|

|

|

|

|||||

|

|

|

AbbVie ABBV is set to report first-quarter 2025 earnings on April 25, before the opening bell. The Zacks Consensus Estimate for the quarter’s sales and earnings is pegged at $12.91 billion and $2.40 per share, respectively. The company’s earnings estimates for 2025 have declined from $12.31 per share to $12.22 in the past 30 days. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar)

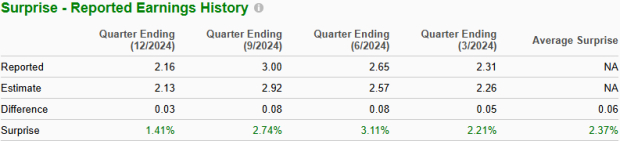

AbbVie’s performance has been pretty impressive, with its earnings exceeding expectations in each of the trailing four quarters. It delivered a trailing four-quarter average earnings surprise of 2.37%. In the last reported quarter, the pharma giant delivered an earnings surprise of 1.41%.

Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or3 (Hold) have a good chance of delivering an earnings beat. This is not the case here. You can uncover the best stocksto buy or sell before they’re reported with our Earnings ESP Filter.

AbbVie has an Earnings ESP of -0.92% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

For the first quarter of 2025, AbbVie expects adjusted earnings to be in the range of $2.34-$2.38 per share. The company expects net revenues of approximately $12.8 billion. Currency is expected to negatively impact revenues by around 1.6% on sales.

AbbVie’s top line in the quarter is likely to have been driven by sales of newer immunology drugs, Skyrizi and Rinvoq. Approvals in new indications must have been driving strong revenues for these drugs. The Zacks Consensus Estimate for Skyrizi sales is pegged at $3.19 billion, while the same for Rinvoq is pinned at $1.61 billion. Our model estimate for Skyrizi and Rinvoq sales is pegged at $3.19 billion and $1.62 billion, respectively.

ABBV lost patent protection for its blockbuster immunology drug Humira in the United States in January 2023 and has been facing sales erosion ever since. The drug lost exclusivity in ex-U.S. territories in 2018. The Zacks Consensus Estimate for Humira sales is pegged at $1.32 billion, while our estimate for the same is pinned at $1.31 billion.

The company has also provided its quarterly forecast for the immunology franchise. It expects to generate revenues worth $6.1 billion (from this franchise), including sales of $3.2 billion, $1.6 billion and $900 million from Skyrizi, Rinvoq and U.S. Humira, respectively.

AbbVie expects to record $1.5 billion from the sale of its oncology drugs. We expect J&J JNJ-partnered Imbruvica sales to have declined due to competition from novel oral therapies. The Zacks Consensus Estimate and our model estimate for the J&J-partnered drug’s sales are pegged at $676 million each.

Roche RHHBY-partnered Venclexta sales are likely to have risen as new patient starts might have improved, driven by strong demand for both CLL and AML indications. The Zacks Consensus Estimate and our model estimate for the Roche-partnered drug’s sales are pegged at $625 million and $630 million, respectively.

Sales of the neuroscience franchise have shown strong growth in recent quarters. Neuroscience sales are likely to have been driven by higher sales of Botox Therapeutic, depression drug Vraylar and new migraine drugs — Ubrelvy and Qulipta. In November, AbbVie gained approval for Vyalev, a transformative therapy for treating advanced Parkinson’s disease. Investors will watch the initial sales numbers for this new drug.

The Zacks Consensus Estimate and our model estimate for neuroscience product sales are pegged at $2.16 billion and $2.21 billion, respectively. ABBV forecasts revenues from its neuroscience segment to be $2.1 billion for the quarter.

In the aesthetics franchise, we expect overall sales to have been negatively impacted by the sluggish growth of Botox and Juvederm fillers in the United States and China. The Zacks Consensus Estimate and our model estimate for aesthetics product sales are pegged at $1.14 billion each. AbbVie expects to generate $1.1 billion from the sale of its aesthetic products.

Nonetheless, a single quarter’s results are not so important for long-term investors. Let us delve deeper to understand whether to buy, sell or hold the stock at present.

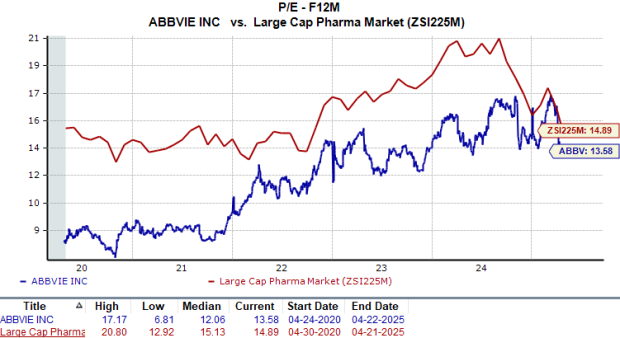

Shares of AbbVie have lost 2% year to date compared with the industry’s 4% decline. The stock has outperformed the sector and the S&P 500 index, as seen in the chart below.

From a valuation standpoint, AbbVie shares are not very cheap. Going by the price/earnings ratio, the company’s shares currently trade at 13.58 times forward 12-month earnings value, just slightly lower than 14.89 for the industry. AbbVie’s shares, however, are trading above their five-year mean of 12.06.

AbbVie has faced its biggest challenge — Humira biosimilar erosion — quite well by launching two other successful new immunology medicines, Skyrizi and Rinvoq, which are performing extremely well due to approvals in new indications. The company looks well-positioned for continued strong growth in the years ahead. Despite the increasing competitive pressure on cancer drug Imbruvica and declining sales of Juvederm fillers, the company saw a rapid return to sales growth in 2024.

Strong sales performance of drugs like Rinvoq, Skyrizi, Venclexta and Vraylar, coupled with significant contributions from newer drugs like Ubrelvy, Elahere, Epkinly and Qulipta, should keep driving the company’s top line.

Though AbbVie faced some key pipeline setbacks last year, it has been proactively pursuing strategic collaborations and partnership deals across several therapeutic areas to further strengthen its pipeline and drive long-term growth. Notably, the company recently forayed into the lucrative obesity space after in-licensing rights from Denmark-based Gubra for the latter’s experimental obesity drug.

Despite declining estimates and slightly expensive valuation, a solid pipeline and the prospect of growth in 2025 sales and profits are good enough reasons to stay invested in AbbVie’s stock. Any major decline in the company’s share price could be an opportunity for long-term investors to add the stock to their portfolio.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite