|

|

|

|

|||||

|

|

|

General Mills, Inc. GIS updated investors at the Consumer Analyst Group of New York conference, sharing progress on its Accelerate strategy while lowering its fiscal 2026 guidance due to a tougher consumer environment.

The company now expects organic net sales to decline 1.5% to 2% for the year compared with its earlier view of down 1% to up 1%. Adjusted operating profit and adjusted diluted earnings per share are projected to fall 16% to 20% in constant currency, wider than the previous expectation of a 10% to 15% decline. Free cash flow conversion is still expected to be at least 95% of adjusted after-tax earnings.

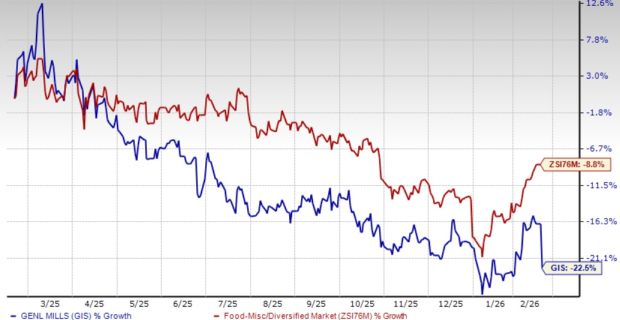

The revised guidance weighed on investor sentiment, with GIS shares falling nearly 7% on Feb. 17 following the announcement. The decline reflects concerns about slower demand recovery and continued pressure on margins. The Zacks Rank #4 (Sell) stock has tumbled 22.5% over the past year compared with the industry’s decline of 8.8%.

While reaffirming its long-term strategy, General Mills acknowledged that consumer demand remains uneven. Lower and middle-income shoppers are increasingly buying products on promotion rather than at regular prices. Although promotional activity has not risen significantly, purchases are higher during discount periods, making volume recovery more expensive.

In the second quarter of fiscal 2026, GIS’ organic net sales declined 1%, while organic volume was flat, showing improvement from the first quarter. North America Retail posted organic volume growth for the first time in several years, helped by base price adjustments across a large part of the portfolio and higher media spending. Adjusted operating profit fell 20% in constant currency, and adjusted earnings per share declined 21%, mainly due to higher input costs and increased brand investment.

General Mills continues to invest in product innovation to drive growth. The company expects new products to contribute roughly 25% more sales in fiscal 2026 compared with the prior year. Its innovation pipeline focuses on protein-rich offerings, bold flavors and products aligned with health and wellness trends. The North America Pet segment is also seeing investment to strengthen core brands and expand newer offerings.

At the same time, cost savings remain a priority. Productivity initiatives are expected to deliver meaningful savings in the cost of goods sold this year, helping support margins and cash flow even as profits face near-term pressure.

The updated guidance highlights the challenges of operating in a cautious spending environment. While the company is making progress on volumes and innovation, sustained improvement in demand and profitability will likely be the key to rebuilding investor confidence.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Hershey’s current financial-year sales and earnings indicates growth of 4.4% and 27.1%, respectively, from the prior-year reported levels. HSY delivered a trailing four-quarter earnings surprise of 17.2%, on average.

The Simply Good Foods Company SMPL, a consumer-packaged food and beverage company, engages in the development, marketing and sale of snacks, meal replacements and other products in North America and internationally. It sports a Zacks Rank #1 at present. SMPL delivered a trailing four-quarter earnings surprise of 5.5%, on average.

The Zacks Consensus Estimate for Simply Good Foods’ current fiscal-year earnings implies growth of 1.6% from the year-ago reported figures.

Ollie's Bargain Outlet Holdings, Inc. OLLI operates as a retailer of closeout merchandise and excess inventory in the United States. OLLI currently has a Zacks Rank #2 (Buy). Ollie's Bargain delivered a trailing four-quarter earnings surprise of 5.2%, on average.

The Zacks Consensus Estimate for Ollie's Bargain’s fiscal 2025 sales and earnings suggests an increase of 16.7% and 17.7%, respectively, from the previous year’s reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite