|

|

|

|

|||||

|

|

|

Over the last six months, OFG Bancorp’s shares have sunk to $41.38, producing a disappointing 7.1% loss - a stark contrast to the S&P 500’s 7.3% gain. This might have investors contemplating their next move.

Is there a buying opportunity in OFG Bancorp, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons there are better opportunities than OFG and a stock we'd rather own.

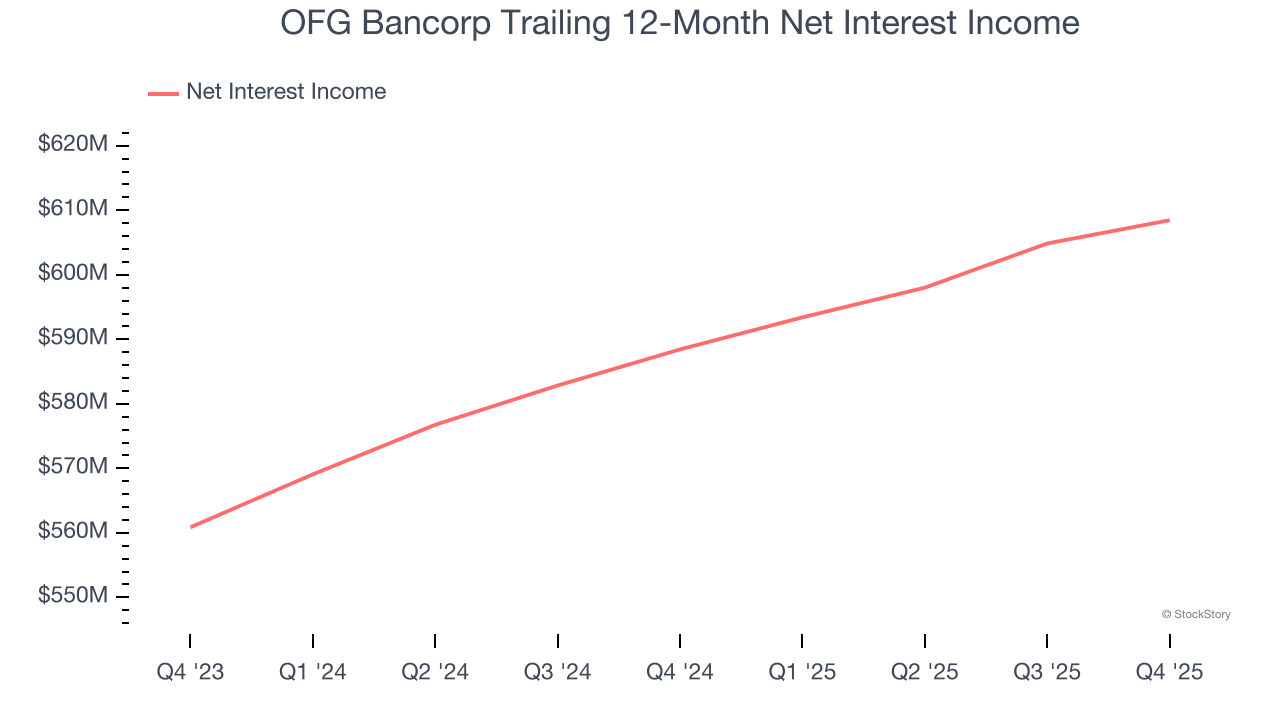

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

OFG Bancorp’s net interest income has grown at a 8.3% annualized rate over the last five years, worse than the broader banking industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect OFG Bancorp’s net interest income to drop by 2.2%, a decrease from its 4.2% annualized growth for the past two years. This projection is below its 4.2% annualized growth rate for the past two years.

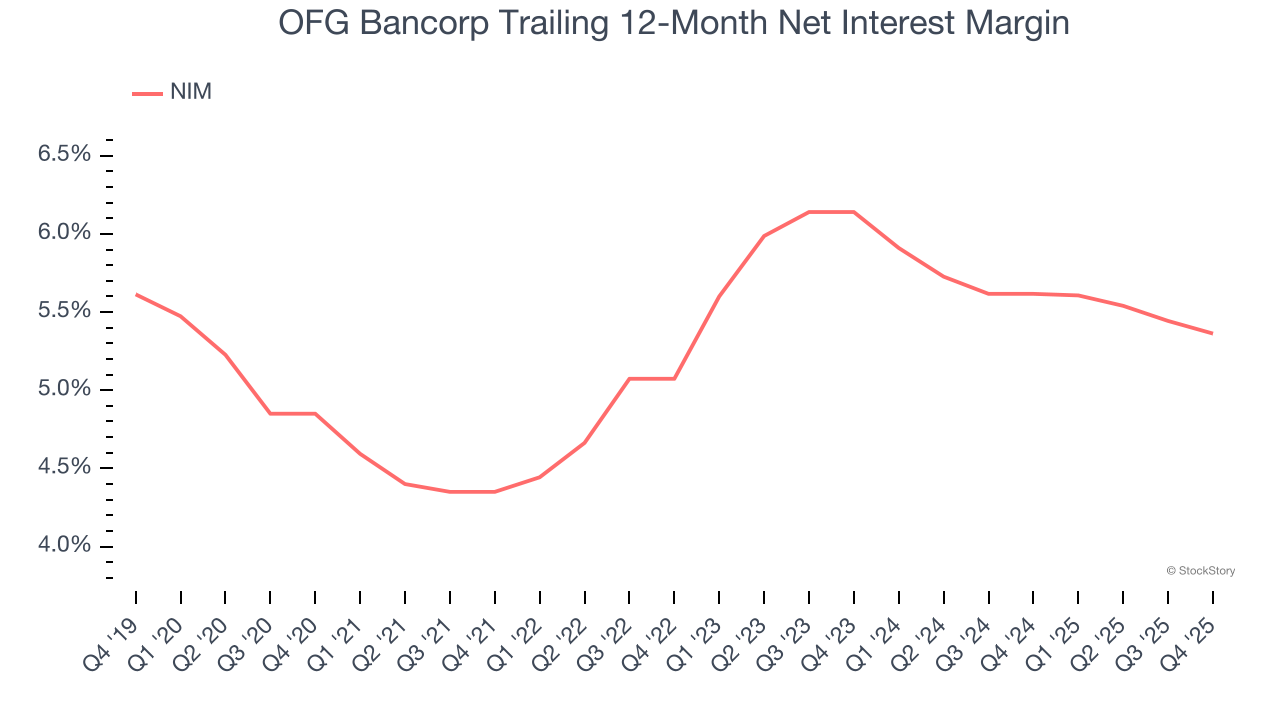

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, OFG Bancorp’s net interest margin averaged 5.5%. However, its margin contracted by 77.8 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean OFG Bancorp either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

OFG Bancorp’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 1.2× forward P/B (or $41.38 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-12 | |

| Jun-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-21 | |

| Mar-23 | |

| Mar-02 | |

| Feb-23 | |

| Feb-18 | |

| Feb-16 | |

| Feb-03 | |

| Feb-02 | |

| Jan-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite