|

|

|

|

|||||

|

|

|

Becton Dickinson and Company BDX, popularly known as BD, is scheduled to report first-quarter fiscal 2026 results on Feb. 9, before market open.

In the last reported quarter, the company’s adjusted earnings per share (EPS) of $3.96 surpassed the Zacks Consensus Estimate by 1%. Over the trailing four quarters, its earnings outperformed the Zacks Consensus Estimate on all occasions, delivering an earnings surprise of 6.5%, on average.

Let’s check out the factors that have shaped BDX’s performance prior to this announcement.

BD Medical’s strong fourth-quarter fiscal 2025 performance is expected to carry into the first quarter of fiscal 2026 as key growth drivers remain intact. In the fiscal fourth quarter, strength in Vascular Access Management and Infusion Systems in Medication Delivery Solutions and Medication Management Solutions business units, respectively, strong biologics demand in Pharmaceutical Systems (PS) unit and robust momentum in the Advanced Patient Monitoring unit, fueled by the HemoSphere Alta Monitor and Smart Recovery, all contributed to segment strength. This is likely to have continued in the to-be-reported quarter, supported by sustained demand for biologics and GLP-1 therapies. The segment is also likely to have benefited from the continued adoption of products, like Acumen IQ sensors.

During the quarter, the company launched BD Incada Connected Care Platform, a new scalable, AI-enabled, cloud-based platform that unifies BD device data into one intelligent ecosystem. It is now available with the next-generation BD Pyxis Pro Automated Medication Dispensing Solution, creating enterprise-wide visibility and connectivity that transforms data into actionable insight. This is likely to have witnessed strong customer adoption, thereby driving up the segmental revenues.

The Zacks Consensus Estimate for the first quarter of fiscal 2026 BD Medical segment’s revenues is currently pegged at $2.59 billion.

In December 2025, BD announced the expansion of its respiratory and sexually transmitted infection diagnostics offerings in Europe following In Vitro Diagnostic Medical Device Regulation certification of two VIASURE assays developed by Certest Biotec for use on the BD MAX System. The addition of these new assays to the BD MAX System portfolio is expected to enable clinical laboratories to detect a broad range of pathogens quickly and accurately using a fully automated molecular platform.

The same month, BD announced the global commercial release of new configurations of cell analyzers featuring breakthrough spectral and real-time cell imaging technologies. The three- and four-laser BD FACSDiscover A8 Cell Analyzers will likely expand accessibility of spectral, real-time imaging cell analysis.

In October, the segment’s Diagnostic Solutions (DS) business unit announced a new self-collection solution for HPV (human papillomavirus) testing in markets outside the United States, broadening access to cervical cancer screening. These are likely to have witnessed encouraging product adoption during the to-be-reported quarter, thereby driving the segmental revenues.

In November, BD announced that the Conformité Européenne (CE) Marked BD Onclarity HPV Assay for the BD COR System and the BD Viper LT System have been accepted for the World Health Organization list of prequalified in vitro diagnostic products. This is expected to expand access to high-quality cervical cancer screening tools in low- and middle-income countries. The same month, BD received the FDA’s 510(k) clearance and CE marking in the European Union for its Enteric Bacterial Panel (EBP) and Enteric Bacterial Panel plus (EBP plus) for the BD COR System. These also look promising for the stock.

However, BD continued to face market dynamics in China, which impacted its Specimen Management business unit’s performance in fourth-quarter fiscal 2025. The company’s research funding was also impacted by continued market dynamics during the fiscal fourth quarter. These raise our apprehension about the company’s performance in the to-be-reported quarter.

The Zacks Consensus Estimate for first-quarter fiscal 2026 BD Life Sciences revenues is currently pegged at $1.32 billion, suggesting an uptick of 1.9% from the year-ago quarter’s reported figure.

In November, the company launched the BD Surgiphor Surgical Wound Irrigation System in Europe, which is the first of its kind to receive CE approval. It is now available in select European countries. The same month, BD introduced the PureWick Portable Collection System, a discreet, battery-powered personal urine management device designed for wheelchair users to help improve mobility around and outside the home. These products are expected to have witnessed robust customer adoption during the fiscal first quarter, thereby driving up the segmental revenues.

On fourth-quarter fiscal 2025 earnings call in November, management stated that the company’s organic growth was led by robust growth in BD Interventional with strong performance across its growth platforms. This includes strong sales in the Urology & Critical Care business unit, driven by PureWick and in Surgery business unit, led by the Advanced Tissue Regeneration platform, including continued strong adoption of Phasix resorbable mesh. Growth in the Peripheral Intervention business unit reflected strength across the oncology portfolio and Rotarex. We expect this momentum to have continued in the first quarter of fiscal 2026.

The Zacks Consensus Estimate for first-quarter fiscal 2026 BD Interventional revenues is currently pegged at $1.30 billion, suggesting an uptick of 3.6% from the year-ago quarter’s reported figure.

For first-quarter fiscal 2026, the Zacks Consensus Estimate for revenues is pegged at $5.15 billion, implying a decline of 0.4% from the prior-year quarter’s reported figure.

The consensus estimate for EPS is pegged at $2.82, indicating a decrease of 17.8% from the prior-year period’s reported number.

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold), along with a positive Earnings ESP, has higher chances of beating estimates. This is not the case here, as you can see below.

Earnings ESP: BD has an Earnings ESP of -0.56%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank stocks here.

Becton, Dickinson and Company price-eps-surprise | Becton, Dickinson and Company Quote

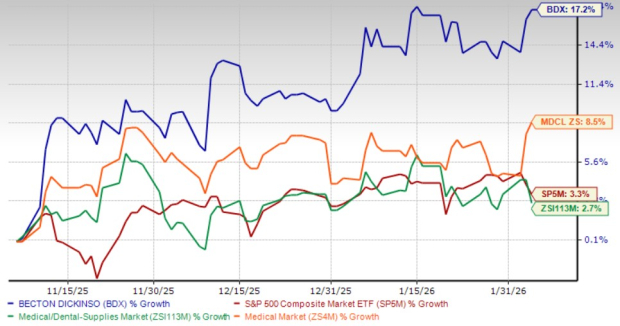

Over the past three months, BD’s shares have gained 17.2%, outperforming the Medical - Dental Supplies’ 2.7% gain. BDX’s shares also outperformed the Zacks Medical sector’s increase of 8.5% and the S&P 500’s growth of 3.3%.

BD’s peer, Globus Medical, Inc. GMED, has outperformed the company, while other peers like Masimo Corporation MASI and Merit Medical Systems, Inc. MMSI have underperformed. GMED, MASI and MMSI’s shares are up 41.1%, down 5% and down 8.3%, respectively, in the same time frame.

From a valuation standpoint, BDX’s forward 12-month price-to-earnings (P/E) is 13.7X, a discount to the industry's average of 17.5X and its five-year median of 18.5X.

The company is trading at a discount to its peers, Globus Medical, Masimo and Merit Medical. Globus Medical, Masimo and Merit Medical’s P/E currently stand at 21.9X, 23.5X and 19.5X, respectively.

This suggests that investors may be paying a lower price relative to the company's expected sales growth.

Last month, BD and Envetec Sustainable Technologies announced the successful completion of a joint feasibility study to test the ability to recycle polystyrene Petri dishes into new, high-quality manufacturing feedstock. The results of the pilot study suggest that similar high-quality polymers, including polystyrene, polyester, polypropylene and polyethylene, could be reused in the manufacturing supply chain after being safely disinfected and processed. These polymers find extensive use in medical devices, such as those made by BD.

The same month, BD announced that the company's board of directors had set the close of business on Feb. 5, 2026, as the record date for the previously announced spin-off of BD's Biosciences (BDB) & DS business units. Immediately following the spin-off, the spun-off entity will be combined with Waters Corporation. BD had announced the definitive agreement to combine its BDB & DS business with Waters in July 2025. Per BD’s management, the agreement will likely bring together complementary portfolios and channels that create an industry-leading life science and diagnostics company. This looks promising for BD as it is expected to enhance its strategic focus as a medical technology company.

Also, in January, BD and Ypsomed announced that they are strengthening their collaboration with the development of a 5.5 mL version of the BD Neopak XtraFlow Glass Prefillable Syringe. The same month, BD announced an $110 million investment to expand its production of prefillable syringes, helping accelerate biologic and GLP-1 drug delivery and supporting pharmaceutical reshoring in the United States. This investment will bring BD Neopak Glass Prefillable Syringe production to Columbus, NE, thus reinforcing its supply resilience within its PS portfolio.

In January, BD announced that the FDA granted 510(k) clearance for the EnCor EnCompass Breast Biopsy and Tissue Removal System, a multi-modality breast biopsy system designed to provide clinicians with flexibility across breast imaging modalities in the diagnosis of breast disease. This looks promising for the company.

In December, BD announced a strategic collaboration with the Institute for Immunology and Immune Health at the University of Pennsylvania to advance research in deep human immune profiling and support the development of immune-mediated therapies. The same month, BDX announced a strategic collaboration with ChemoGLO to advance hazardous drug contamination testing in health care settings to improve the safety of health care workers. These partnerships raise our optimism about the stock’s performance in the long term.

However, BD’s strong performance in the fiscal fourth quarter was partially offset by continued market dynamics in China, which is likely to have continued in the to-be-reported quarter. The current unstable macroeconomic business environment is also likely to have weighed on the company’s fiscal first-quarter revenues, raising our apprehension.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 10 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite