|

|

|

|

|||||

|

|

|

Deckers has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 5.5% to $111.69 per share while the index has gained 9.8%.

Is there a buying opportunity in Deckers, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We're sitting this one out for now. Here are three reasons there are better opportunities than DECK and a stock we'd rather own.

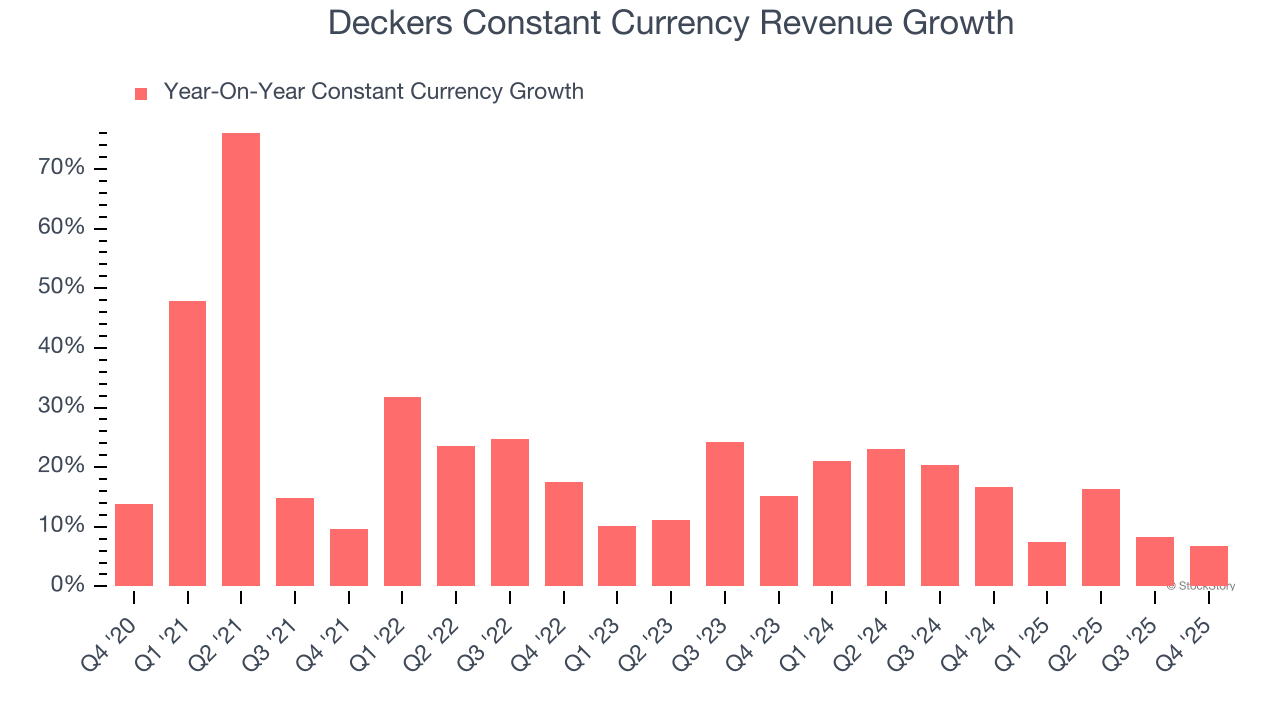

Investors interested in Footwear companies should track constant currency revenue in addition to reported revenue. This metric excludes currency movements, which are outside of Deckers’s control and are not indicative of underlying demand.

Over the last two years, Deckers’s constant currency revenue averaged 15% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

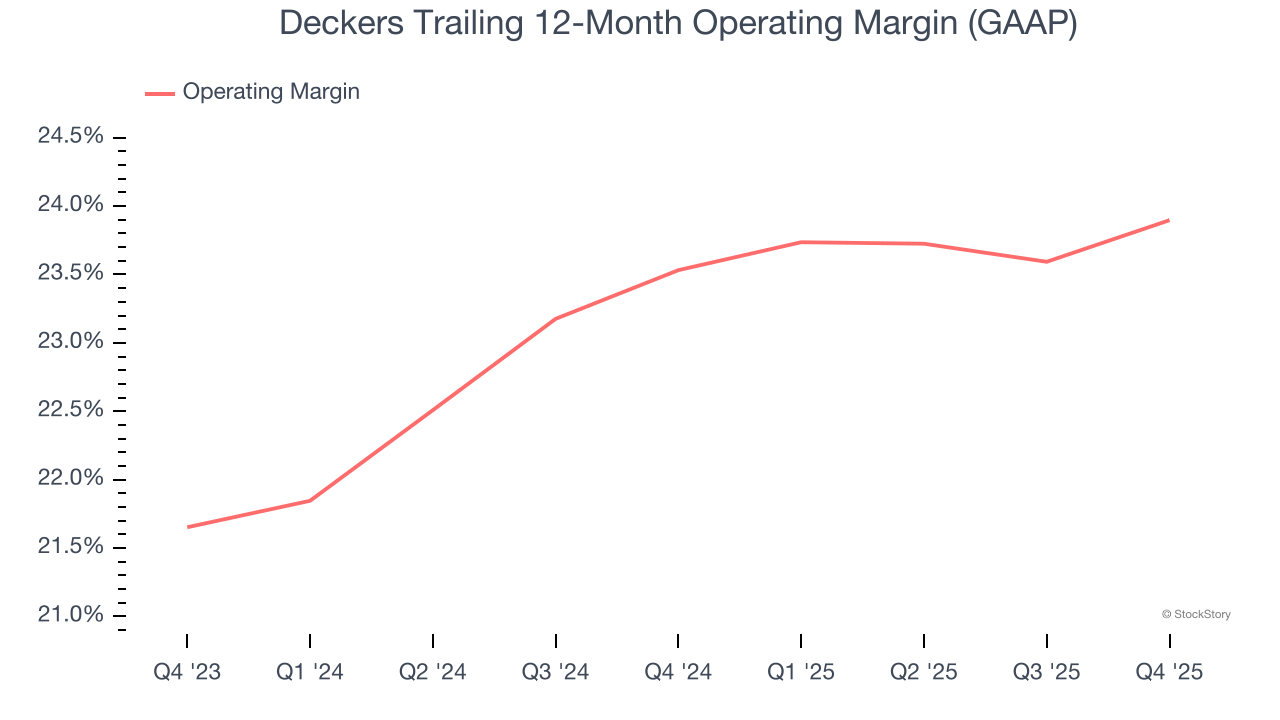

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Deckers’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 23.7% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

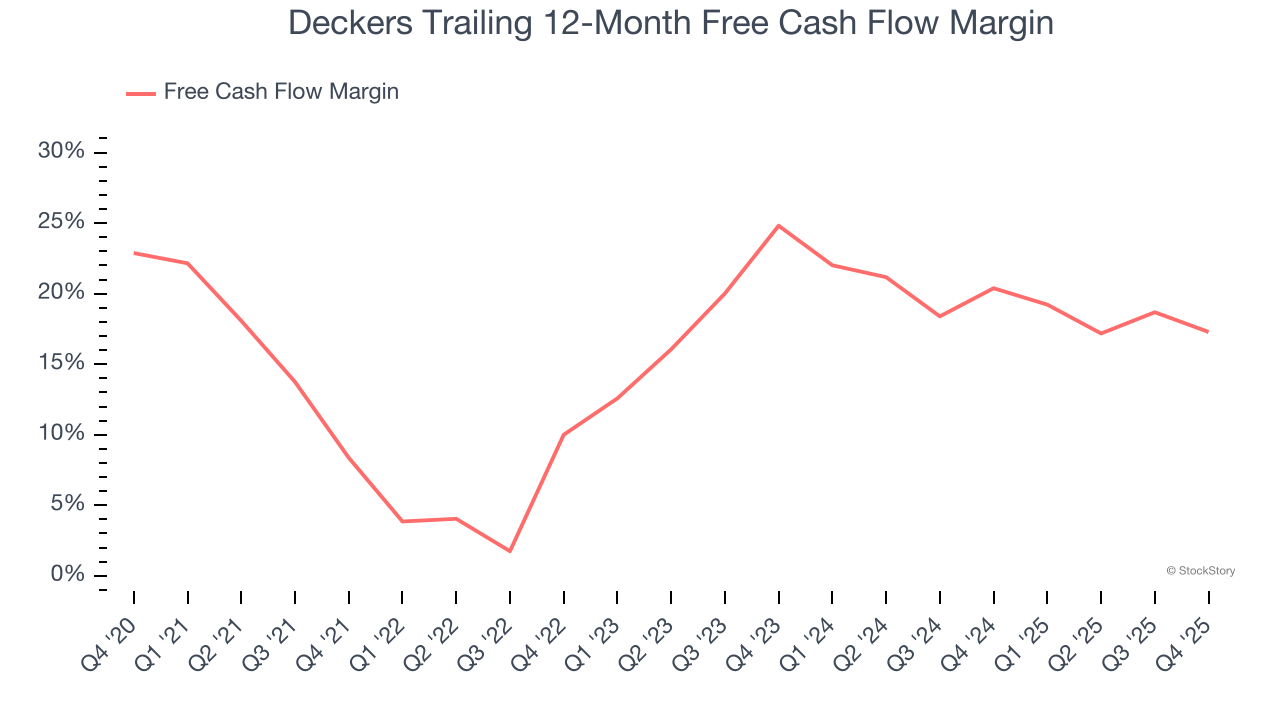

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Deckers has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 18.8%, lousy for a consumer discretionary business.

We see the value of companies helping consumers, but in the case of Deckers, we’re out. That said, the stock currently trades at 15.7× forward P/E (or $111.69 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jun-09 | |

| Jun-02 | |

| Jun-02 | |

| May-28 | |

| May-28 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-21 | |

| May-21 | |

| May-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite