|

|

|

|

|||||

|

|

|

Digital payments are on the rise around the world as both consumers and businesses are embracing card-based, real-time and embedded finance solutions. In this changing landscape, factors like scale, network reach, credit exposure and monetization models play a bigger role in shaping the competitive dynamics within the payments ecosystem. Companies such as Visa Inc. V and Affirm Holdings, Inc. AFRM operate at different layers of this ecosystem but intersect at the point of digital transaction enablement.

Visa operates one of the largest payment networks in the world, earning most of its revenues from processing transactions and handling cross-border volumes. On the other hand, Affirm specializes in buy now, pay later (BNPL) financing, making money through merchant fees and consumer loans.

V’s asset-light network model prioritizes scale and operating leverage, while AFRM’s credit-driven platform relies on underwriting and merchant partnerships for growth. These differences shape revenue stability, margin structure and exposure to credit cycles. Let’s dive deep and closely compare the fundamentals of the two stocks to determine which stock offers greater upside right now.

Visa, boasting a market cap of $582.6 billion, runs a global payment network that processes transactions without taking credit risk. Its revenues largely hinge on payment volumes, cross-border transactions and value-added services. A standout feature of Visa is its extensive international reach, with acceptance in more than 200 countries and territories. This broad presence allows the company to capitalize on cross-border travel, the resurgence of tourism and the increasing digital adoption in emerging markets.

Cross-border transactions are proving to be a vital growth driver for global payment networks, fueled by the uptick in international travel and the ongoing boom in cross-border e-commerce. In the first quarter of fiscal 2026, the company reported growth of 11% year over year in cross-border volumes (excluding intra-Europe), reflecting the strength of its diverse global network and a favorable revenue mix.

Beyond volumes, Visa’s asset-light model continues to demonstrate operating leverage. The company delivered strong operating margins during the quarter, aided by disciplined expense management and a favorable shift toward value-added services. Its adjusted operating income rose 13.9% to $7.5 billion, keeping V’s adjusted operating margins close to 69% in the first quarter of fiscal 2026. It beat earnings in each of the past four quarters with an average surprise of 2.1%.

Visa Inc. price-consensus-eps-surprise-chart | Visa Inc. Quote

Visa is focused on expanding money movement capabilities across consumer payments, B2B flows and real-time solutions. It has expanded AI-powered commercial payment solutions, strengthened tokenization and biometric authentication capabilities and advanced embedded finance integrations, positioning its network to support secure, scalable and innovation-driven digital commerce growth.

Additionally, V’s strong cash position enables substantial share buybacks and dividend payouts and supports inorganic growth and financial stability. With $14.8 billion in cash, the company maintains a solid capital position. Its long-term debt-to-capital of 33.6% is lower than the industry’s average of 37.8% and AFRM’s 72%. Visa returned $3.8 billion to its shareholders through share repurchases in the fiscal first quarter.

However, escalating operating expenses and higher rebates and client incentives will likely impact its growth potential. In the first quarter of fiscal 2026, V’s operating expenses rose 27% year over year. In the United States, the Department of Justice earlier accused the company of using its dominance to overcharge merchants. European and U.K. regulators are also investigating cross-border and merchant fees, potentially leading to fee caps or new compliance requirements, which could dent revenue growth in the region.

With a market capitalization of $17 billion, AFRM represents a scaled yet still growth-oriented player within the fintech and consumer credit space. As the BNPL model evolves, the company is expanding beyond point-of-sale financing toward a more integrated payments and lending platform built on proprietary underwriting and merchant partnerships. Its AI-powered underwriting tools and real-time risk assessment give it the agility to approve users more accurately and scale profitably.

By teaming up with giants like Amazon, Shopify, Apple Pay and Williams-Sonoma, AFRM is seamlessly integrated into the checkout process for millions of shoppers. It extended its partnership with Amazon till January 2031 to provide flexible payment solutions to customers, while it extended its collaboration with Wayfair to bring financial products to shoppers in the U.K. and Canada.

In the second quarter of fiscal 2026, Affirm generated solid Gross Merchandise Volume (GMV) growth of 36.6% year over year, supported by higher repeat usage and deeper merchant integrations. An increasing contribution from returning customers pointed to improving engagement trends and stronger ecosystem stickiness, helping drive revenues. In second-quarter fiscal 2026, its revenues rose 30% year over year to $1.1 billion. Its active consumer count increased to 25.8 million, and transactions per active consumer grew by 20%, showing rising engagement and repeat usage. It beat earnings in each of the past four quarters with an average surprise of 83.5%.

Affirm Holdings, Inc. price-consensus-eps-surprise-chart | Affirm Holdings, Inc. Quote

The company is expanding its reach into everyday spending categories and improving distribution through debit-linked and embedded finance offerings. These efforts are aimed at increasing transaction frequency, improving funding flexibility and supporting more balanced, scalable long-term growth. However, it continues to face a rise in total expenses. Total operating expenses rose 15.5% year over year in the second quarter, mainly due to higher funding costs, provision for credit losses, loss on loan purchase commitment and processing and servicing expenses.

The Zacks Consensus Estimate for Affirm's bottom line is comparably favorable at this stage. The consensus estimate for V’s fiscal 2026 earnings indicates an 11.9% increase from a year ago, while the same for revenues suggests 11.3% growth. On the other hand, the Zacks Consensus Estimate for Affirm's fiscal 2026 EPS indicates 626.7% year-over-year improvement, and the same for revenues signals a 28.3% rise.

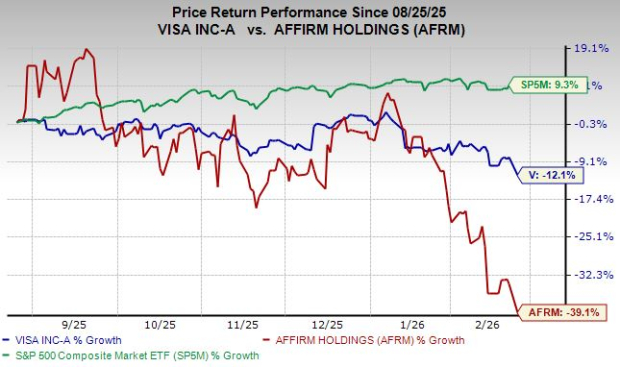

Over the past six months, Visa has shed less value than AFRM. However, the S&P 500 increased 9.3% during this time.

On a price-to-sales basis, Visa sits at 12X forward revenues, significantly above Affirm’s multiple of 3.29X. AFRM’s cheaper P/S multiple leaves room for significant growth as business expansion accelerates.

Visa currently trades below its average analyst price target of $402.31, implying a 25.4% potential upside from current levels. AFRM also trades below its average analyst price target of $85.73, implying an attractive 67.8% potential upside from current levels.

Both V and AFRM bring distinct strengths to the digital payments ecosystem. While Visa offers scale, stability and consistent margin strength through its asset-light global network, Affirm is delivering faster revenue growth, rising engagement and stronger earnings acceleration, supported by expanding merchant partnerships and increasing transaction frequency.

For investors seeking rapid future gains rather than stability, Affirm appears to have the edge at this stage of the cycle. Its lower valuation multiple combined with higher growth expectations enhances its risk-reward profile, even though both companies currently carry a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite