was a solid print. The market seemed to be hoping for more, and the stock traded down 4.1% to $232.95 immediately after reporting.

Big picture, is AMD a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| 3 min | |

| 25 min | |

| 38 min | |

| 51 min | |

| 56 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite