|

|

|

|

|||||

|

|

|

SoFi Technologies, Inc.’s SOFI fourth-quarter 2025 results were undeniably strong, yet the stock’s response told a more complicated story. Despite earnings and revenue beating expectations, shares have declined roughly 9% since the results were released on Jan. 30.

That divergence between fundamentals and price action is precisely why this earnings review comes with a short pause. The market had time to digest the numbers, reset expectations and reassess valuation, making it clearer whether this was a one-day headline beat or something more structurally meaningful.

SoFi closed the quarter with adjusted earnings per share of 13 cents, which surpassed the Zacks Consensus Estimate by 8.3% and marked a massive improvement of 160% from the prior year. This was the fourth consecutive quarter in which SoFi exceeded consensus earnings estimates, signaling growing reliability in execution.

Quarterly revenues crossed a milestone, exceeding $1 billion for the first time. Revenues also beat the Zacks Consensus Estimate by 3.2%. On a year-over-year basis, adjusted net revenues expanded at a high double-digit rate, reflecting sustained demand across lending, financial services and platform operations. Growth was broad-based rather than concentrated, helping reduce reliance on any single business line and supporting a more balanced earnings profile.

Operating performance was one of the most notable takeaways from the quarter. Adjusted EBITDA of $317.6 million grew meaningfully faster than revenues, pushing margins above 30% and reinforcing that SoFi’s cost structure is beginning to scale efficiently.

Adjusted net income of $173.5 million rose 184% from the prior year, supported by improving margins and disciplined expense growth. GAAP profitability was maintained as well, extending the company’s streak of profitable quarters. This consistency matters, especially given SoFi’s earlier perception as a growth-first fintech. The earnings profile now reflects a company transitioning toward sustainable profitability rather than one reliant on favorable macro conditions.

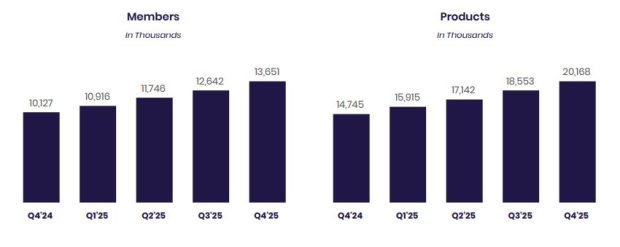

Member growth remained a key driver of SoFi’s momentum. Total members increased 35% to 13.7 million. Product growth of 37% to 20.2 million outpaced member additions, highlighting rising engagement across the platform.

A significant portion of new products was adopted by existing members, reinforcing the effectiveness of SoFi’s cross-selling strategy. This dynamic supports higher lifetime value per customer and improves monetization without requiring proportional increases in acquisition spending. Brand investment and product innovation continue to feed into this cycle, strengthening the company’s ecosystem over time.

One of the most constructive elements of the quarter was the acceleration in fee-based revenues. Growth of 53% in this segment outpaced overall revenue expansion, helping diversify income streams and reduce dependence on net interest income alone.

The Loan Platform Business played a meaningful role here, growing 15% year over year and contributing high-margin revenues while also supporting capital-light growth. At the same time, interchange, brokerage, and referral-related revenues showed healthy momentum, reinforcing the value of SoFi’s expanding product suite.

Lending continued to scale, with total originations reaching a record level of $10.5 billion during the quarter. Personal loans remained the primary contributor, supported by continued growth in student and home lending products.

Credit performance stayed within management’s expectations, with personal-loan charge-offs down 57 basis points year over year. While some metrics reflected normal portfolio seasoning, overall charge-off trends improved on a year-over-year basis. Management reiterated confidence in long-term loss assumptions, supported by performance data from recent loan vintages. This balance between growth and credit discipline remains central to the investment thesis.

The Technology Platform segment delivered steady revenue growth of 19% year over year, even as total enabled accounts declined following the transition of a large client. While the headline account number drew attention, contribution margins improved, indicating a shift toward higher-quality, more profitable relationships.

This segment continues to play a strategic role, offering longer-term optionality while contributing positively to consolidated profitability.

Management’s guidance for 2026 points to continued growth across revenues, earnings and margins, with medium-term expectations reinforcing sustained expansion beyond the near term. The outlook aligns closely with recent execution trends rather than assuming a step-change in operating conditions.

Total members are expected to grow by at least 30% year over year, reinforcing confidence in sustained customer acquisition and engagement. Adjusted net revenues are projected to be approximately $4.66 billion, implying around 30% year-over-year growth, driven by continued momentum across lending, financial services, and the platform ecosystem.

Profitability is set to scale alongside growth. Adjusted EBITDA is expected to reach roughly $1.6 billion, translating to an EBITDA margin of about 34%. Adjusted net income is projected at approximately $825 million, implying a margin near 18%, while adjusted earnings per share are expected to come in around 60 cents, reflecting strong bottom-line expansion.

For the first quarter of 2026, management expects adjusted net revenues of approximately $1.04 billion, adjusted EBITDA of around $300 million, adjusted net income of roughly $160 million, and adjusted EPS of approximately 12 cents. This guidance suggests steady sequential performance following the strong finish to 2025.

SoFi’s latest quarter confirms that the business is executing well, with improving profitability, strong member engagement and diversified revenue streams. However, the post-earnings pullback suggests much of this progress was already expected. While the long-term story remains intact and operational momentum is encouraging, near-term stock performance may stay choppy as investors reassess valuation and growth sustainability. At this stage, SoFi appears best positioned as a hold—supported by solid fundamentals but lacking a clear catalyst for immediate upside. Patience may be rewarded, but selectivity remains key.

SOFI currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Trane Technologies TT reported impressive fourth-quarter 2025 results.TT’s quarterly earnings of $2.86 per share beat the Zacks Consensus Estimate by 1.4% and increased 9.6% from the year-ago quarter.

TT’s total revenues of $5.1 billion surpassed the consensus estimate by 1.3% and rallied 5.5% from the year-ago quarter.

Booz Allen Hamilton BAH registered mixed results for third-quarter fiscal 2026. BAH’s earnings per share of $1.77 beat the consensus mark by 40.5% and increased 14.2% from the year-ago quarter.

BAH’s revenues of $2.6 billion missed the Zacks Consensus Estimate by 3.9% and declined 10.2% from the year-ago quarter.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 min | |

| 54 min | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite