|

|

|

|

|||||

|

|

|

Over the past six months, Kirby has been a great trade, beating the S&P 500 by 23%. Its stock price has climbed to $127.79, representing a healthy 29.7% increase. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Following the strength, is KEX a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Transporting goods along all U.S. coasts, Kirby (NYSE:KEX) provides inland and coastal marine transportation services.

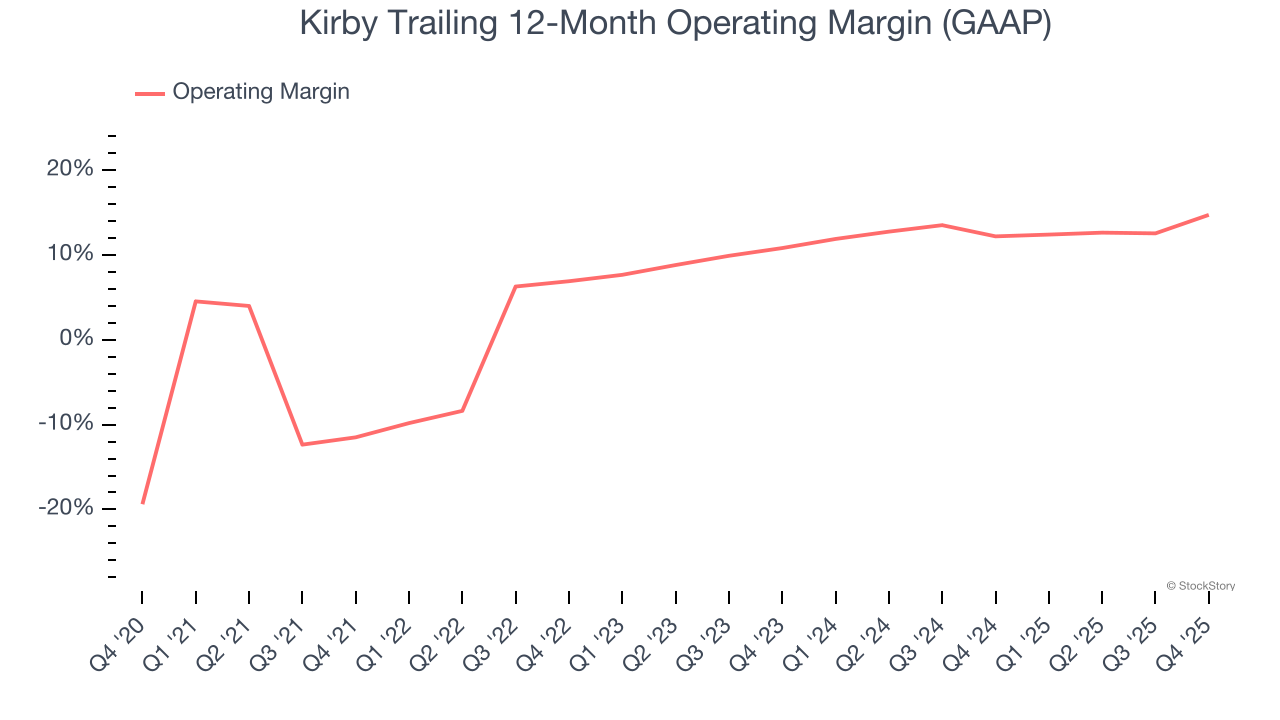

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Kirby’s operating margin rose by 26.2 percentage points over the last five years, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was 14.8%.

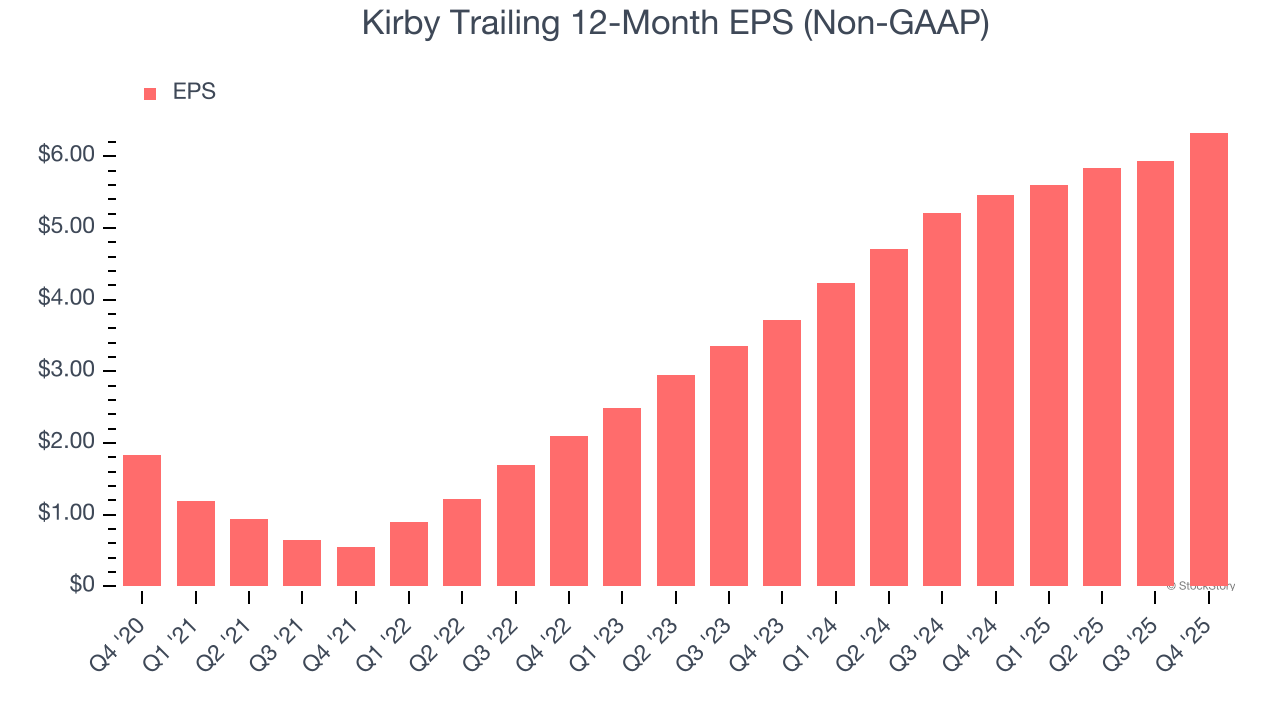

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Kirby’s EPS grew at an astounding 28% compounded annual growth rate over the last five years, higher than its 9.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

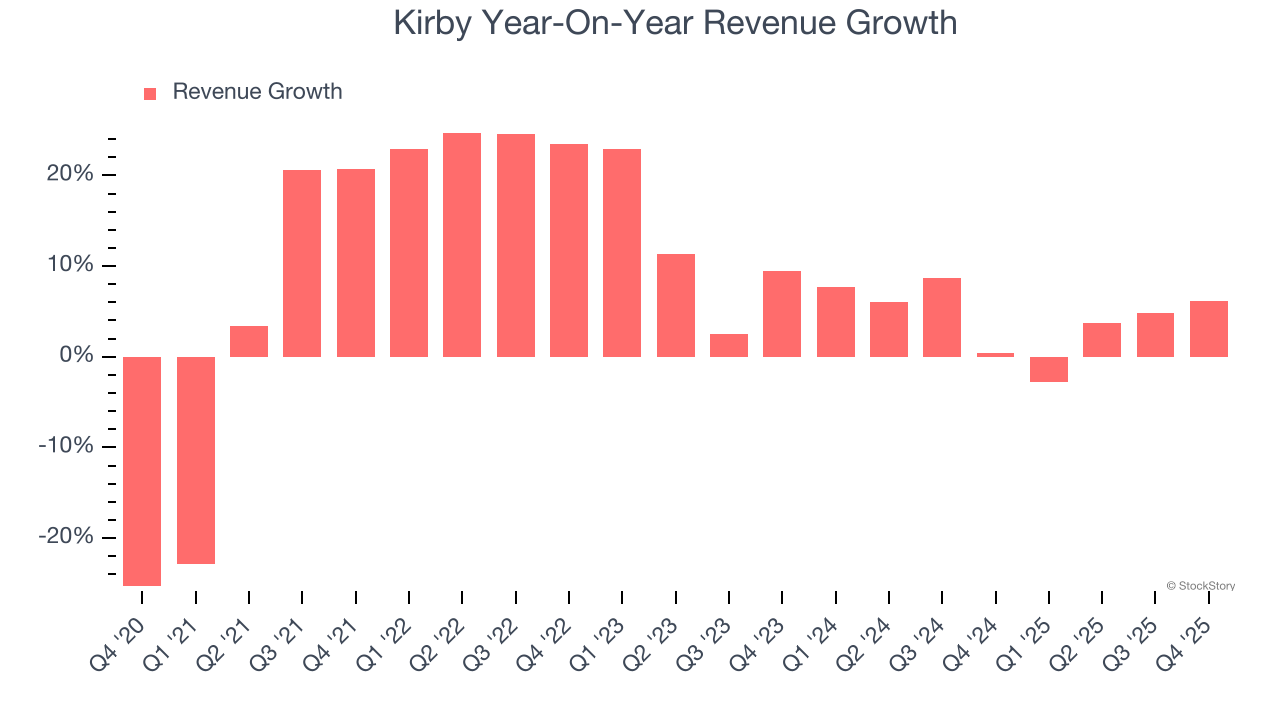

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kirby’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Kirby has huge potential even though it has some open questions, and with its shares beating the market recently, the stock trades at 18.7× forward P/E (or $127.79 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-10 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jun-29 | |

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-21 | |

| Mar-31 | |

| Mar-31 | |

| Feb-23 | |

| Feb-20 | |

| Feb-18 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite