|

|

|

|

|||||

|

|

|

Dollar General has had an impressive run over the past six months as its shares have beaten the S&P 500 by 27.2%. The stock now trades at $149.55, marking a 33.2% gain. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Dollar General, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the momentum, we're sitting this one out for now. Here are three reasons why DG doesn't excite us and a stock we'd rather own.

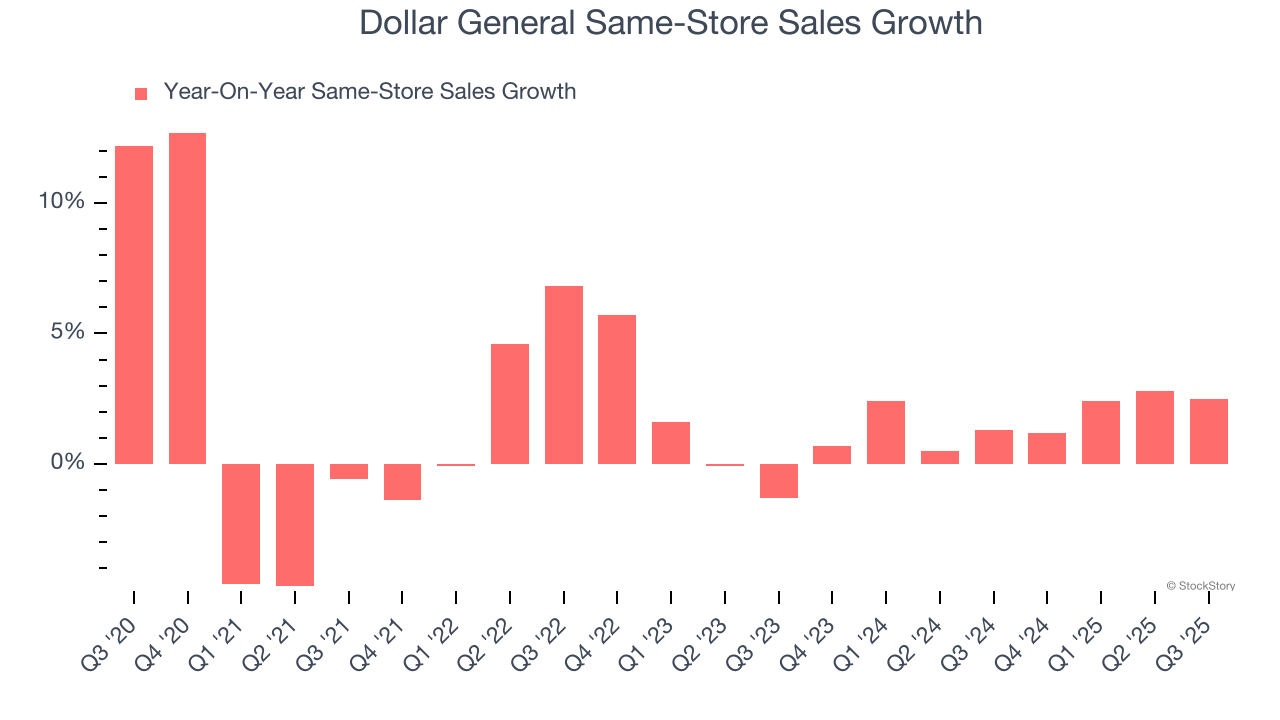

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Dollar General’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.7% per year.

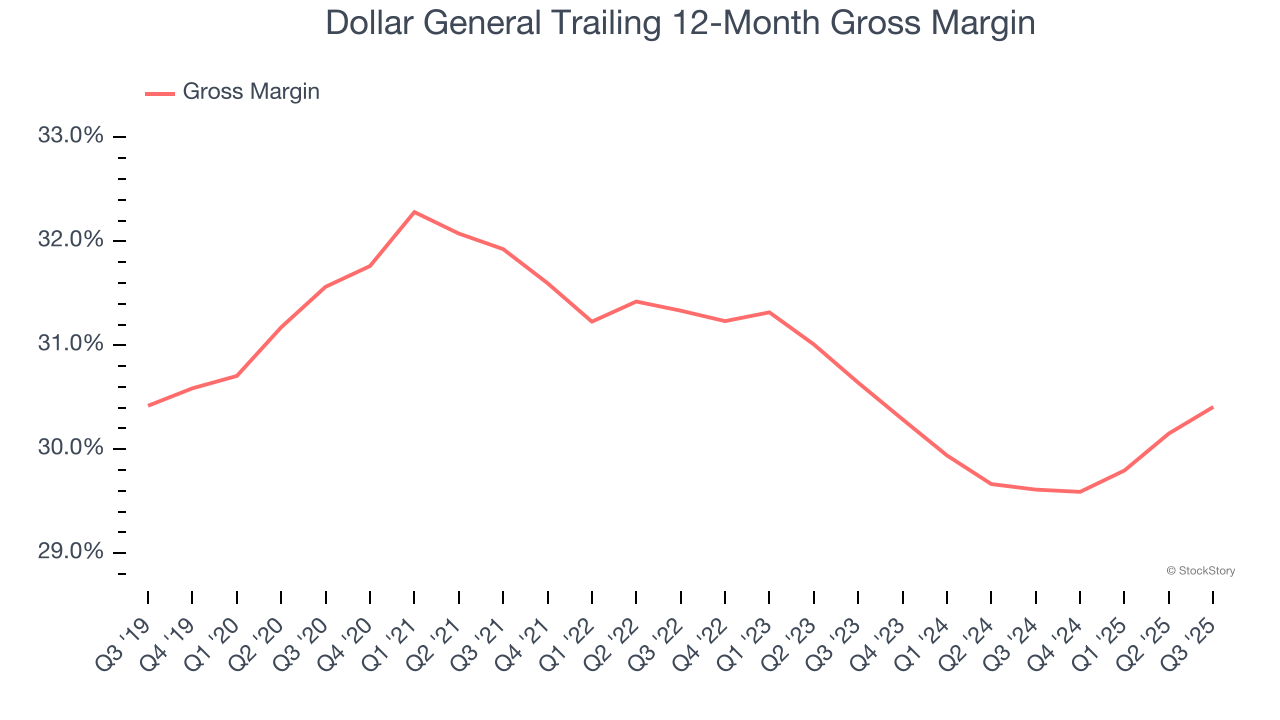

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Dollar General has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 30% gross margin over the last two years. Said differently, Dollar General had to pay a chunky $69.98 to its suppliers for every $100 in revenue.

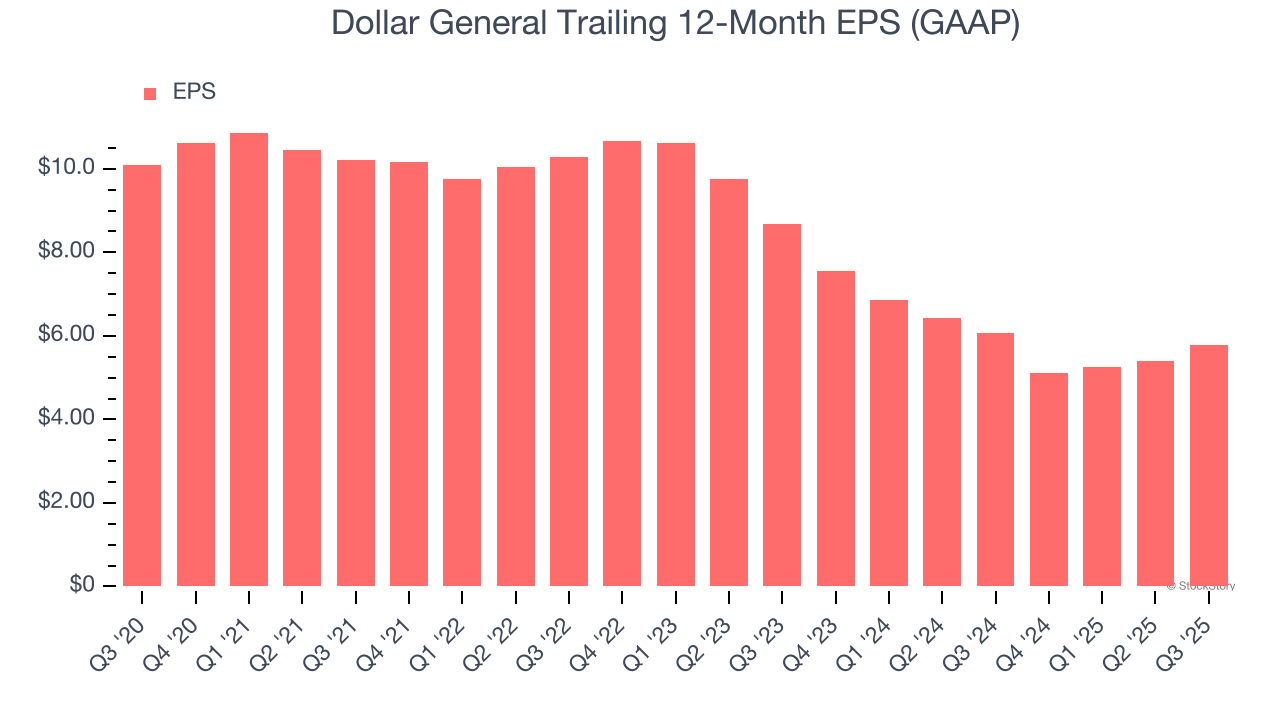

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Dollar General, its EPS declined by 17.4% annually over the last three years while its revenue grew by 5.1%. This tells us the company became less profitable on a per-share basis as it expanded.

Dollar General isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 22× forward P/E (or $149.55 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Apr-14 | |

| Apr-13 | |

| Apr-13 | |

| Apr-13 | |

| Apr-10 | |

| Apr-10 | |

| Apr-09 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-27 | |

| Mar-27 | |

| Mar-26 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite