|

|

|

|

|||||

|

|

|

Novo Nordisk NVO and Eli Lilly LLY lead the diabetes and obesity market, driven by blockbuster GLP-1 therapies. Lilly sells its dual GIP/GLP-1 agonist tirzepatide as Mounjaro for type II diabetes and as Zepbound for obesity. Novo Nordisk markets semaglutide as Ozempic and Rybelsus for type 2 diabetes, and as Wegovy for weight management.

In 2025, Lilly’s Cardiometabolic Health unit, which includes Mounjaro and Zepbound, delivered nearly $40 billion in revenues. Novo Nordisk’s Diabetes and Obesity segment generated about $44.0 billion (DKK 289.456 billion). The Cardiometabolic Health segment contributes roughly 78% of Lilly’s total sales, compared with a much higher 93.6% for NVO.

So, which stock looks more attractive now? A closer review of their financial strength, pipeline depth, competitive positioning and valuation can help investors decide.

Lilly has seen tremendous success with Mounjaro and Zepbound, with demand rising rapidly. These therapies account for more than 50% of the company’s total revenues.

In 2025, the drugs generated combined sales of $36.5 billion, comprising around 56% of the company’s total revenues. Robust growth trends in the U.S. incretin analogs market and positive uptake trends of Mounjaro and Zepbound in new international markets led to strong sales growth in 2025, with the positive trend expected to continue in 2026.

In addition to Mounjaro and Zepbound, Lilly has secured approvals for several other new therapies over the past few years. These include Omvoh, Jaypirca, Ebglyss and Kisunla. These newly approved drugs are also contributing to Lilly’s revenue growth. Lilly expects its new drugs, Mounjaro, Zepbound, Ebglyss, Jaypirca, Inluriyo, Kisunla and Omvoh to drive sales growth in 2026.

Lilly is investing broadly in obesity and has several new molecules currently in clinical development with a range of oral and injectable medications with different mechanisms of action. A key drug in its obesity pipeline is the once-daily oral GLP-1 small molecule called orforglipron.

Lilly has announced positive data across six studies on orforglipron in obesity and type 2 diabetes. It filed regulatory applications in the United States, the EU, and several other countries in late 2025/early 2026 seeking approval for orforglipron in obesity. Lilly expects to launch orforglipron for obesity in the United States during the second quarter of 2026 and in most international markets during 2027.

Oral pills will be a more convenient alternative to the once-weekly injectable obesity treatments like Zepbound and Novo Nordisk’s Wegovy. Novo Nordisk gained approval for an oral version of Wegovy in December 2025 and launched the pill in January 2026.

The company is also evaluating another key candidate, triple-acting incretin, retatrutide (which combines GLP-1, GIP and glucagon), in type II diabetes and obesity, along with other indications like obstructive sleep apnea, knee osteoarthritis and chronic low back pain, in late-stage studies.

In the past couple of years, Lilly upped its efforts to diversify beyond GLP-1 drugs by expanding into cardiovascular, oncology and neuroscience areas. In 2025, it announced several M&A deals.

Lilly has its share of problems. Prices of most of Lilly’s products are declining in the United States. Price is expected to continue to be a drag on top-line growth in the low to mid-teens percentage in 2026. Rising competition in the GLP-1 diabetes/obesity market is a key headwind. Also, sales of late-life cycle products like Trulicity, Taltz and Verzenio are expected to be flat or down in 2026.

The Wegovy pill gives NVO the first-to-market advantage and will initially bring in additional revenues, which may hurt Lilly’s market share. However, we believe Lilly may be able to close the gap fast, once its own oral obesity pill, orforglipron, is approved by the FDA in 2026.

Smaller biotechs like Structure Therapeutics GPCR and Viking Therapeutics VKTX are also developing oral GLP-1 drugs for treating obesity.

Viking Therapeutics’ dual GIPR/GLP-1 receptor agonist, VK2735, is being developed both as oral and subcutaneous formulations for the treatment of obesity. Viking plans to advance oral VK2735 into phase III development for obesity in the third quarter of 2026.

Structure Therapeutics’ ACCESS study on its orally GLP-1 RA, aleniglipron, for obesity, met its primary and all key secondary endpoints. Structure Therapeutics expects to initiate the late-stage program of aleniglipron in obesity around mid-2026.

Novo Nordisk has a strong presence in the Diabetes care market, with one of the broadest diabetes portfolios in the industry. Novo Nordisk’s success in recent years has been driven by the sales of Ozempic and Rybelsus (oral) for type II diabetes, and Wegovy for obesity. Ozempic and Wegovy are the major revenue drivers. However, their sales slowed down in 2025 due to increased competition from Lilly, widespread compounded semaglutide use in the United States, pricing pressure and foreign-exchange headwinds. There is not much improvement expected in 2026, with sales and operating profit expected to decline 5-13% at CER in 2026.

The launch of oral Wegovy raised hopes of a meaningful new growth driver for NVO. However, the weak 2026 guidance has raised uncertainty that the oral pill can bring any meaningful top-line growth, at least until Lilly launches its oral pill.

In several clinical studies, Lilly’s tirzepatide products have shown superior weight-loss efficacy versus NVO’s semaglutide medicines.

Novo Nordisk is expanding access to Wegovy through broader distribution and partnerships with major U.S. pharmacies, telehealth providers, and proprietary and third-party platforms to ensure patients can obtain authentic, FDA-approved treatments. If successful, this strategy, along with NVO’s legal actions and tighter FDA oversight, could help mitigate the compounded alternatives problem.

Novo Nordisk is expanding semaglutide's reach through new indications. Wegovy injection is now approved for reducing major cardiovascular events, easing HFpEF symptoms and relieving osteoarthritis-related knee pain in obesity. Rybelsus’ label in the United States and the EU has been expanded to include cardiovascular benefits in diabetes patients.

Novo Nordisk is also developing several next-generation obesity candidates in its pipeline. The most advanced candidate in Novo Nordisk’s pipeline is CagriSema injection, a fixed-dose combination of cagrilintide and Wegovy. The company has already filed a regulatory application for the candidate to treat obesity based on data from the REDEFINE 1 and REDEFINE 2 pivotal studies. On Monday, NVO announced data from the head-to-head phase III REDEFINE 4 study, in which CagriSema showed less weight loss than Zepbound, further reducing investor confidence about the company’s potential to regain the obesity market share.

Novo Nordisk also plans to advance another next-generation candidate, amycretin, for weight management into late-stage development. The phase III program on amycretin is planned to be initiated during the first quarter of 2026.

Beyond its GLP-1 portfolio, Novo Nordisk is broadening its presence in rare diseases.

The Zacks Consensus Estimate for LLY’s 2026 sales and EPS implies a year-over-year increase of 25.3% and 39.9%, respectively. The Zacks Consensus Estimate for 2026 has risen from $33.18 to $33.86 per share over the past 30 days, while that for 2027 has risen from $41.48 to $41.96 per share over the same timeframe.

The Zacks Consensus Estimate for Novo Nordisk’s 2026 sales and EPS implies a year-over-year decrease of 2.6% and 14.9%, respectively. EPS estimates for 2026 have risen from $3.36 per share to $3.37 per share, while those for 2027 have declined from $3.52 per share to $3.35 per share.

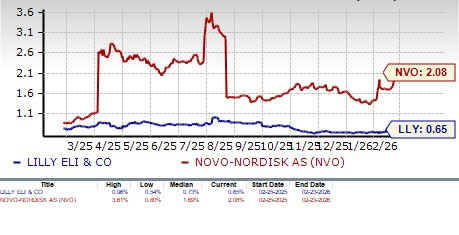

In the past year, while LLY’s stock has risen 17.4%, Novo Nordisk’s stock has plunged 56.4%. The industry has risen10.8% in the said time frame.

Lilly is more expensive than Novo Nordisk, going by the price/earnings ratio. Lilly’s shares currently trade at 30.18 forward earnings, higher than 11.76 for NVO. Lilly’s stock is also priced higher than the industry’s 18.45, while NVO trades below the same. Both NVO and LLY trade below their 5-year mean.

Lilly’s dividend yield is 0.7%, while NVO’s is much higher at around 2.1%.

Lilly has a Zacks Rank #3 (Hold), while Novo Nordisk has a Zacks Rank #4 (Sell), which clearly shows that Lilly is the winner.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Slowing demand, intensifying competition, pricing pressure, rising costs and pipeline setbacks have resulted in the stock crashing 56.3% in the past year.

In sharp contrast, exceptional growth from Mounjaro and Zepbound has made Lilly the largest drugmaker. It is the first and only drugmaker to hit a $1 trillion market cap. It delivered robust financial performance in 2025 with revenues surging 45% and EPS growing 86%. Expectations for continued growth in 2026 remain high. Lilly, with its significant price appreciation, its solid product and pipeline portfolio, robust 2026 sales outlook and bullish analyst sentiment, outshines NVO in every way.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 9 hours | |

| 13 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite