|

|

|

|

|||||

|

|

|

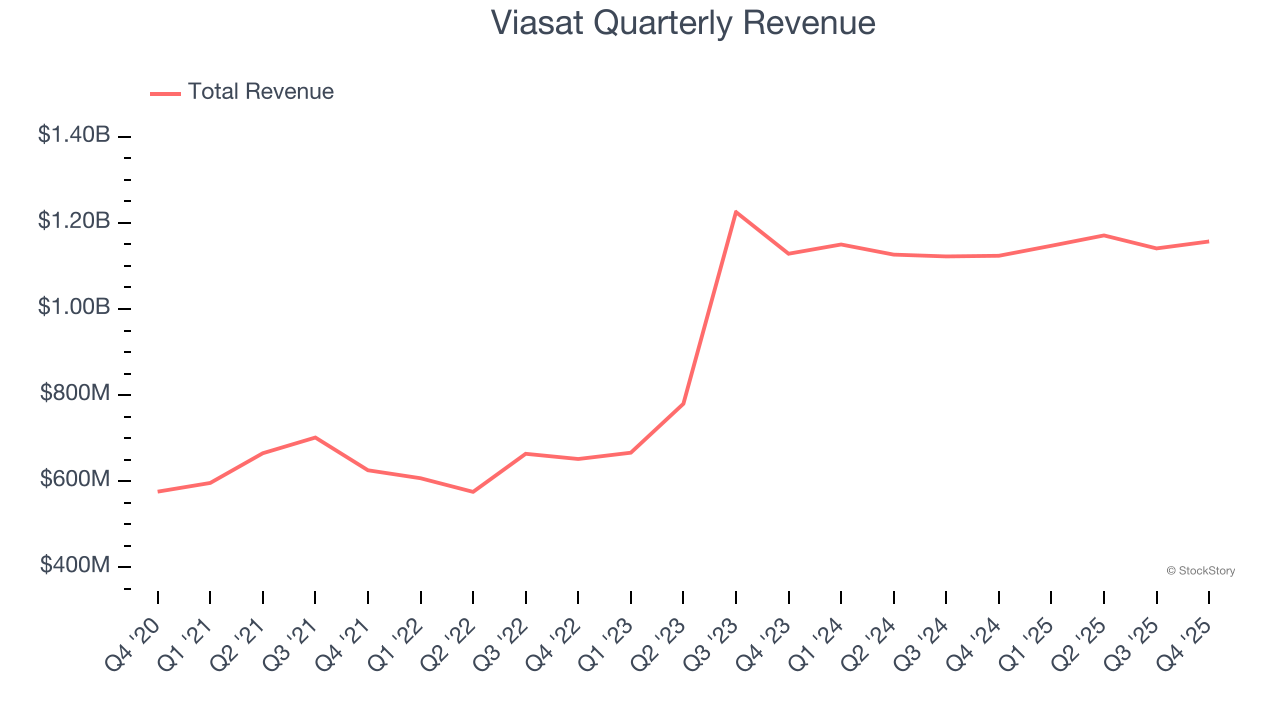

Global satellite communications provider Viasat (NASDAQ:VSAT) missed Wall Street’s revenue expectations in Q4 CY2025 as sales rose 3% year on year to $1.16 billion. Its non-GAAP profit of $0.79 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Viasat? Find out by accessing our full research report, it’s free.

Operating a fleet of 23 satellites that orbit the Earth and beam connectivity from space, Viasat (NASDAQ:VSAT) provides satellite-based communications networks and services for airlines, maritime vessels, governments, businesses, and residential customers worldwide.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.62 billion in revenue over the past 12 months, Viasat is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

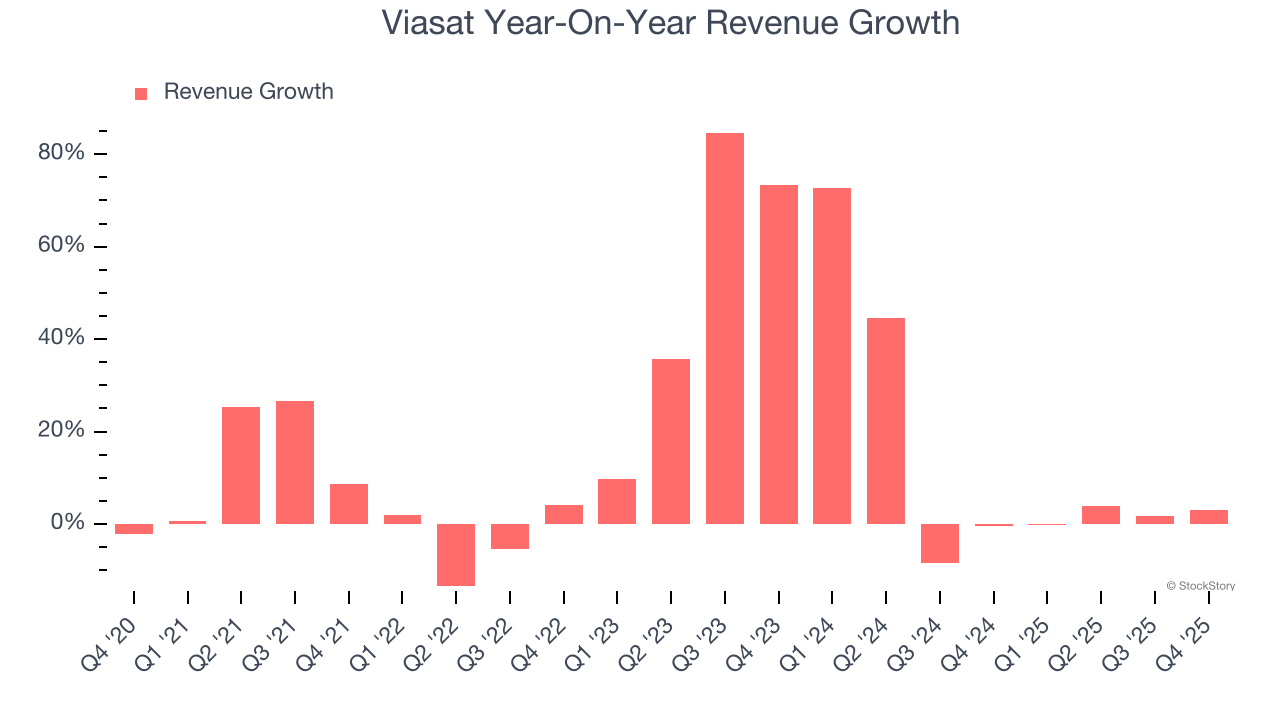

As you can see below, Viasat’s 15.4% annualized revenue growth over the last five years was incredible. This is an encouraging starting point for our analysis because it shows Viasat’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Viasat’s annualized revenue growth of 10.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Viasat’s revenue grew by 3% year on year to $1.16 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

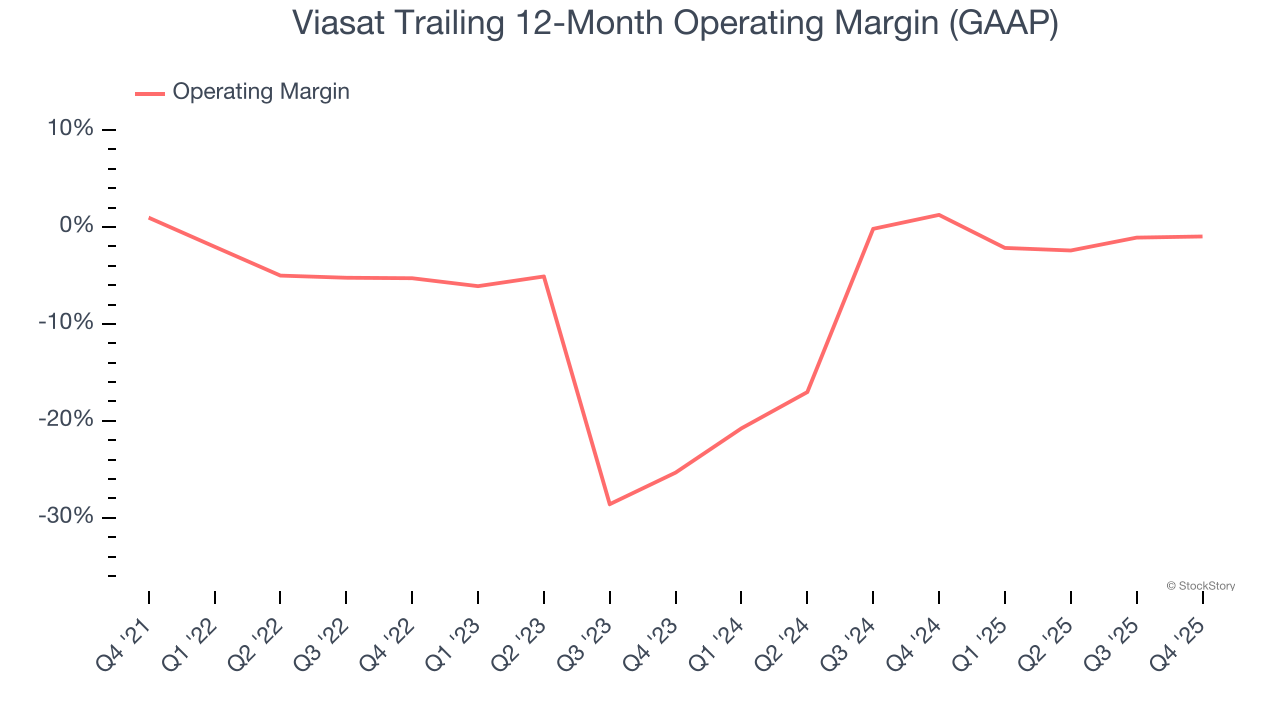

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Although Viasat was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 5.9% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

Analyzing the trend in its profitability, Viasat’s operating margin decreased by 1.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Viasat’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Viasat generated an operating margin profit margin of 2.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

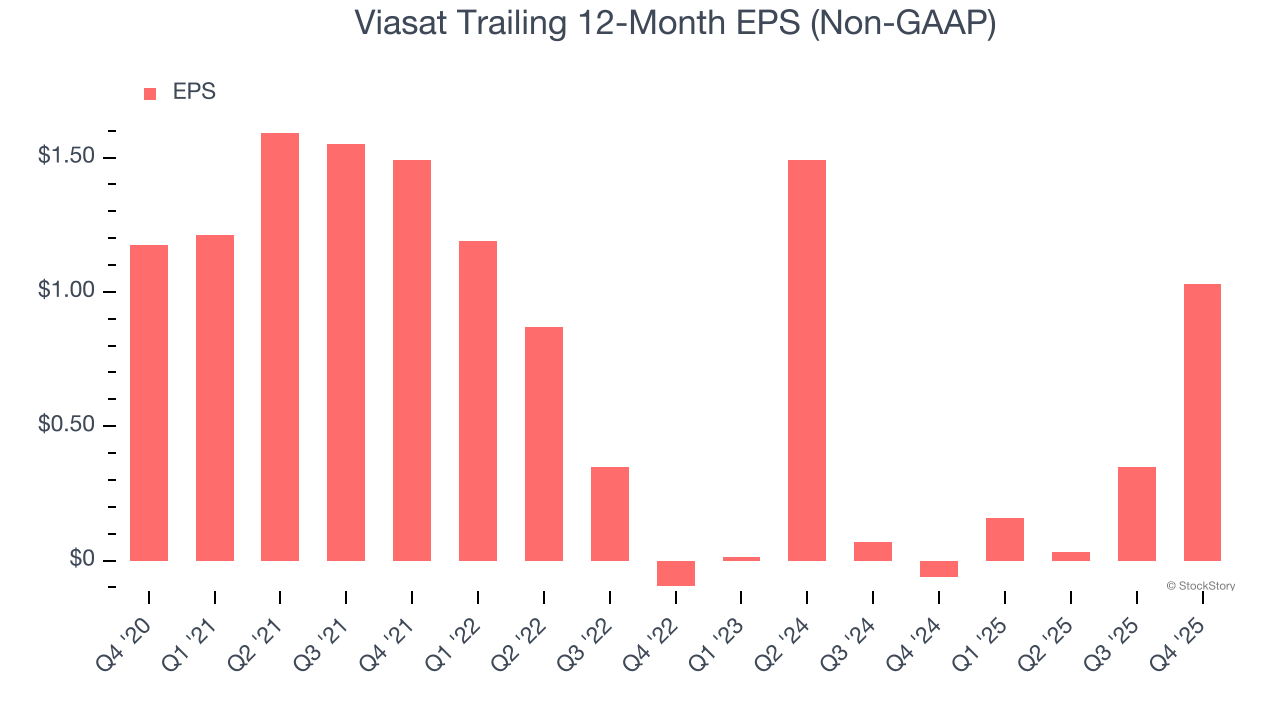

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Viasat, its EPS declined by 2.6% annually over the last five years while its revenue grew by 15.4%. This tells us the company became less profitable on a per-share basis as it expanded.

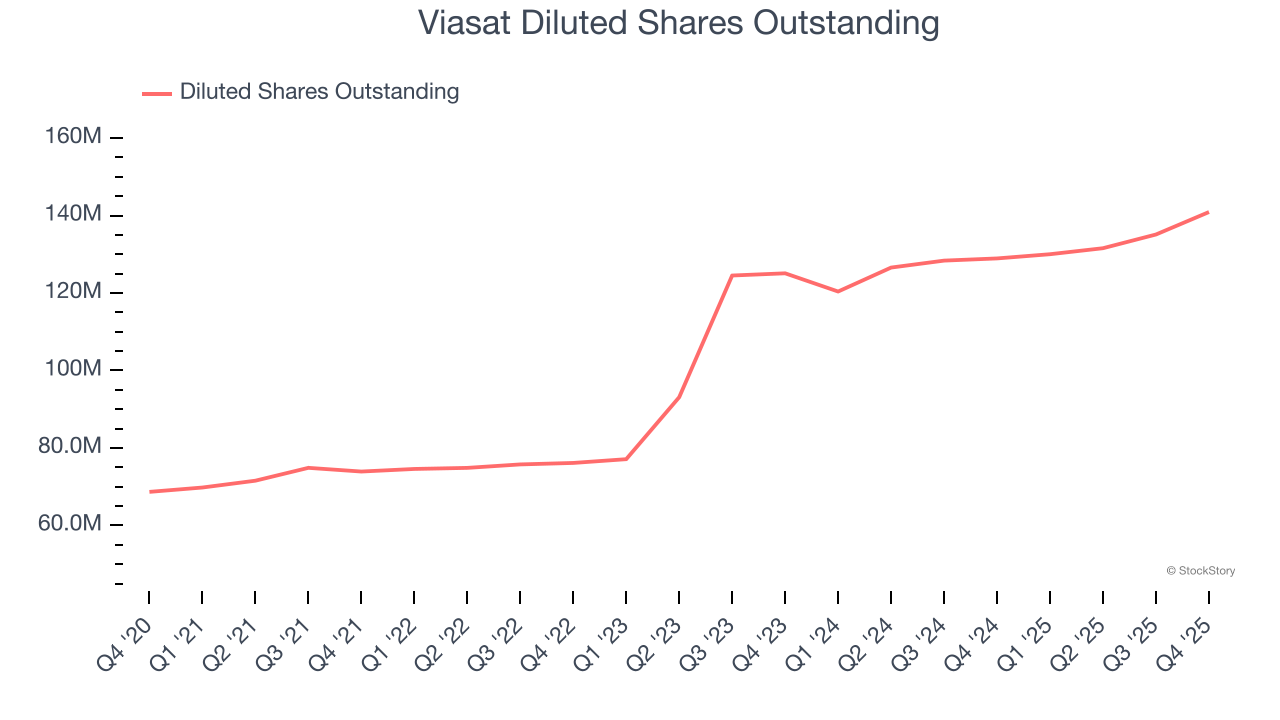

We can take a deeper look into Viasat’s earnings to better understand the drivers of its performance. As we mentioned earlier, Viasat’s operating margin was flat this quarter but declined by 1.9 percentage points over the last five years. Its share count also grew by 105%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Viasat, its two-year annual EPS declines of 26.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Viasat reported adjusted EPS of $0.79, up from $0.11 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Viasat’s full-year EPS of $1.03 to shrink by 27.5%.

It was good to see Viasat beat analysts’ EPS expectations this quarter. On the other hand, its revenue slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.5% to $36.91 immediately after reporting.

So do we think Viasat is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-22 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-10 | |

| Jul-06 |

?? Under the Radar: Investors Salivate Over Wireless Spectrum, Fueling Viasat Rally

VSAT

The Wall Street Journal

|

| Jul-06 | |

| Jul-02 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 | |

| Jun-29 | |

| Jun-27 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite