|

|

|

|

|||||

|

|

|

Figma made creating and collaborating on design products much more seamless than previous options.

Figma customers spending at least $100,000 annually have grown significantly.

Even after declining, it's hard to justify Figma's current valuation.

Last year wasn't a huge year for initial public offerings (IPOs), but one of the more anticipated ones came from design company Figma (NYSE: FIG). Its IPO price was $33 per share on July 31, and by the next day, it had skyrocketed to $122. Unfortunately, the stock has fallen about 80% and trades at about $24 (as of Feb. 2).

Considering the hype surrounding Figma, should investors take the opportunity to invest now that it's so far below its all-time high? Or is this a situation where excitement obscured the actual business? Let's take a look.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Think about how Google Docs made collaborating on documents in real time much more efficient than older software. Now, imagine that for user interface (UI) and user experience (UX) design.

Instead of sending designs back and forth, Figma lets teams build together in real time, in the cloud. It seems simple on the surface, but even legacy companies like Adobe didn't perfect this approach.

Much of Figma's hype has come from becoming the go-to platform to bridge the gap between designers and developers.

The test of Figma's business model is the number of customers it can attract and retain. People and businesses often try a product, but retention matters for stability and long-term growth.

Figma ended its last-reported quarter (ended Sept. 30) with 1,262 customers with an annual recurring revenue (ARR) of at least $100,000, and 12,910 customers with an ARR of at least $10,000. These were up 385 and 3,148 year over year, respectively.

Any new customers are worth celebrating, but the increase in customers spending more than $100,000 is noteworthy because those companies usually stick around longer and would have Figma more ingrained in their design infrastructure. It's also a good sign that about 30% of them were creating on Figma Make (Figma's AI tool) weekly.

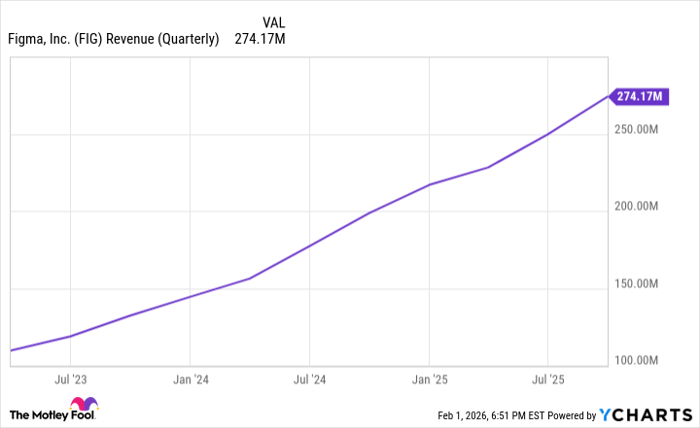

The growing customer base was reflected in Figma's financials in its latest quarter. Revenue rose 38% from a year earlier to $274.2 million. Its annual revenue run rate -- which is current quarterly revenue multiplied by four -- crossed the billion-dollar mark for the first time.

It had an operating loss of about $1.1 billion in the quarter, but most of that was due to the $975.7 million it spent on one-time stock-based compensation. This is expected with newly public companies because executives and early employees tend to vest their equity or receive payouts shortly after the company goes public.

Figma is continuing to reinvest heavily in its business, so profitability isn't the immediate priority. What matters more right now is that Figma's cash flow remains positive.

FIG Revenue (Quarterly) data by YCharts

To start February, Figma is trading at almost 70 times its projected earnings for the next 12 months. It's far below the 329 it traded at in its 2025 peak, but it's still expensive. That's much more than Nvidia's 25, Amazon's 29, and Meta Platforms' 24.

We've seen popular software stocks trade at premiums in recent years (Zoom, Snowflake, to cite a couple), and in most cases, they've experienced sharp and long-running declines. Being down 80% could mean that Figma has already gone through its great reset, but there could also be more downside. You don't want to invest simply because an expensive stock is cheaper than before.

Figma definitely has a good product; the proof is in its growing high-dollar customers and retention. However, given that Figma's stock remains richly valued, it falls in the wait-and-see category for me.

Before you buy stock in Figma, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Figma wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $446,319!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,137,827!*

Now, it’s worth noting Stock Advisor’s total average return is 932% — a market-crushing outperformance compared to 197% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 4, 2026.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Amazon, Figma, Meta Platforms, Nvidia, Snowflake, and Zoom Communications. The Motley Fool recommends the following options: long January 2028 $330 calls on Adobe and short January 2028 $340 calls on Adobe. The Motley Fool has a disclosure policy.

| Aug-07 | |

| Aug-06 | |

| Aug-06 |

Figma's AI credits paved the way for huge revenue growth, CFO explains

FIG -14.85%

Yahoo Finance Video

|

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-01 | |

| Jul-28 | |

| Jul-16 | |

| Jul-15 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite