|

|

|

|

|||||

|

|

|

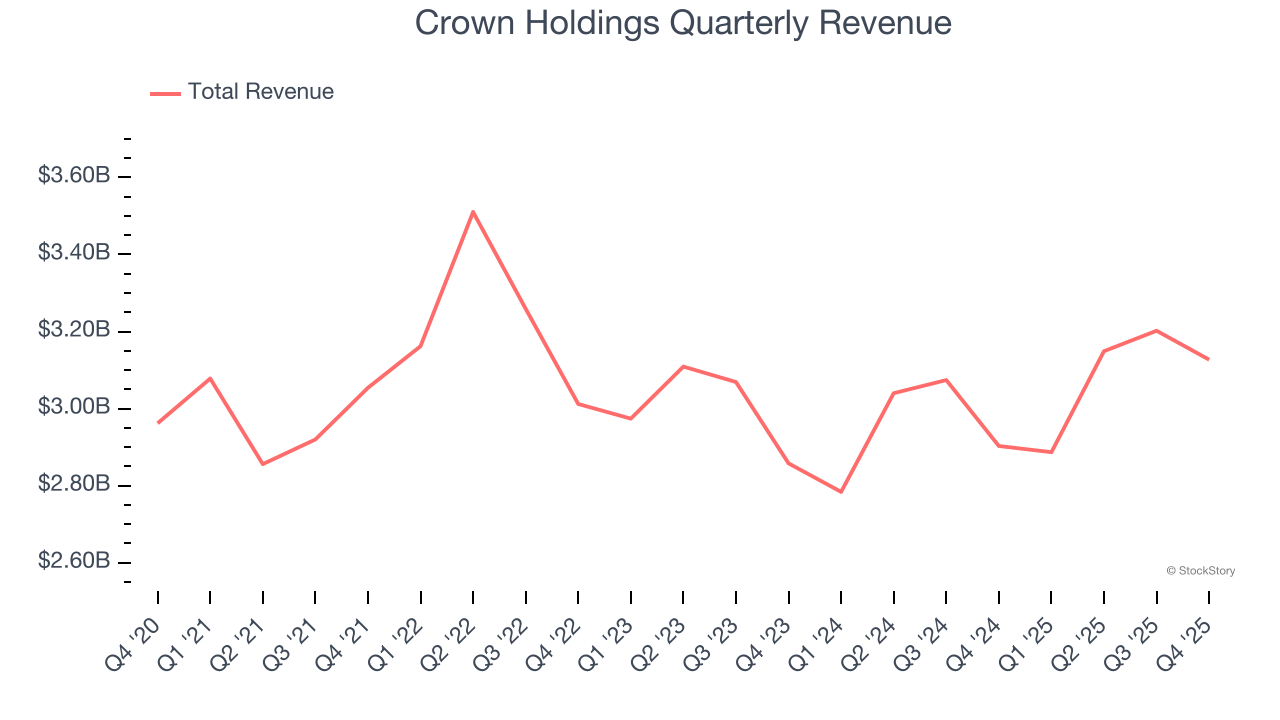

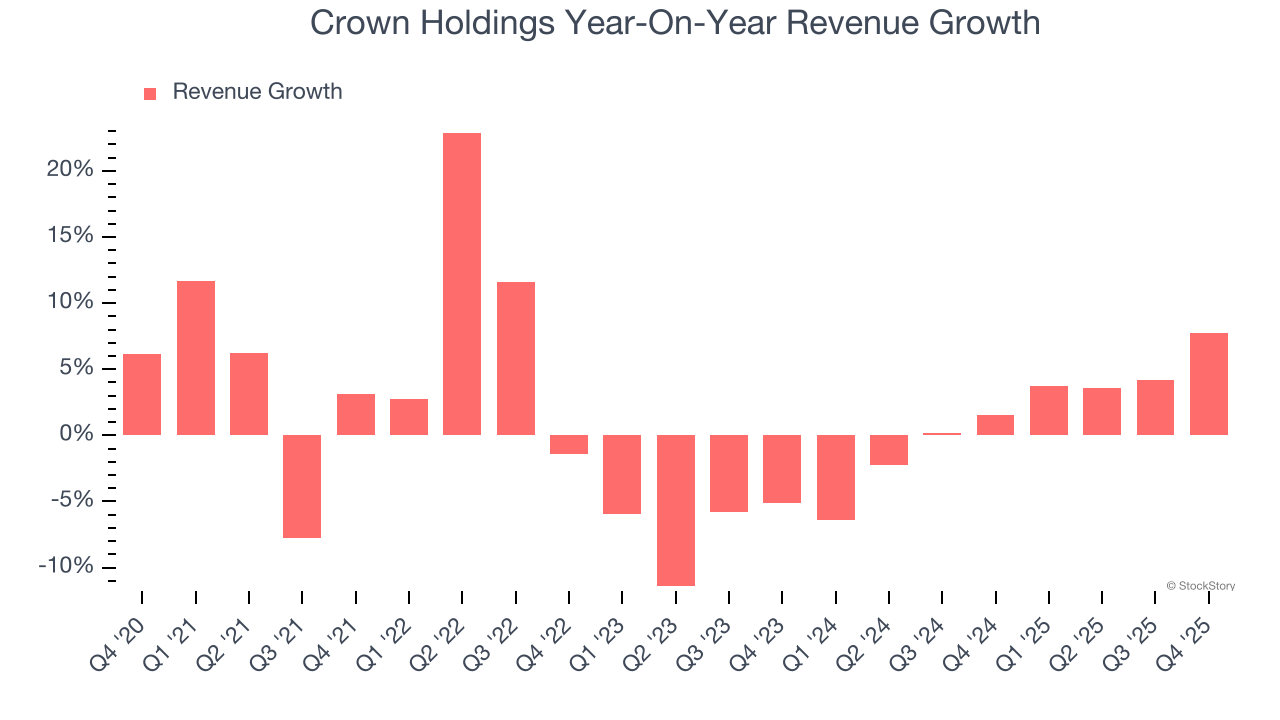

Metal packaging products manufacturer Crown Holdings (NYSE:CCK) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.7% year on year to $3.13 billion. Its non-GAAP profit of $1.74 per share was 2.2% above analysts’ consensus estimates.

Is now the time to buy Crown Holdings? Find out by accessing our full research report, it’s free.

Timothy J. Donahue, Chairman, President and Chief Executive Officer, stated "The Company continued its strong momentum during the fourth quarter to complete an excellent year. In 2025, the Company achieved record adjusted EBITDA of approximately $2.1 billion, an 8% increase over 2024. Over the past three years, Crown has increased adjusted EBITDA by 20%, supported by our culture of continuous improvement and focused capacity expansions. Solid performance throughout the global beverage can and the North American tinplate businesses in 2025 drove segment income expansion of over 8%, building on the strong growth of 6% and 7% delivered in 2024 and 2023, respectively.

Formerly Crown Cork & Seal, Crown Holdings (NYSE:CCK) produces packaging products for consumer marketing companies, including food, beverage, household, and industrial products.

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Crown Holdings grew its sales at a weak 1.3% compounded annual growth rate. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Crown Holdings’s annualized revenue growth of 1.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Crown Holdings reported year-on-year revenue growth of 7.7%, and its $3.13 billion of revenue exceeded Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 2.1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

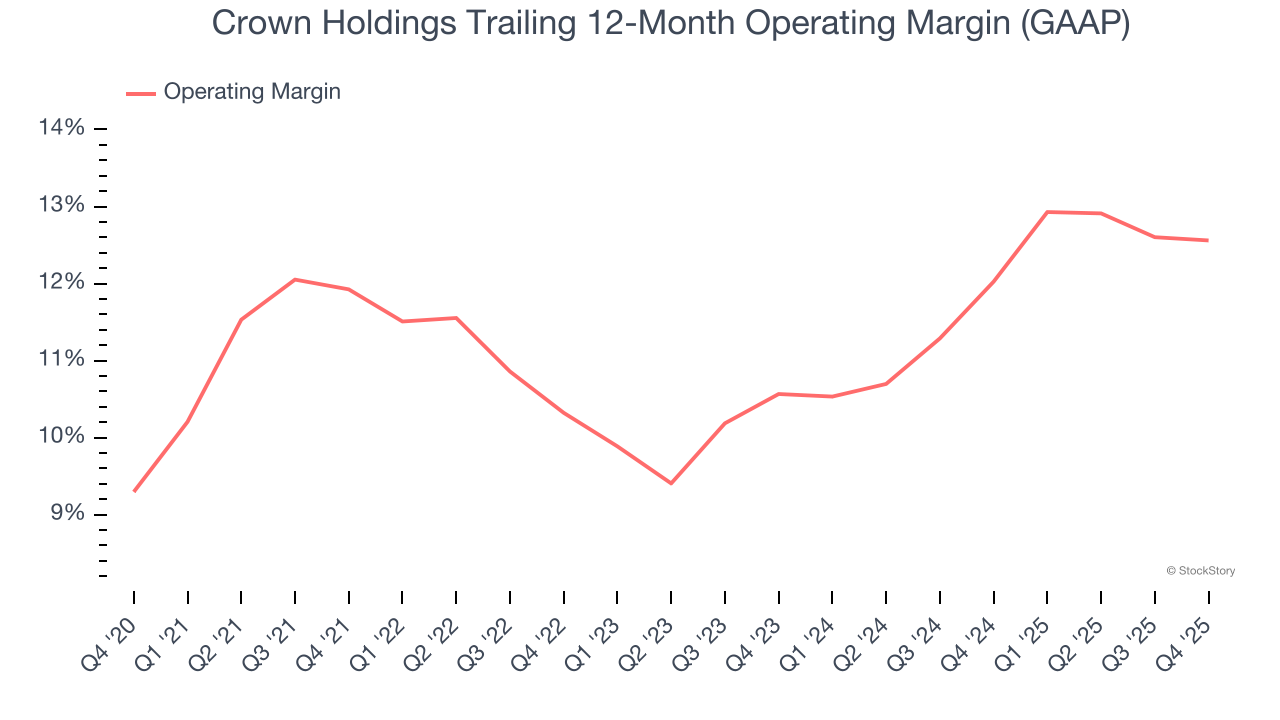

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Crown Holdings’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 11.5% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Crown Holdings’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but we’re still happy with Crown Holdings’s performance considering most Industrial Packaging companies saw their margins plummet.

This quarter, Crown Holdings generated an operating margin profit margin of 12%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

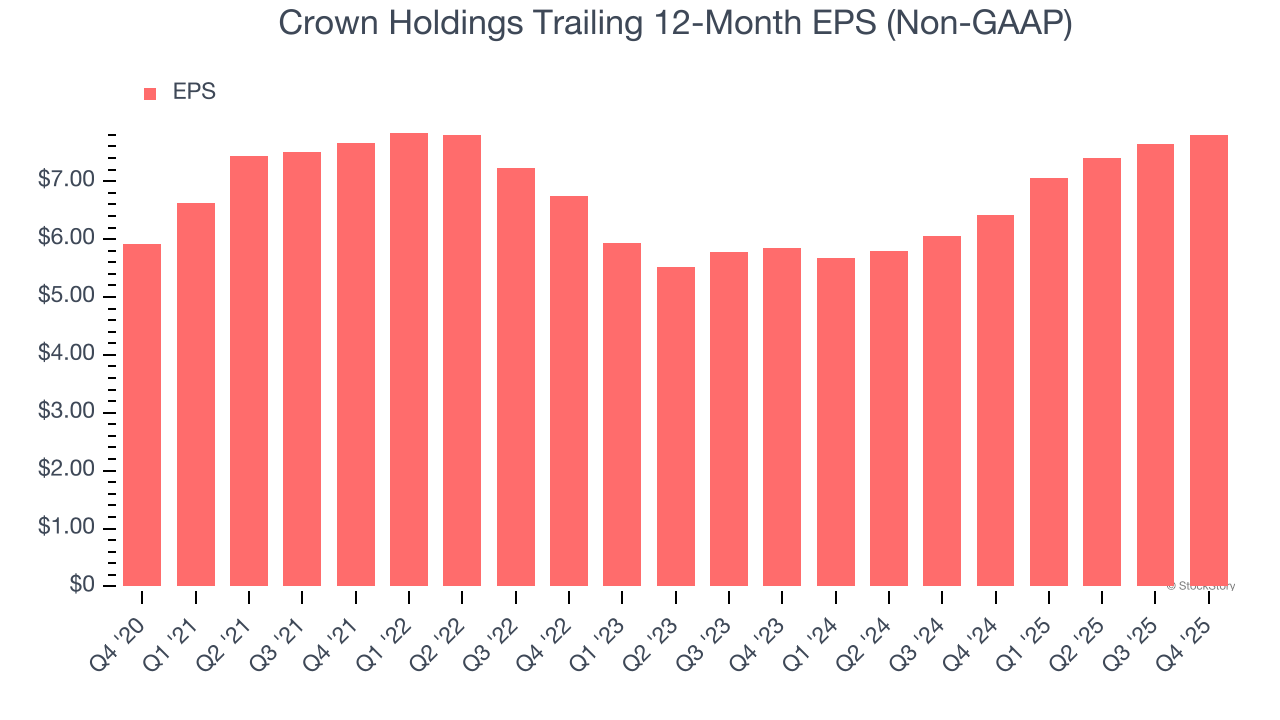

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Crown Holdings’s EPS grew at an unimpressive 5.7% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.3% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

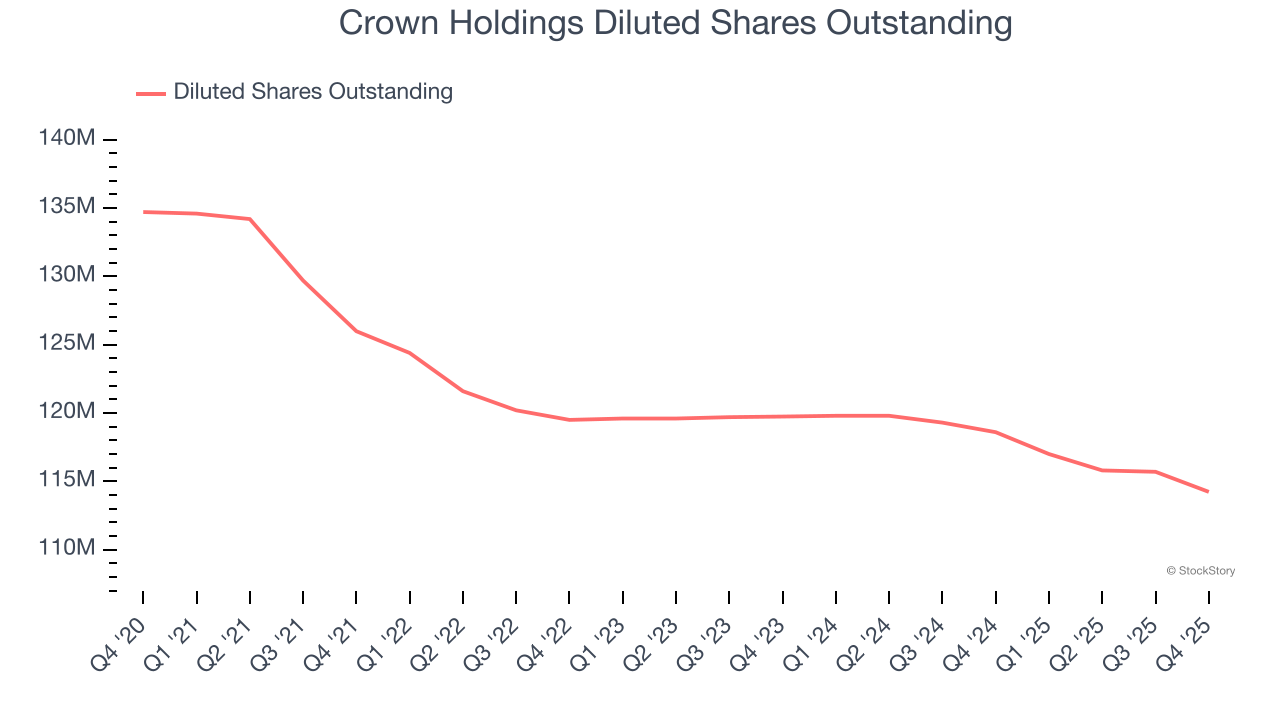

Diving into the nuances of Crown Holdings’s earnings can give us a better understanding of its performance. A five-year view shows that Crown Holdings has repurchased its stock, shrinking its share count by 15.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Crown Holdings, its two-year annual EPS growth of 15.5% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Crown Holdings reported adjusted EPS of $1.74, up from $1.59 in the same quarter last year. This print beat analysts’ estimates by 2.2%. Over the next 12 months, Wall Street expects Crown Holdings’s full-year EPS of $7.80 to grow 5.4%.

We were impressed by how significantly Crown Holdings blew past analysts’ revenue expectations this quarter. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 1.7% to $113.23 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| 2 hours | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-13 | |

| Jun-24 | |

| Jun-22 | |

| Jun-02 | |

| Apr-30 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite