|

|

|

|

|||||

|

|

|

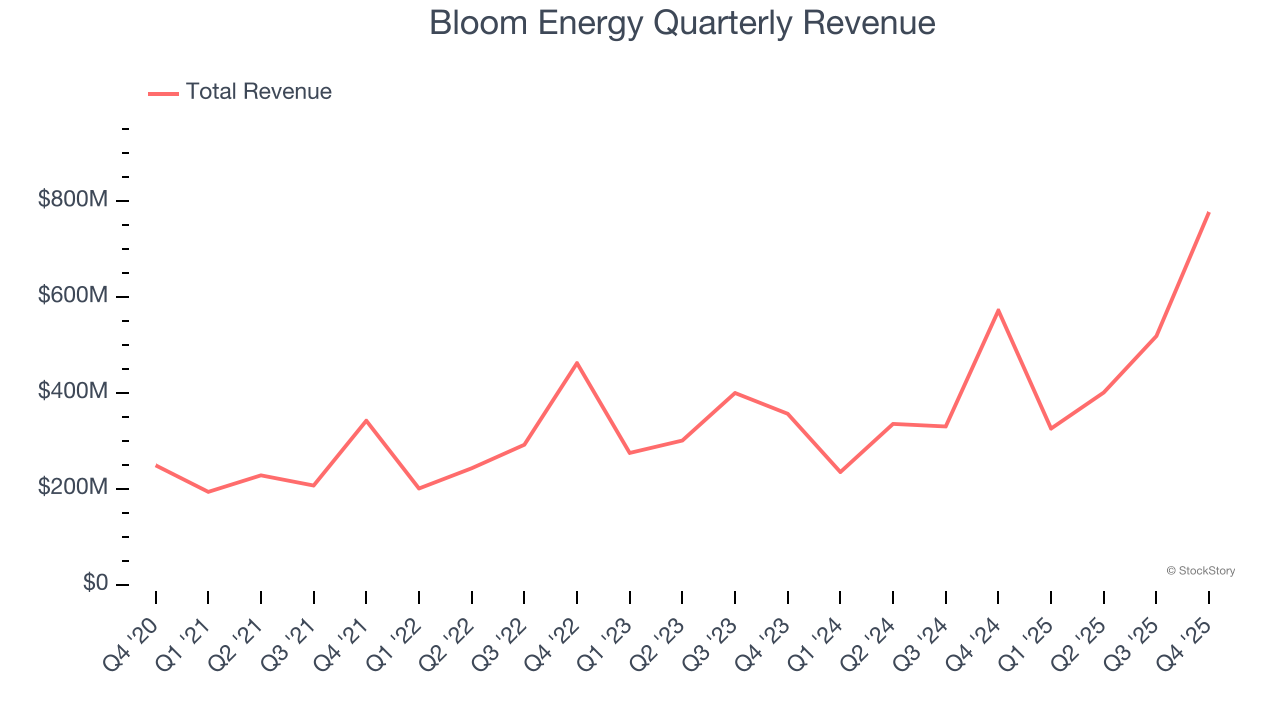

Electricity generation and hydrogen production company Bloom Energy (NYSE:BE) announced better-than-expected revenue in Q4 CY2025, with sales up 35.9% year on year to $777.7 million. The company’s full-year revenue guidance of $3.2 billion at the midpoint came in 24.2% above analysts’ estimates. Its non-GAAP profit of $0.45 per share was 50.4% above analysts’ consensus estimates.

Is now the time to buy Bloom Energy? Find out by accessing our full research report, it’s free.

KR Sridhar, Founder, Chairman, and CEO of Bloom Energy said, “Bring-your-own-power has shifted from a slogan to a business necessity for AI hyperscalers and manufacturing facilities. This shift is secular and growing. We have built a solid state digital power platform for the digital age that is superior to any legacy solution.”

Working in stealth mode for eight years, Bloom Energy (NYSE:BE) designs, manufactures, and markets solid oxide fuel cell systems for on-site power generation.

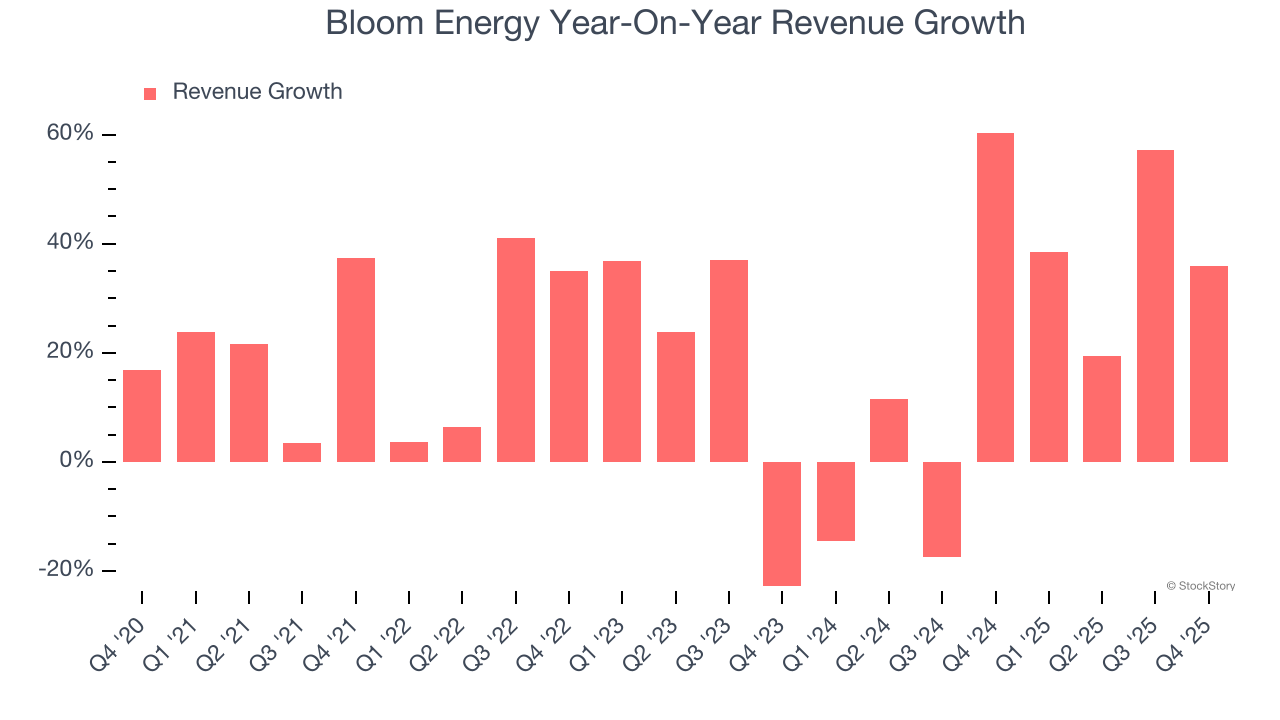

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Bloom Energy’s 20.6% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Bloom Energy’s annualized revenue growth of 23.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

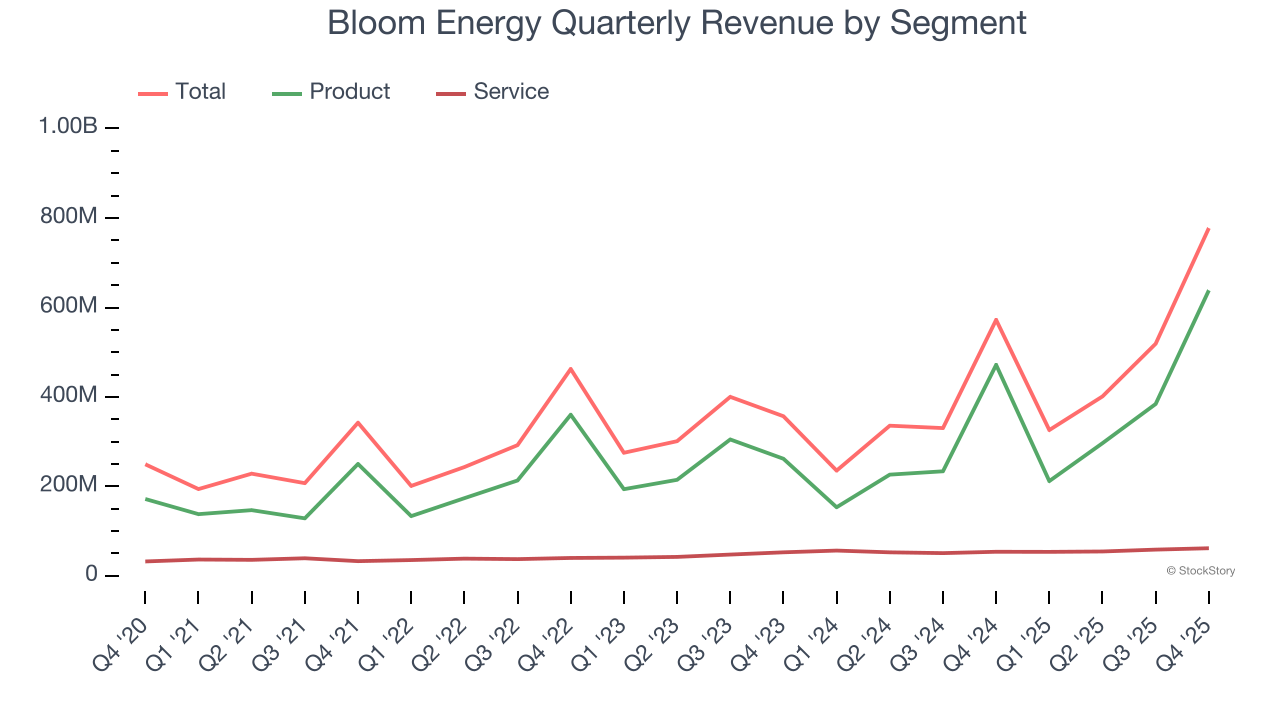

We can better understand the company’s revenue dynamics by analyzing its most important segments, Product and Service, which are 82.1% and 7.9% of revenue. Over the last two years, Bloom Energy’s Product revenue (energy servers and electrolyzers) averaged 26.3% year-on-year growth while its Service revenue (operations and maintenance agreements) averaged 12.6% growth.

This quarter, Bloom Energy reported wonderful year-on-year revenue growth of 35.9%, and its $777.7 million of revenue exceeded Wall Street’s estimates by 18.7%.

Looking ahead, sell-side analysts expect revenue to grow 23.7% over the next 12 months, similar to its two-year rate. This projection is eye-popping and indicates the market is baking in success for its products and services.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

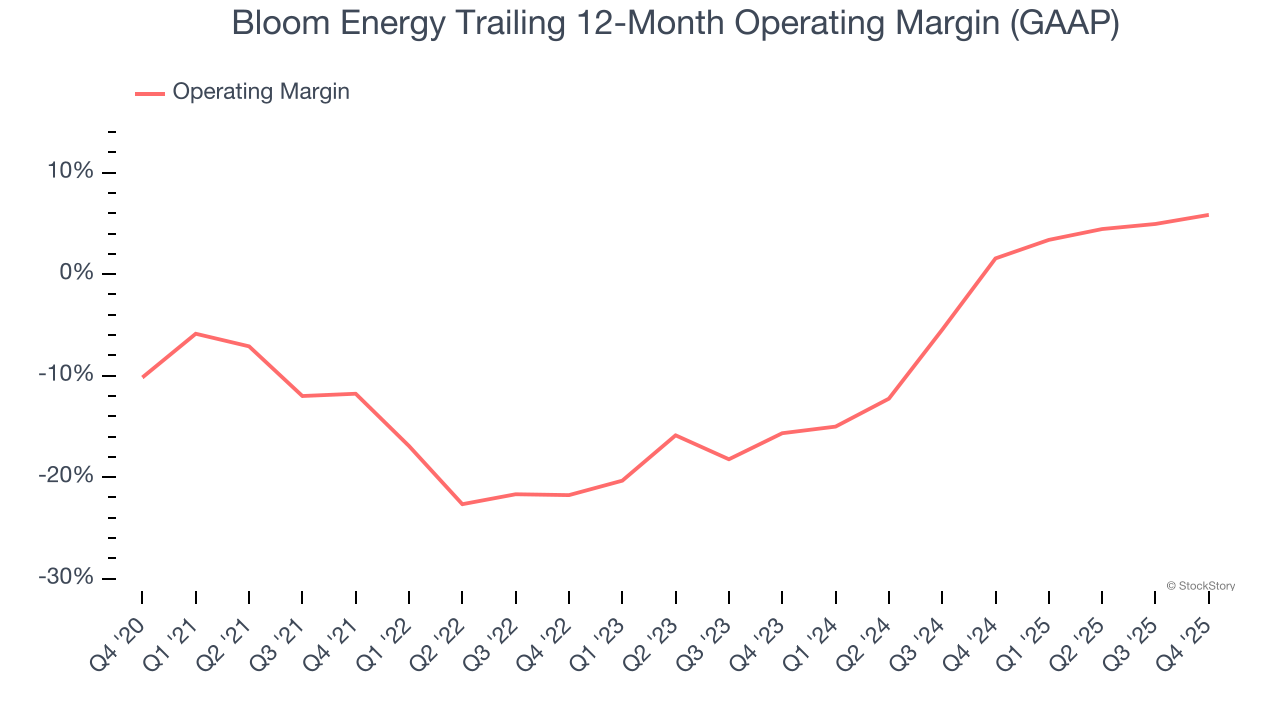

Although Bloom Energy was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6.3% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Bloom Energy’s operating margin rose by 17.6 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

In Q4, Bloom Energy generated an operating margin profit margin of 17.1%, down 1.2 percentage points year on year. Since Bloom Energy’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

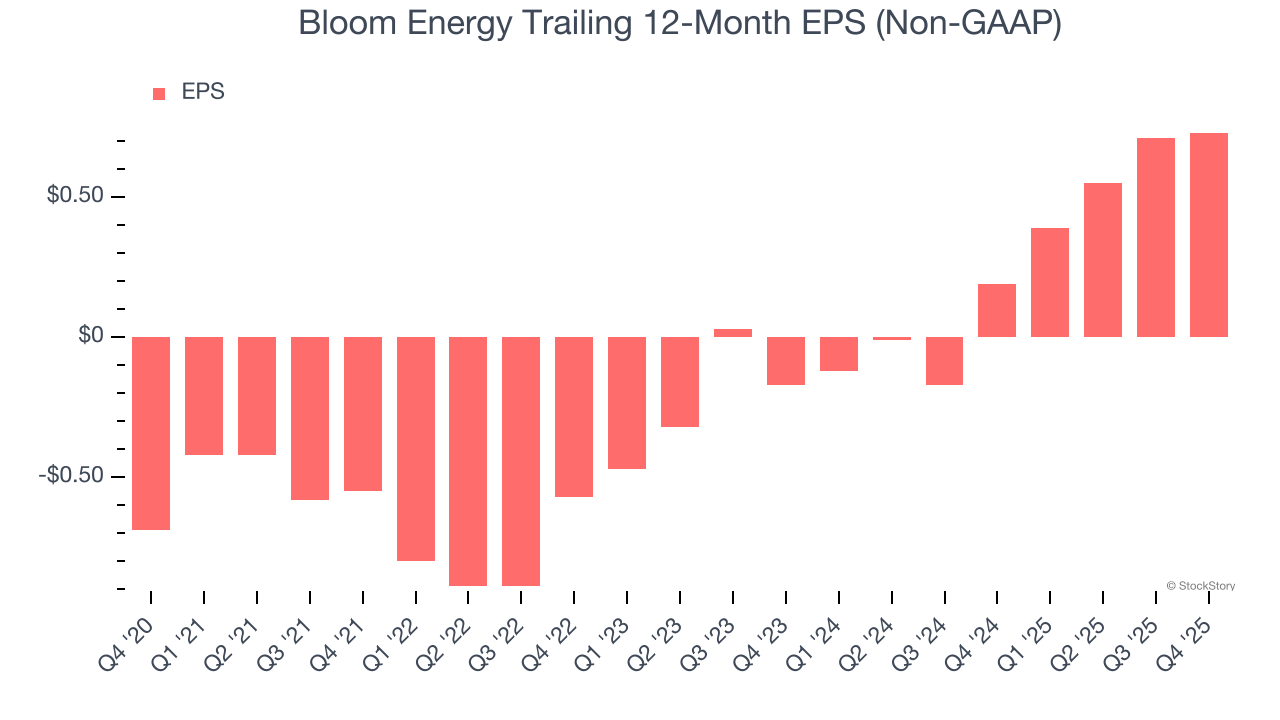

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Bloom Energy’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Bloom Energy, its two-year annual EPS growth of 151% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Bloom Energy reported adjusted EPS of $0.45, up from $0.43 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Bloom Energy’s full-year EPS of $0.73 to grow 47.1%.

It was good to see Bloom Energy beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its Service revenue missed. Zooming out, we think this quarter featured some important positives. The stock traded up 9.1% to $151 immediately following the results.

Indeed, Bloom Energy had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Apr-09 | |

| Apr-06 | |

| Mar-26 | |

| Mar-26 | |

| Mar-24 | |

| Mar-23 |

AI Enabler Blossoms, Wilts And Wavers In Thorny Market. What's An Investor To Do?

BE -5.86%

Investor's Business Daily

|

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite