|

|

|

|

|||||

|

|

|

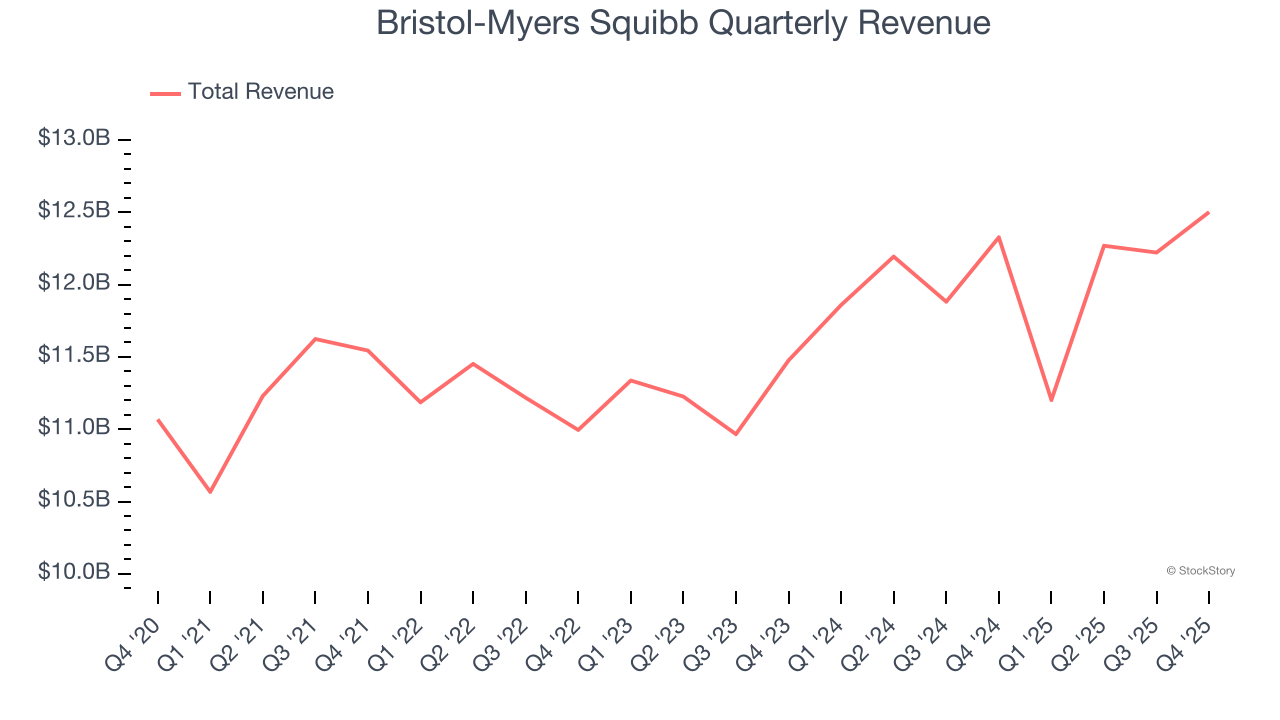

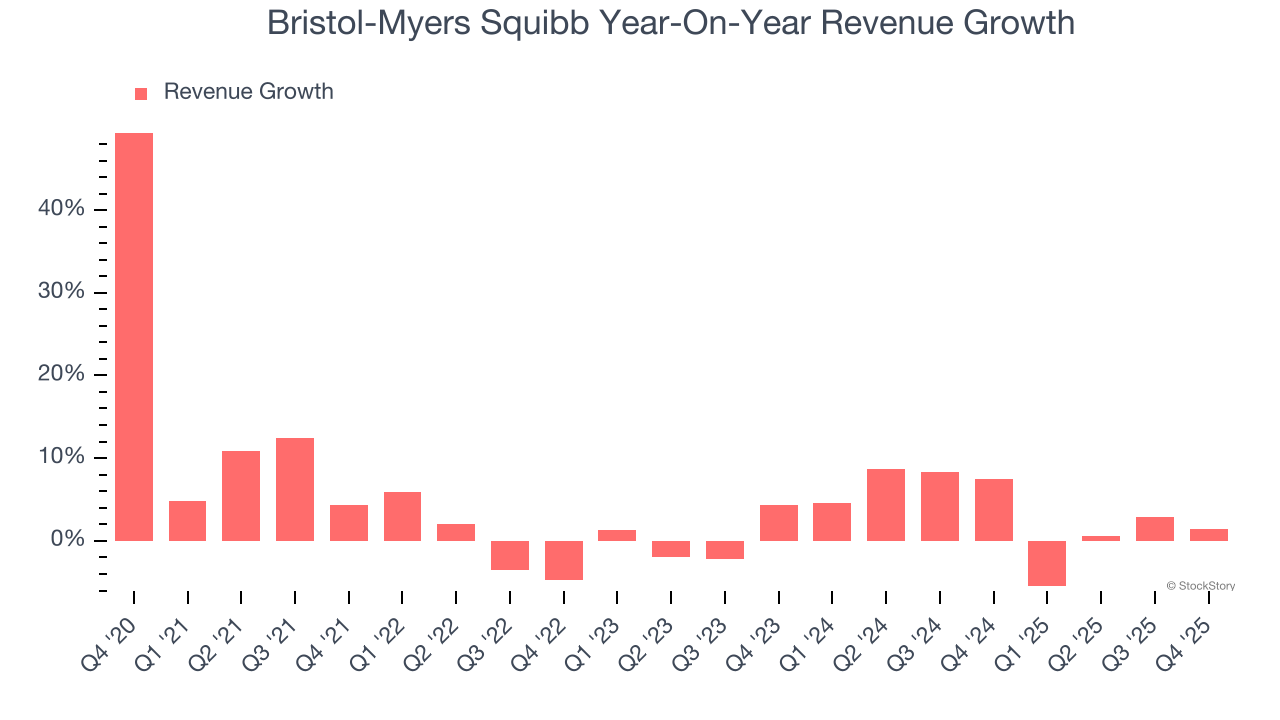

Biopharmaceutical company Bristol Myers Squibb (NYSE:BMY) announced better-than-expected revenue in Q4 CY2025, with sales up 1.4% year on year to $12.5 billion. The company’s full-year revenue guidance of $46.75 billion at the midpoint came in 5.7% above analysts’ estimates. Its non-GAAP profit of $1.26 per share was 4.6% above analysts’ consensus estimates.

Is now the time to buy Bristol-Myers Squibb? Find out by accessing our full research report, it’s free.

With roots dating back to 1887 and a transformative merger in 1989 that gave the company its current name, Bristol-Myers Squibb (NYSE:BMY) discovers, develops, and markets prescription medications for serious diseases including cancer, blood disorders, immunological conditions, and cardiovascular diseases.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Bristol-Myers Squibb’s sales grew at a tepid 3% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Bristol-Myers Squibb’s annualized revenue growth of 3.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

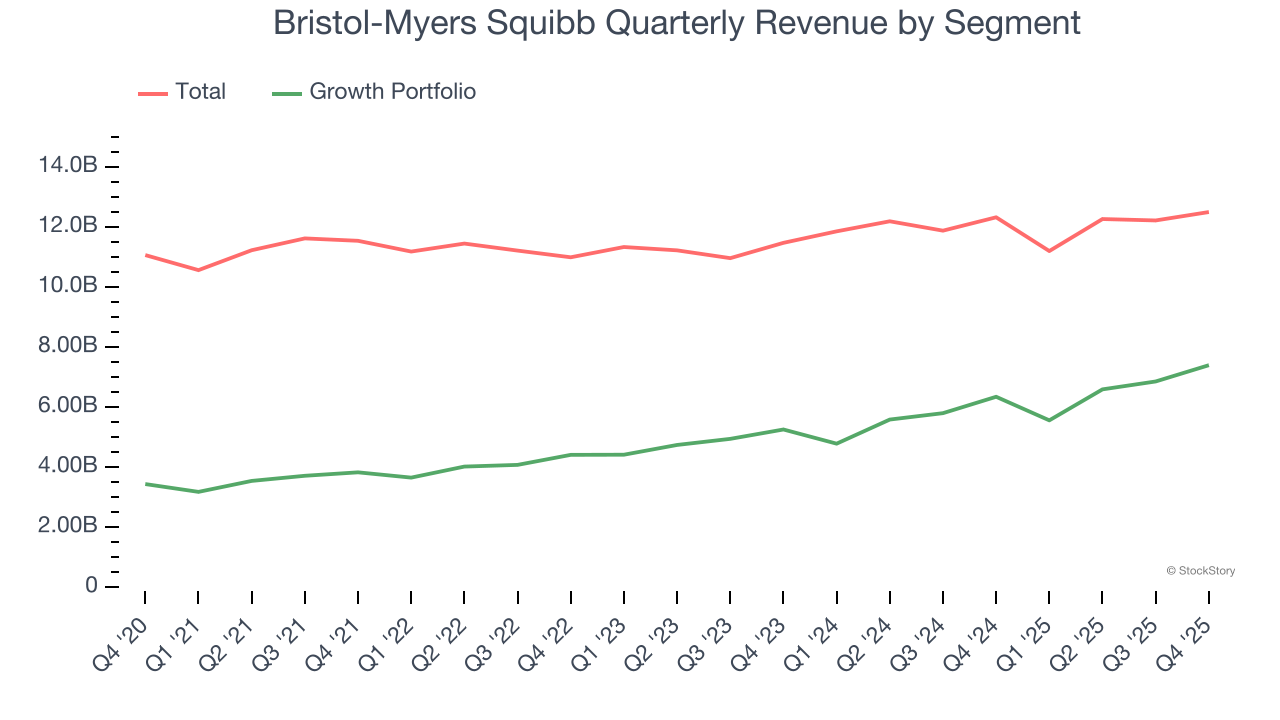

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Growth Portfolio. Over the last two years, Bristol-Myers Squibb’s Growth Portfolio revenue averaged 16.7% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Bristol-Myers Squibb reported modest year-on-year revenue growth of 1.4% but beat Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to decline by 7.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

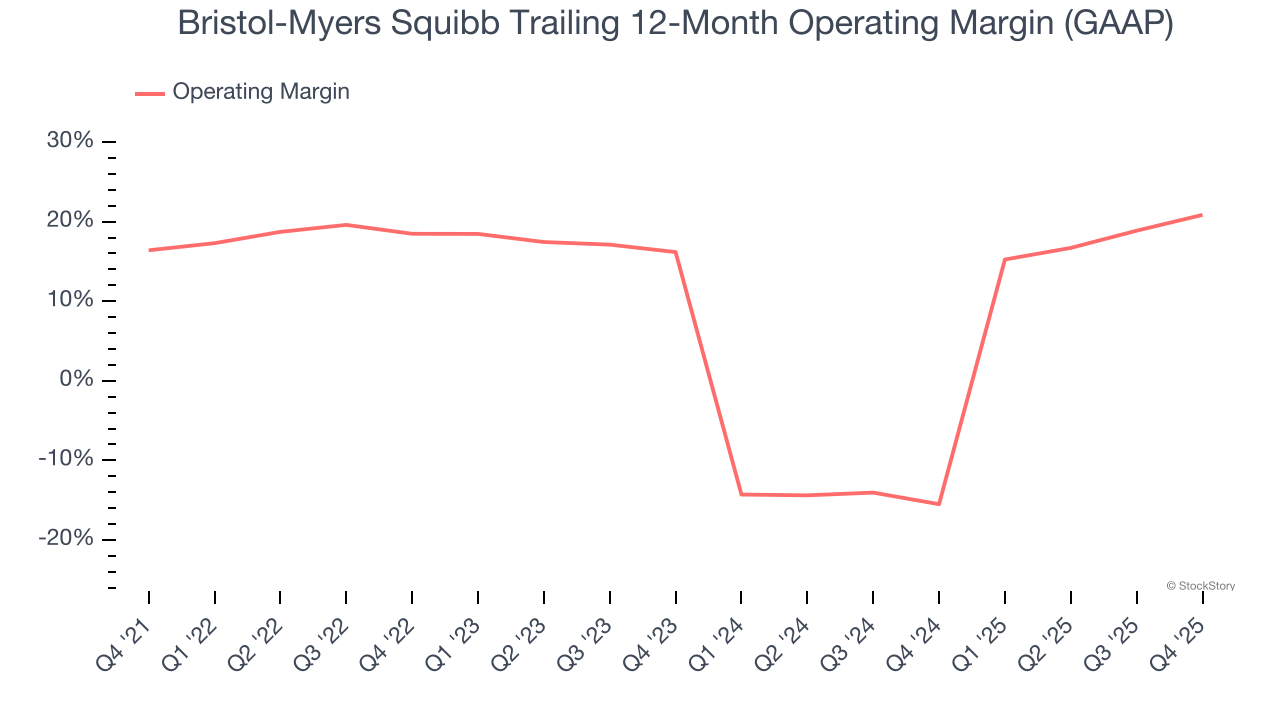

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Bristol-Myers Squibb has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 11%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Bristol-Myers Squibb’s operating margin rose by 4.4 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

This quarter, Bristol-Myers Squibb generated an operating margin profit margin of 11.8%, up 7.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

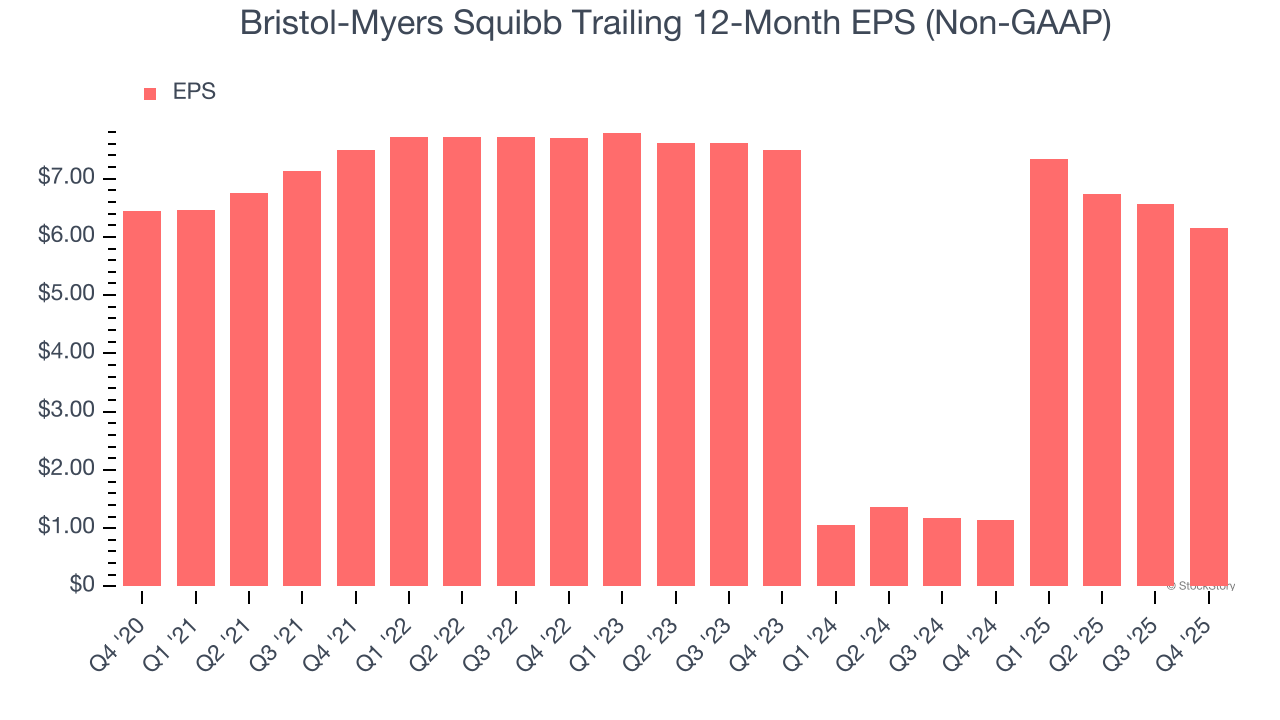

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Bristol-Myers Squibb’s flat EPS over the last five years was below its 3% annualized revenue growth. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q4, Bristol-Myers Squibb reported adjusted EPS of $1.26, down from $1.67 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.6%. Over the next 12 months, Wall Street expects Bristol-Myers Squibb’s full-year EPS of $6.15 to shrink by 3%.

We were impressed by Bristol-Myers Squibb’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.3% to $58.35 immediately following the results.

Indeed, Bristol-Myers Squibb had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| 14 hours | |

| 15 hours | |

| Apr-13 | |

| Apr-13 | |

| Apr-10 | |

| Apr-10 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Mar-30 | |

| Mar-30 | |

| Mar-29 | |

| Mar-28 | |

| Mar-27 |

Consecutive approvals of Opdivo for Hodgkins lymphoma to boost sales growth

BMY

Clinical Trials Arena

|

| Mar-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite