|

|

|

|

|||||

|

|

|

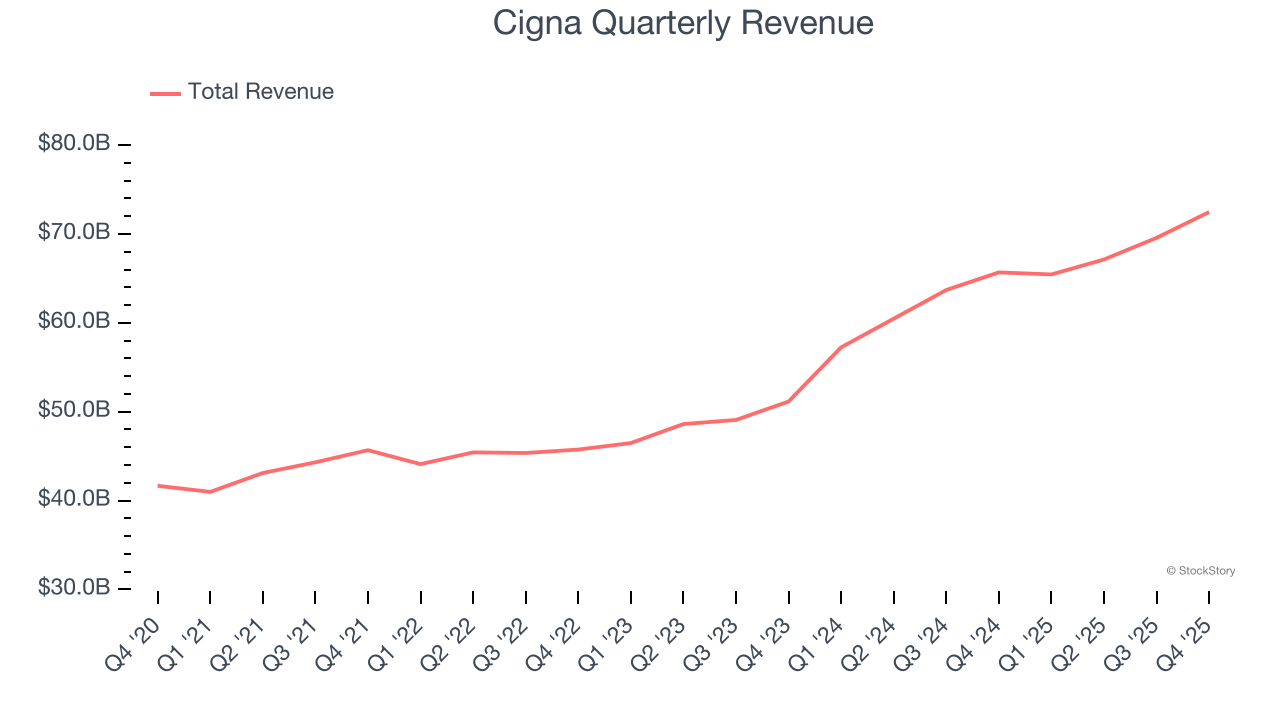

Health insurance company Cigna (NYSE:CI) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 10.3% year on year to $72.47 billion. On the other hand, the company’s full-year revenue guidance of $280 billion at the midpoint came in 0.9% below analysts’ estimates. Its non-GAAP profit of $8.08 per share was 2.5% above analysts’ consensus estimates.

Is now the time to buy Cigna? Find out by accessing our full research report, it’s free.

"In 2025, we expanded access and support, lowered costs, and improved transparency for our customers and patients," said David M. Cordani, chairman and CEO of The Cigna Group.

With roots dating back to 1792 and serving millions of customers across the globe, The Cigna Group (NYSE:CI) provides healthcare services through its Evernorth Health Services and Cigna Healthcare segments, offering pharmacy benefits, specialty care, and medical plans.

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Cigna grew its sales at a decent 11.4% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

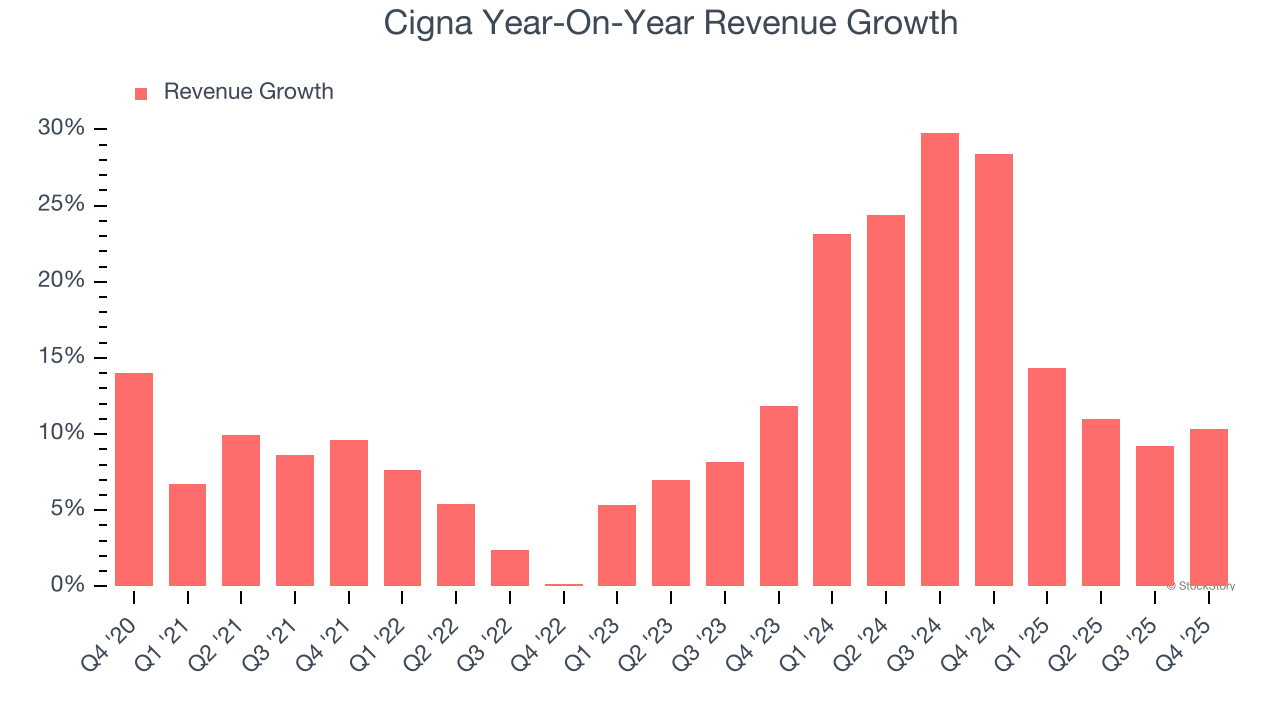

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Cigna’s annualized revenue growth of 18.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

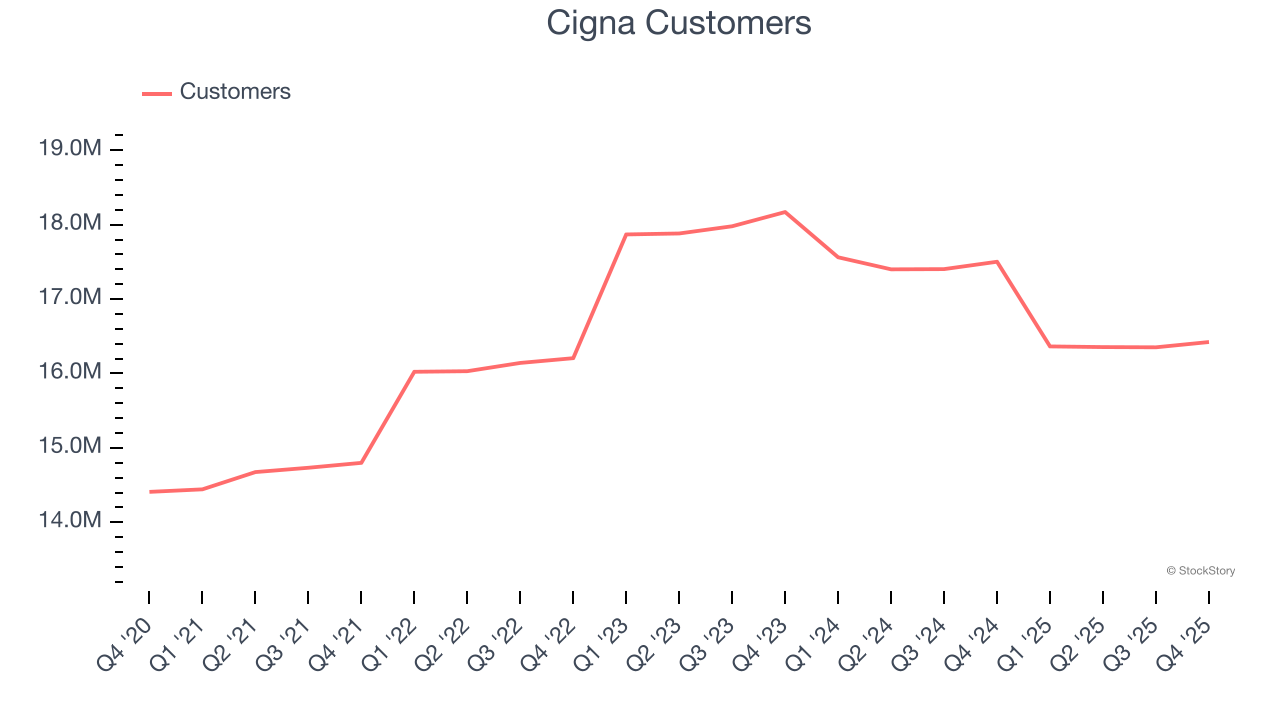

We can dig further into the company’s revenue dynamics by analyzing its number of customers, which reached 16.42 million in the latest quarter. Over the last two years, Cigna’s customer base averaged 4.5% year-on-year declines. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Cigna reported year-on-year revenue growth of 10.3%, and its $72.47 billion of revenue exceeded Wall Street’s estimates by 3.7%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

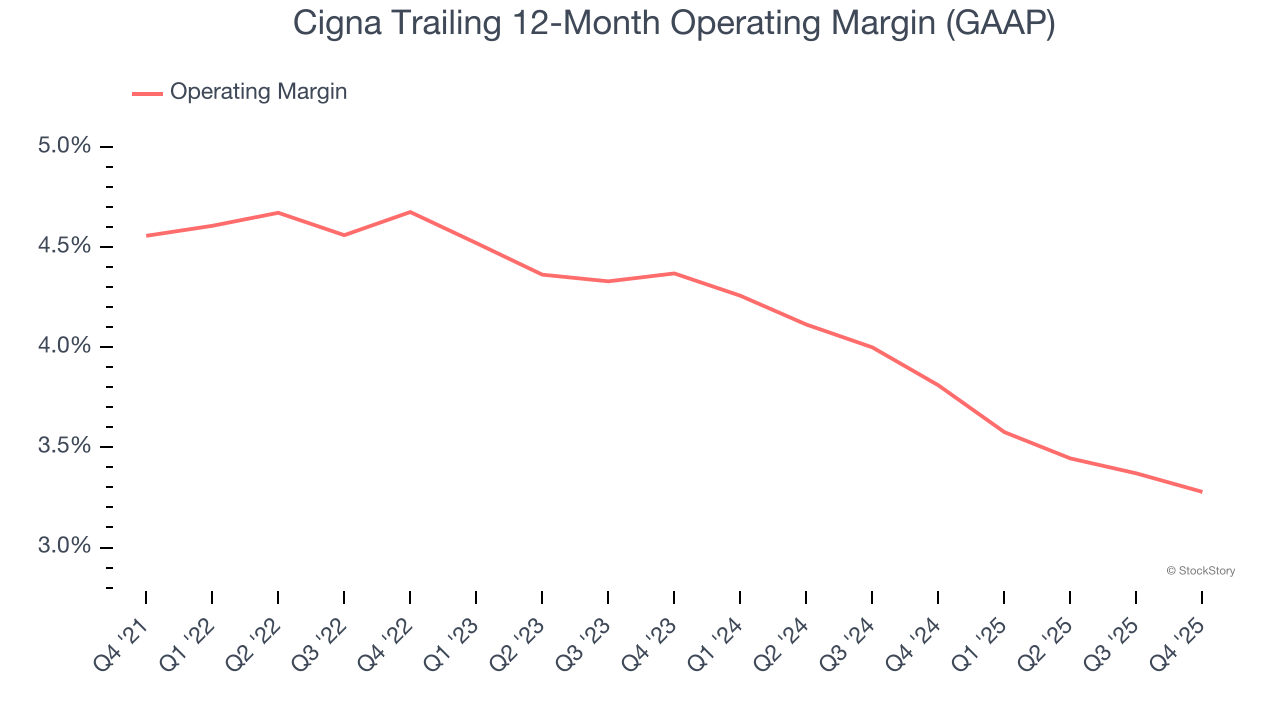

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Cigna was profitable over the last five years but held back by its large cost base. Its average operating margin of 4% was weak for a healthcare business.

Looking at the trend in its profitability, Cigna’s operating margin decreased by 1.3 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.1 percentage points. We still like Cigna but would like to see some improvement in the future.

In Q4, Cigna generated an operating margin profit margin of 3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

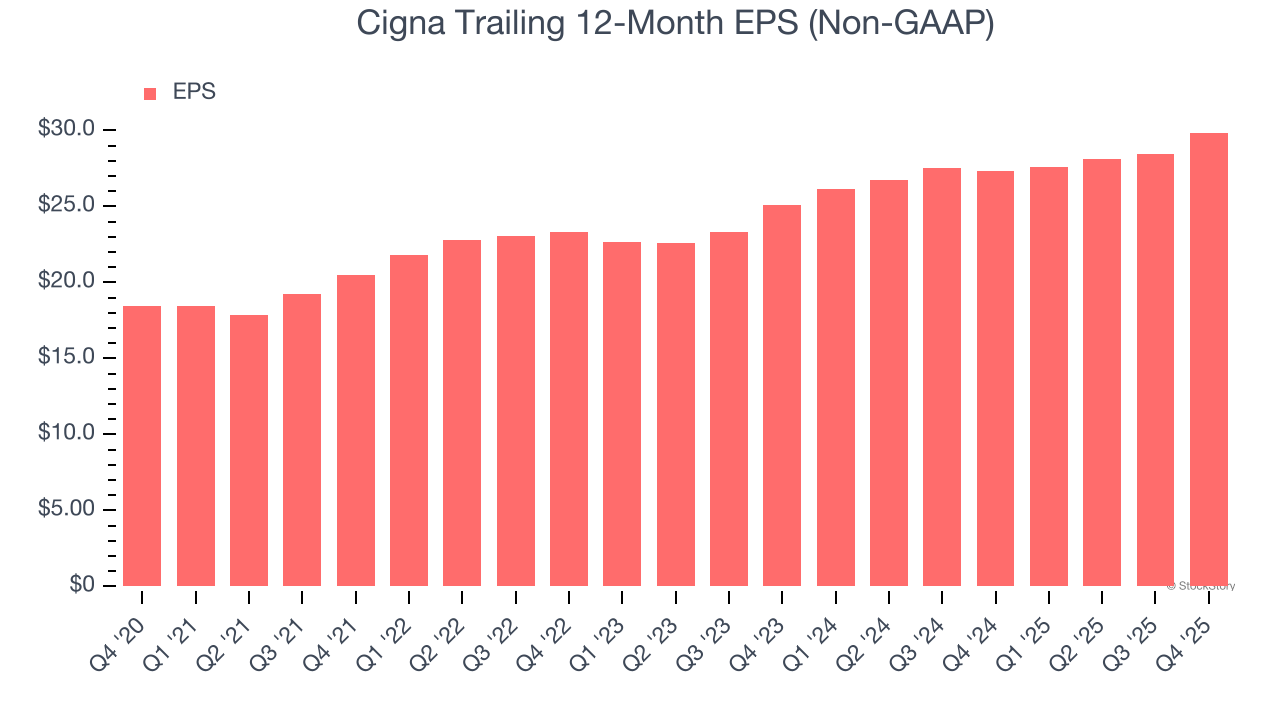

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Cigna’s remarkable 10.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, Cigna reported adjusted EPS of $8.08, up from $6.64 in the same quarter last year. This print beat analysts’ estimates by 2.5%. Over the next 12 months, Wall Street expects Cigna’s full-year EPS of $29.85 to grow 1.6%.

We enjoyed seeing Cigna beat analysts’ revenue expectations this quarter. We were also happy its customer base was in line with Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed and its full-year EPS guidance was in line with Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $270.78 immediately after reporting.

So should you invest in Cigna right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| 1 hour | |

| 1 hour | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jul-03 | |

| Jul-01 | |

| Jun-25 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite