|

|

|

|

|||||

|

|

|

Since August 2025, Preferred Bank has been in a holding pattern, posting a small loss of 1.8% while floating around $92.33. The stock also fell short of the S&P 500’s 6.5% gain during that period.

Is there a buying opportunity in Preferred Bank, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We're sitting this one out for now. Here are three reasons there are better opportunities than PFBC and a stock we'd rather own.

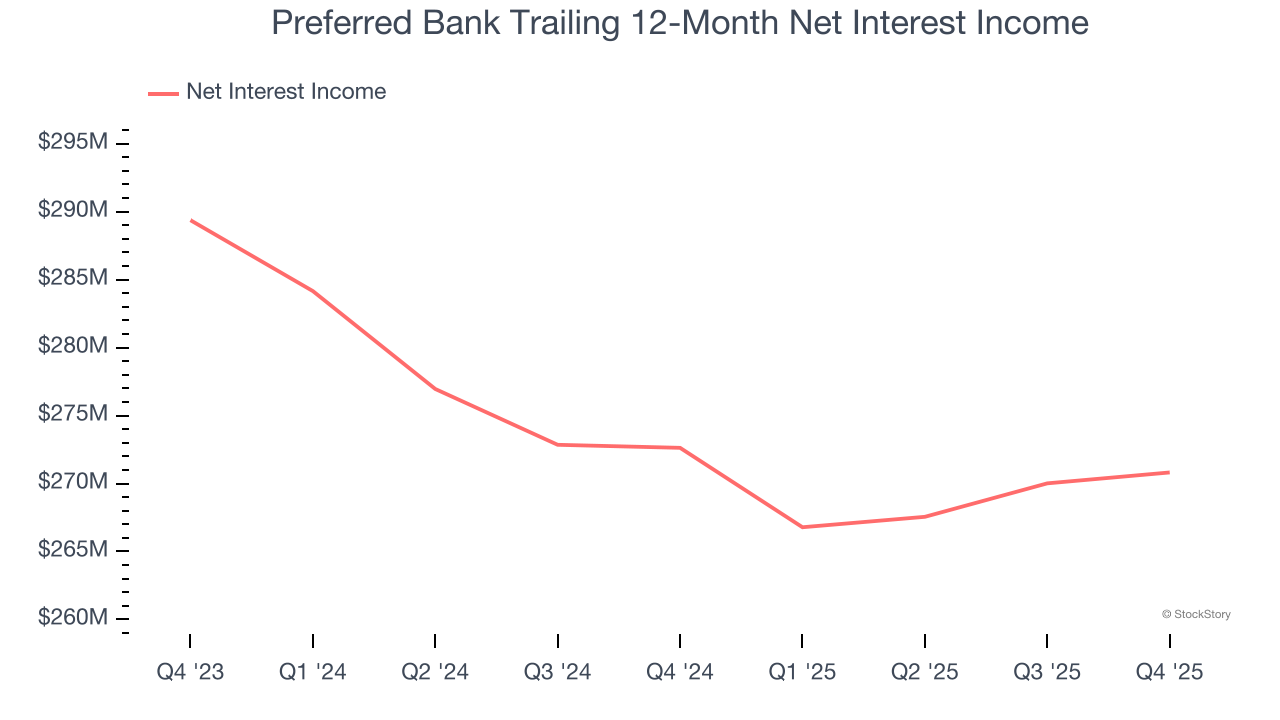

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Preferred Bank’s net interest income has grown at a 9.2% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue.

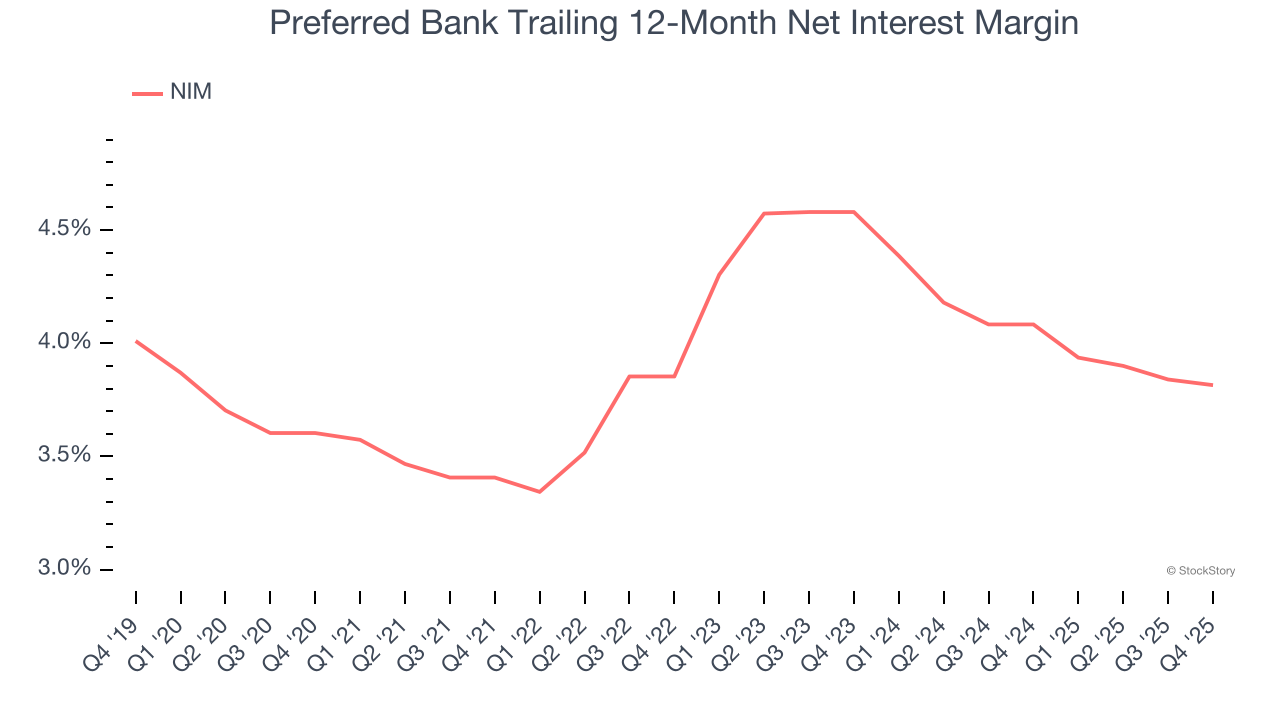

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, Preferred Bank’s net interest margin averaged 3.9%. However, its margin contracted by 76.5 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Preferred Bank either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

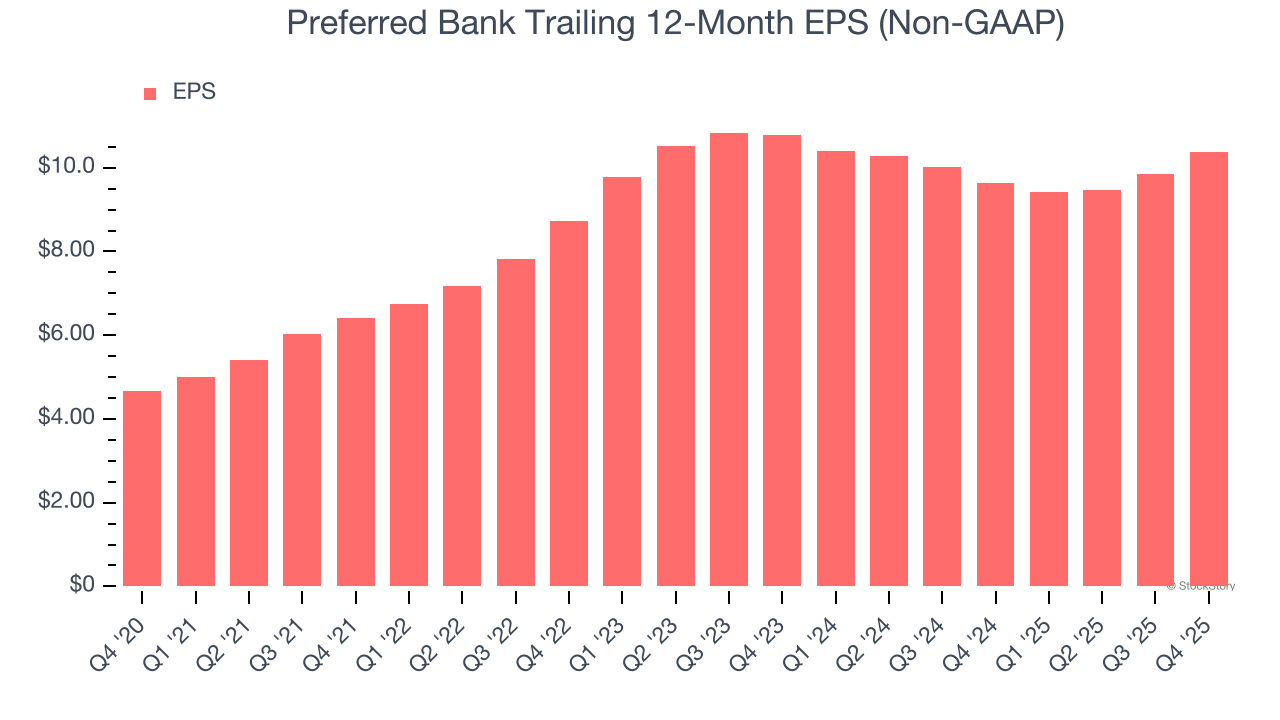

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Preferred Bank, its EPS and revenue declined by 1.8% and 1.2% annually over the last two years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Preferred Bank’s low margin of safety could leave its stock price susceptible to large downswings.

Preferred Bank isn’t a terrible business, but it isn’t one of our picks. With its shares lagging the market recently, the stock trades at 1.3× forward P/B (or $92.33 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. Let us point you toward the most dominant software business in the world.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-09 | |

| Jun-17 | |

| May-20 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-20 | |

| Apr-08 | |

| Mar-18 | |

| Feb-23 | |

| Feb-22 | |

| Feb-10 | |

| Jan-29 | |

| Jan-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite