|

|

|

|

|||||

|

|

|

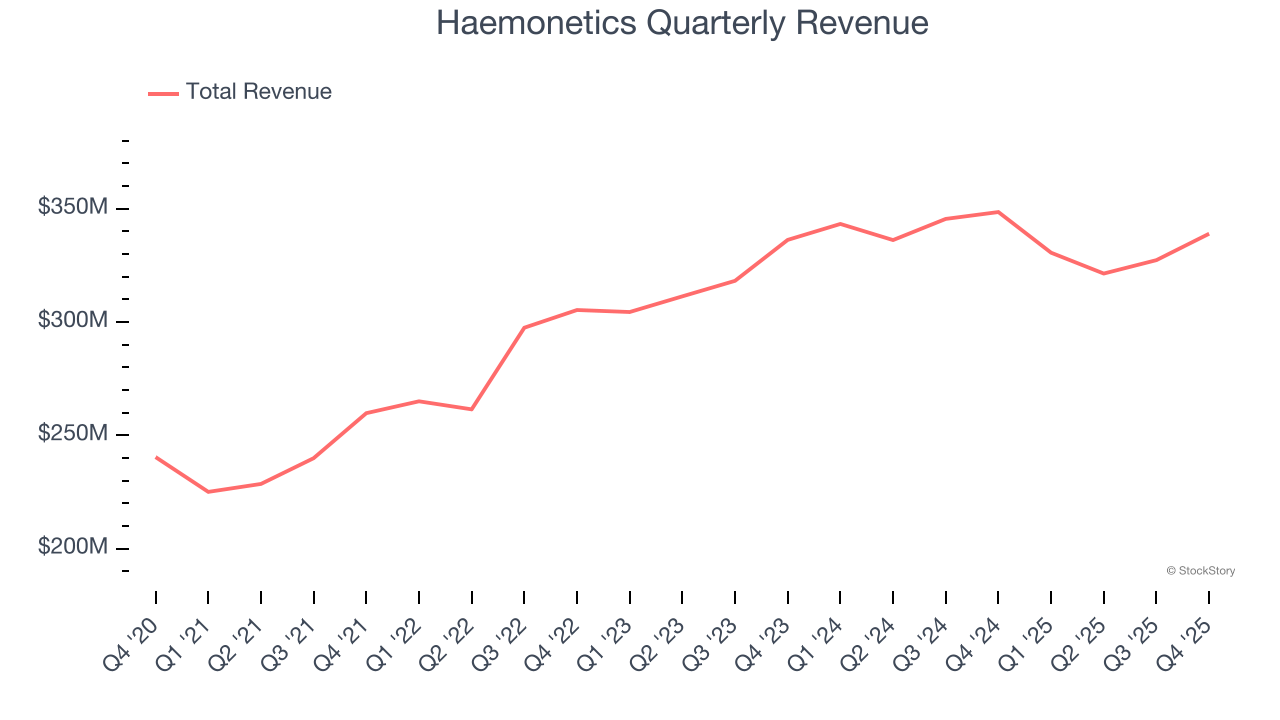

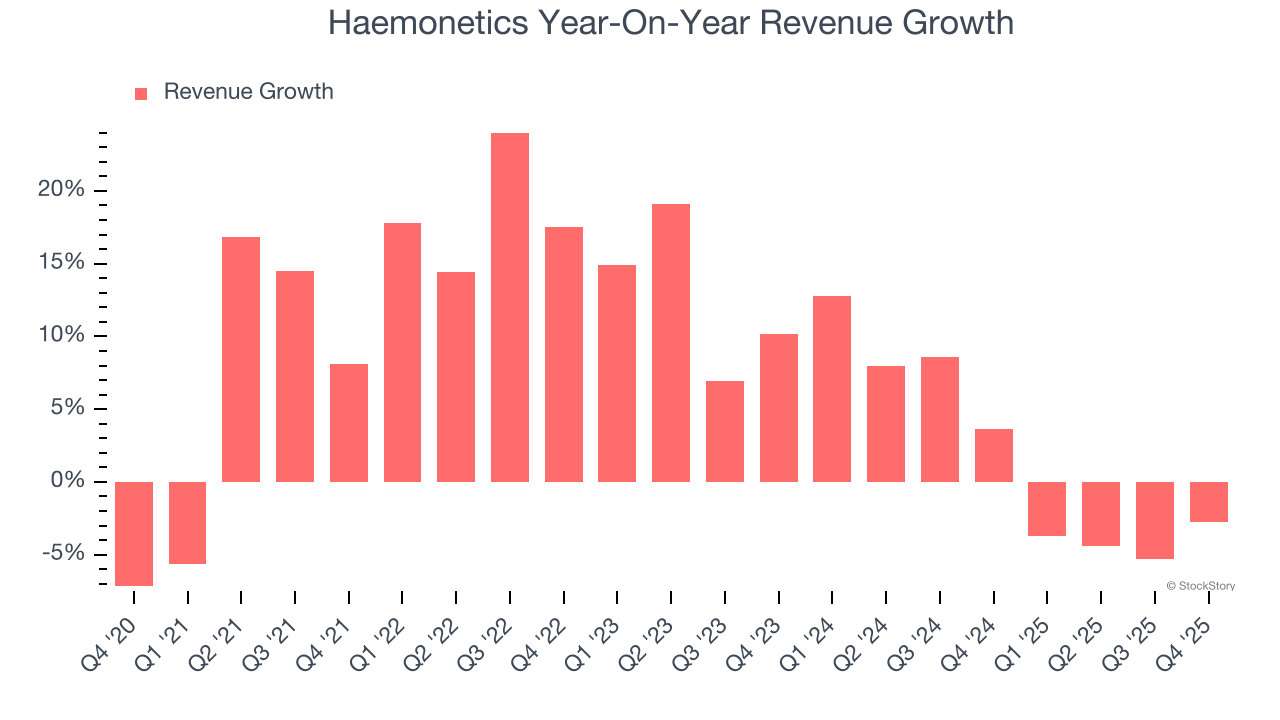

Blood products company Haemonetics (NYSE:HAE). beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 2.7% year on year to $339 million. Its non-GAAP profit of $1.31 per share was 4.8% above analysts’ consensus estimates.

Is now the time to buy Haemonetics? Find out by accessing our full research report, it’s free.

With roots dating back to 1971 and a mission to improve blood-related healthcare, Haemonetics (NYSE:HAE) provides specialized medical devices and software for blood collection, processing, and management across plasma centers, blood banks, and hospitals.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Haemonetics’s 8.3% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Haemonetics’s recent performance shows its demand has slowed as its annualized revenue growth of 1.9% over the last two years was below its five-year trend.

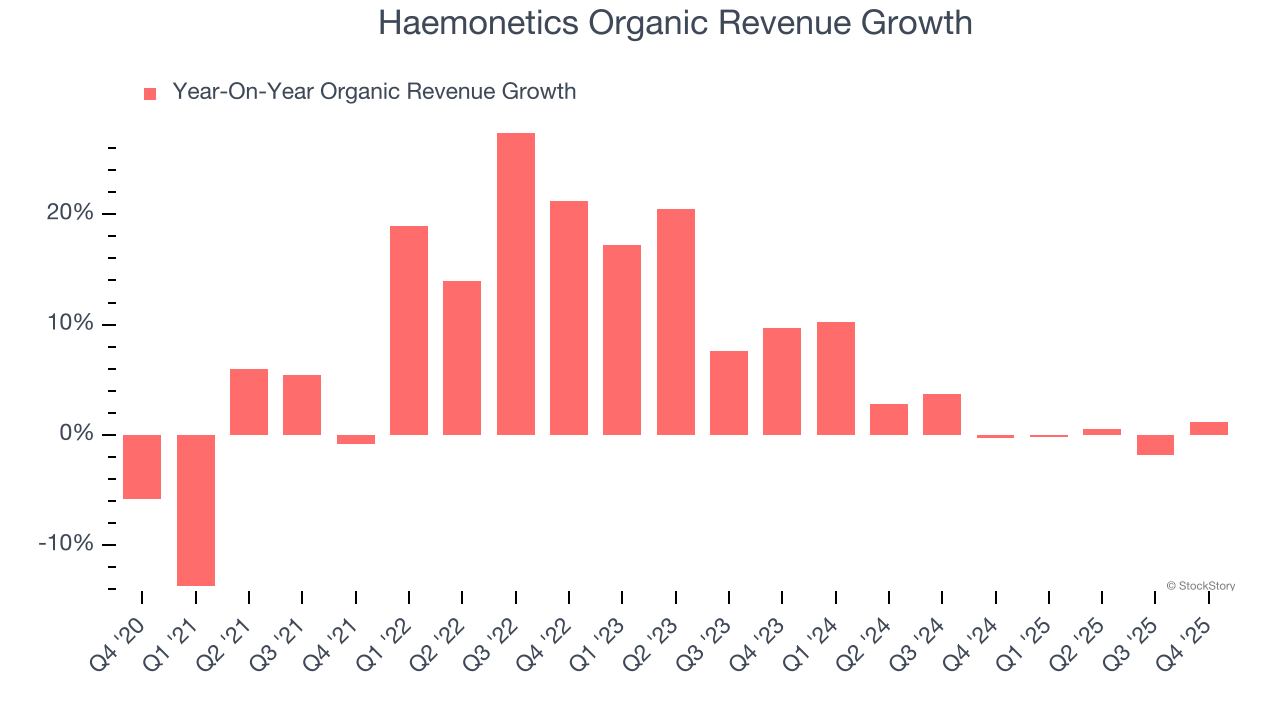

Haemonetics also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Haemonetics’s organic revenue averaged 2% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Haemonetics’s revenue fell by 2.7% year on year to $339 million but beat Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

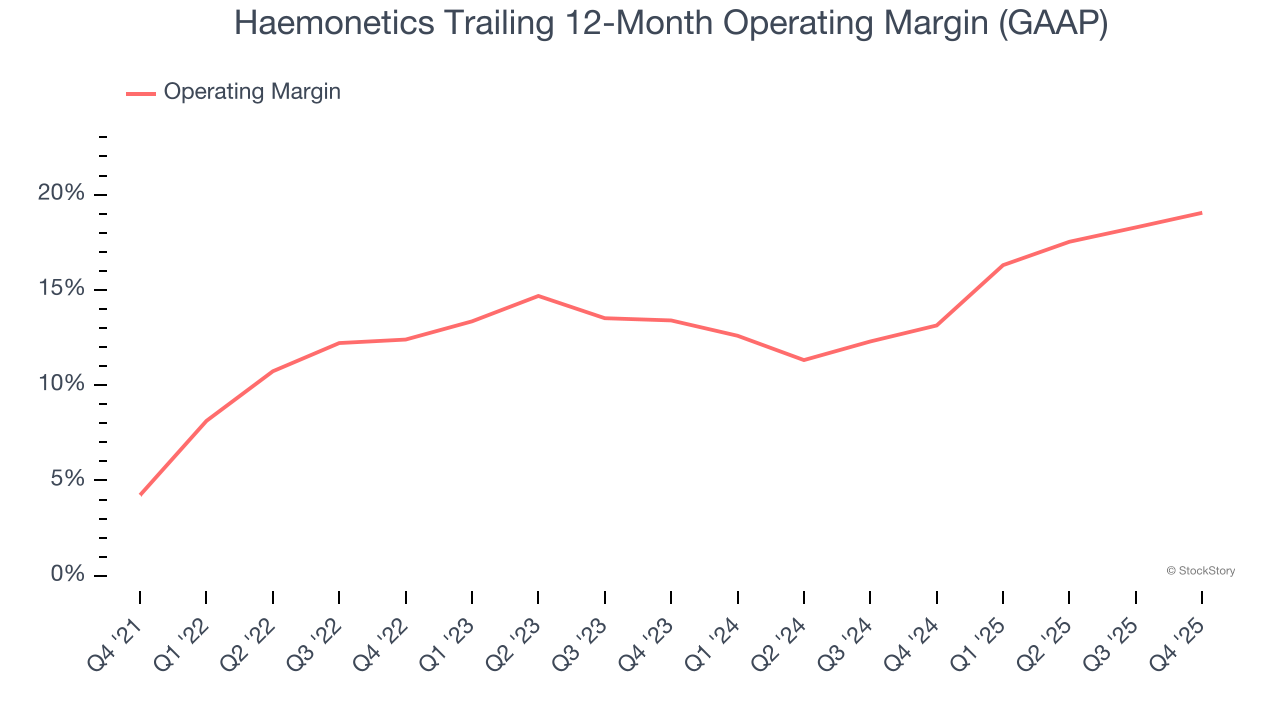

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Haemonetics has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 12.9%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Haemonetics’s operating margin rose by 14.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 5.6 percentage points on a two-year basis.

This quarter, Haemonetics generated an operating margin profit margin of 19.9%, up 2.9 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

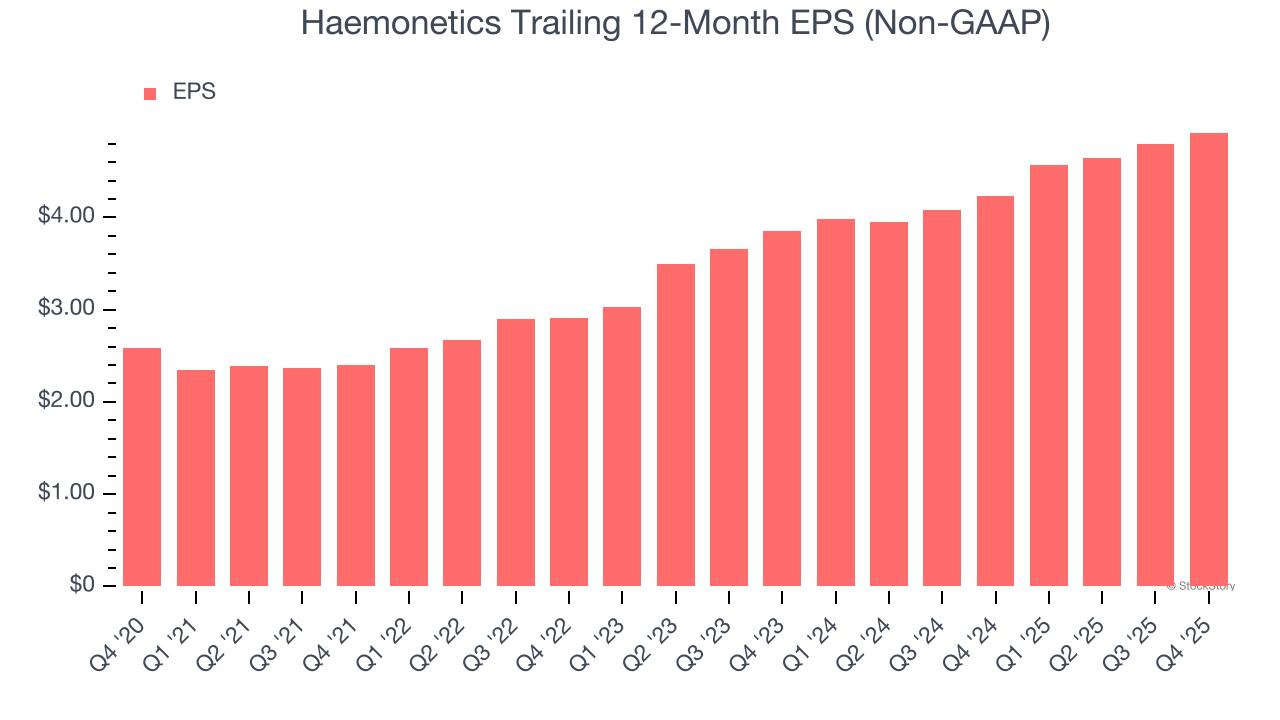

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Haemonetics’s EPS grew at a spectacular 13.8% compounded annual growth rate over the last five years, higher than its 8.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

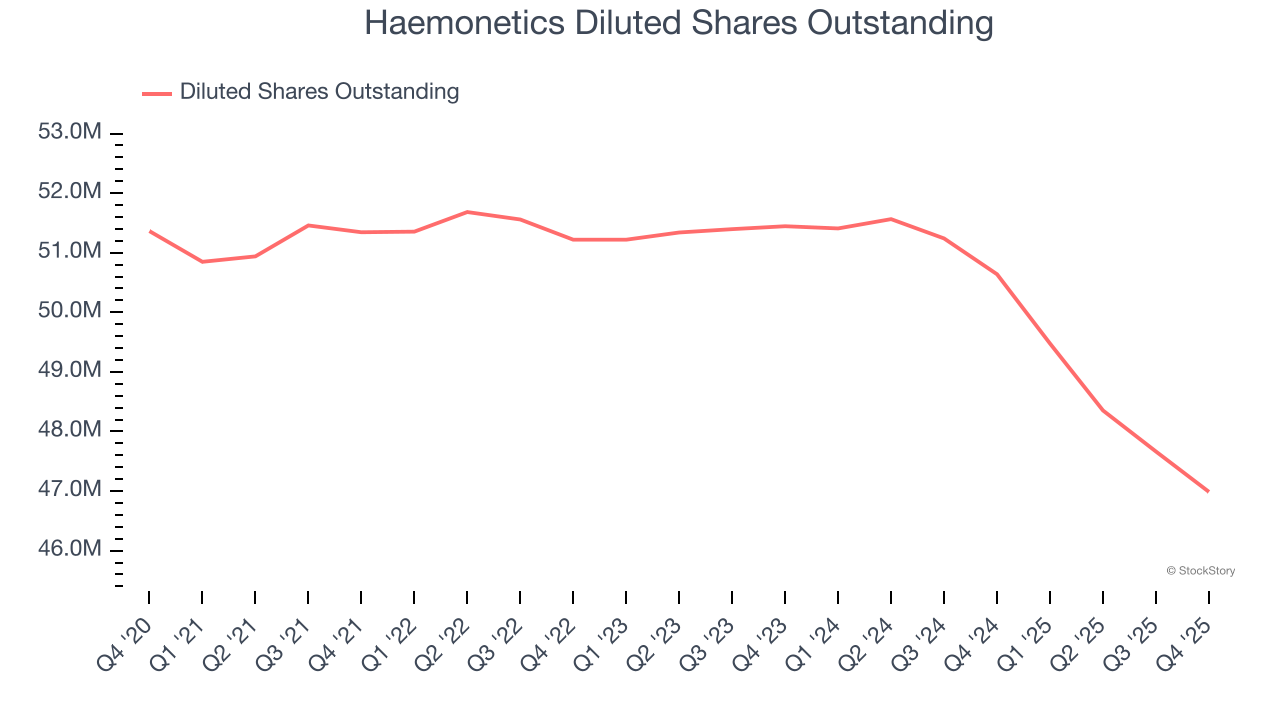

Diving into Haemonetics’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Haemonetics’s operating margin expanded by 14.8 percentage points over the last five years. On top of that, its share count shrank by 8.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Haemonetics reported adjusted EPS of $1.31, up from $1.19 in the same quarter last year. This print beat analysts’ estimates by 4.8%. Over the next 12 months, Wall Street expects Haemonetics’s full-year EPS of $4.92 to grow 6.9%.

We enjoyed seeing Haemonetics beat analysts’ organic revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Additionally, EPS beat, and the company raised its full-year EPS guidance. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 8.7% to $71.66 immediately following the results.

Haemonetics had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-28 | |

| Jul-08 | |

| Jun-05 | |

| Jun-02 | |

| May-08 | |

| May-07 | |

| May-07 | |

| May-05 | |

| Apr-24 | |

| Apr-01 | |

| Mar-30 | |

| Mar-30 | |

| Mar-11 | |

| Mar-05 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite