|

|

|

|

|||||

|

|

|

The Home Depot, Inc. HD continues to reinforce its long-term growth outlook through a disciplined and well-articulated capital allocation framework. Despite navigating a softer demand environment, the company has demonstrated resilience by prioritizing investments that strengthen its competitive moat while consistently returning cash to shareholders.

In the third quarter of fiscal 2025, the company invested approximately $900 million in capital expenditure. These investments were directed toward store expansions, supply-chain enhancements and technology upgrades aimed at improving productivity, fulfillment efficiency and customer experience. For fiscal 2025, HD expects capital expenditure to be 2.5% of sales, underscoring a steady commitment to strengthening core infrastructure and advancing the interconnected retail strategy.

Home Depot’s disciplined investment strategy is supported by solid liquidity and cash generation. At the end of the third quarter, the company held $1.68 billion in cash and cash equivalents. The operating cash flow for the first nine months of fiscal 2025 totaled $13 billion, reflecting resilient earnings generation and effective working capital management.

Alongside reinvestment, Home Depot remains focused on returning excess cash to shareholders. In the fiscal third quarter, the company paid out $2.3 billion in dividends. On Nov. 20, management announced a quarterly dividend of $2.30 per share, which was paid out on Dec. 18, highlighting the company’s consistency in capital returns.

The company’s long-term financial framework further reinforces this disciplined approach. While return on invested capital stood at 26.3% at the end of the third quarter, current investments are viewed as foundational to improving returns over time. Overall, with a dividend payout ratio of 61%, an annualized dividend yield of 2.4% and a free cash flow yield of 3.6%, Home Depot’s capital allocation strategy reflects a balanced focus on reinvestment, financial flexibility and sustained shareholder value creation.

Lowe's Companies, Inc. LOW maintained a disciplined capital allocation approach in third-quarter fiscal 2025, supported by healthy cash generation. Lowe’s delivered $687 million in operating cash flow, even after roughly $900 million in deferred tax payments, while investing $597 million in capex toward strategic growth initiatives.

Lowe’s returned $673 million to shareholders via dividends, reflecting confidence in cash durability. Post the FBM acquisition, cash and equivalents stood at $621 million, with leverage at 3.36X debt-to-EBITDAR. Management reaffirmed its commitment to deleverage toward a 2.75X target by mid-2027, balancing reinvestment, shareholder returns and balance sheet strength.

Floor & Decor Holdings, Inc. FND maintains a disciplined capital allocation strategy supported by a strong liquidity position. At the end of third-quarter fiscal 2025, Floor & Decor Holdings held $893.5 million in unrestricted liquidity, including $204.5 million in cash, providing ample financial flexibility. In the past nine months of fiscal 2025, Floor & Decor Holdings generated $257.8 million in operating cash flow despite inventory investments tied to expansion.

FND had earlier outlined its plan to invest $280-$300 million in fiscal 2025, primarily funding 20 store openings, distribution center expansions and technology investments. Management’s balanced approach prioritizes high-return growth while preserving balance sheet strength.

HD has seen its shares increase 17% in the past three months compared with the industry’s 18.8% growth.

From a valuation standpoint, Home Depot trades at a forward price-to-earnings ratio of 25.74, higher than the industry’s 23.53.

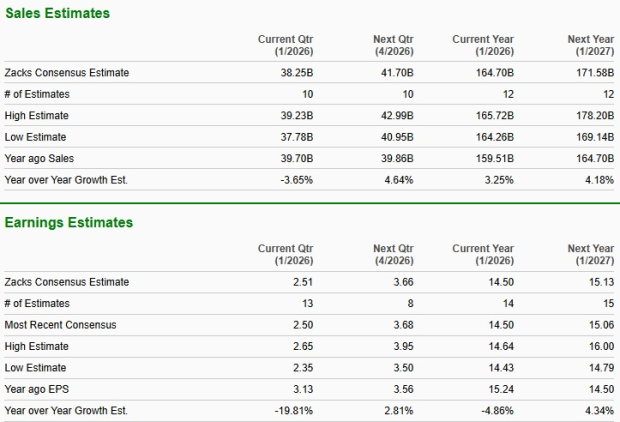

The Zacks Consensus Estimate for Home Depot’s current financial-year sales implies year-over-year growth of 3.3%, while the same for earnings per share suggests a decline of 4.9%. For the next fiscal year, the consensus estimate indicates a 4.2% rise in sales and 4.3% growth in earnings.

Home Depot currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-20 | |

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite