|

|

|

|

|||||

|

|

|

Shareholders of Agilysys would probably like to forget the past six months even happened. The stock dropped 33.6% and now trades at $71.97. This might have investors contemplating their next move.

Is there a buying opportunity in Agilysys, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we're swiping left on Agilysys for now. Here are three reasons you should be careful with AGYS and a stock we'd rather own.

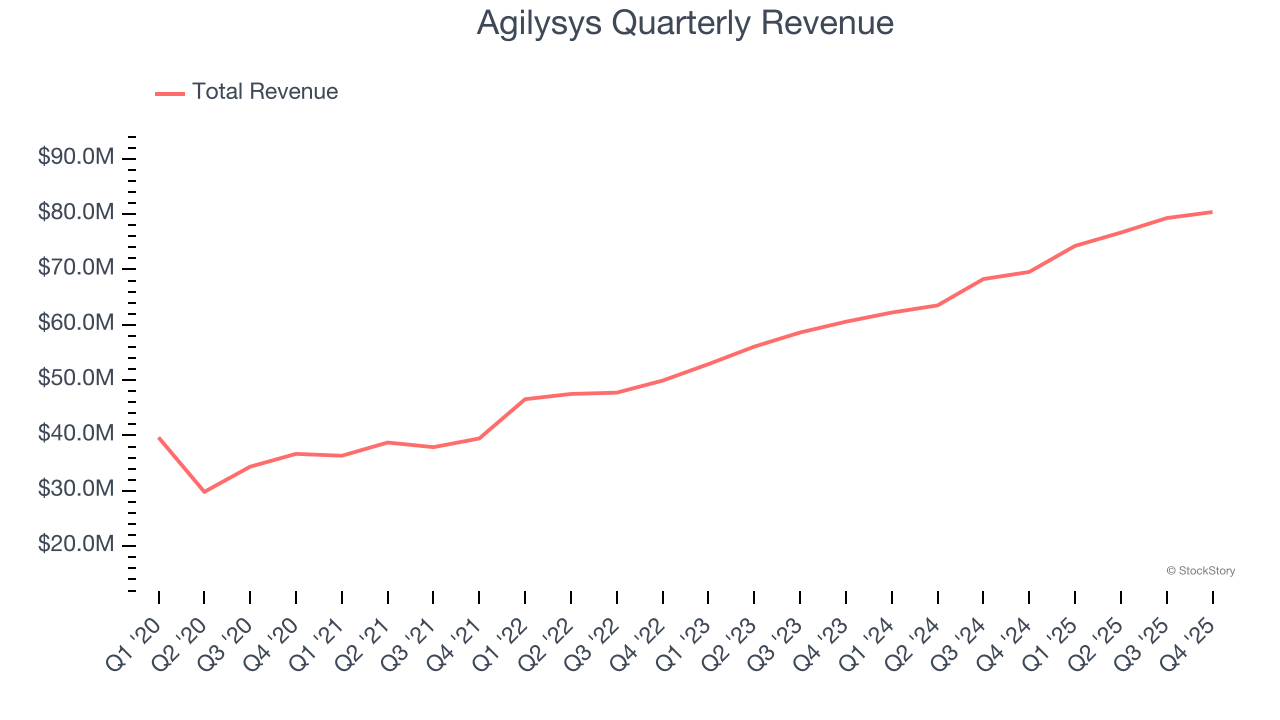

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Agilysys grew its sales at a 17.2% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

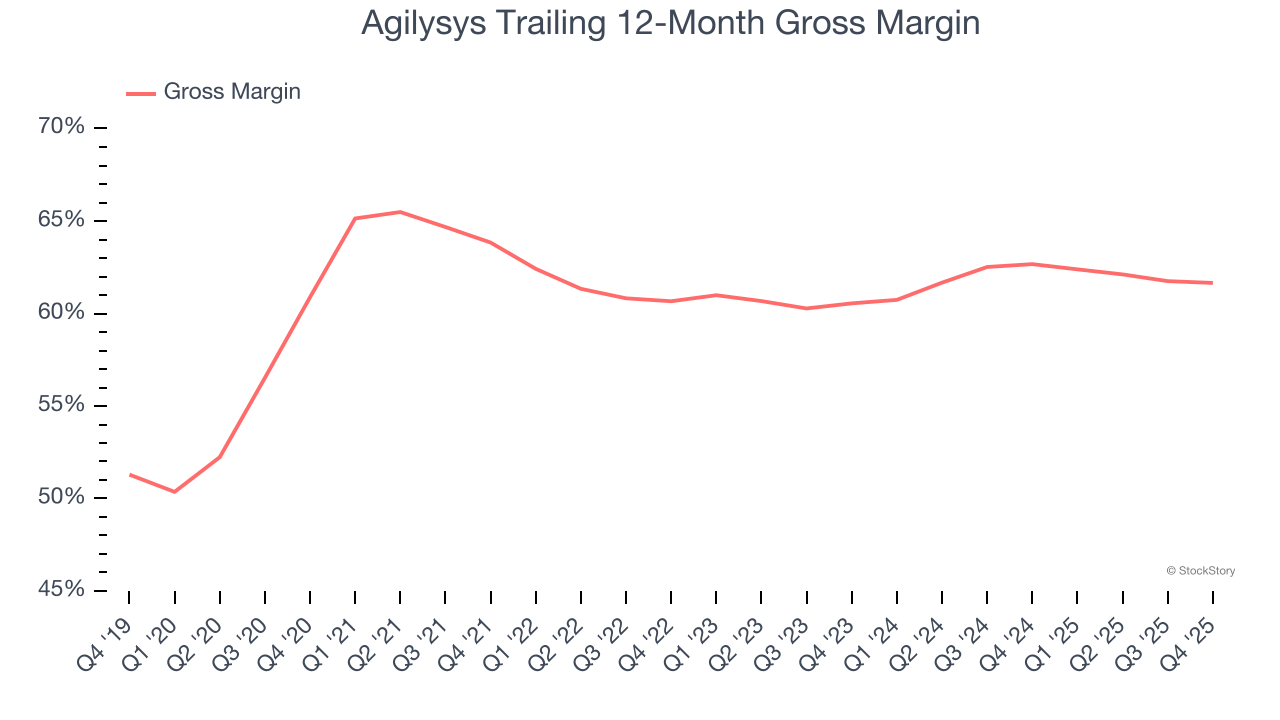

For software companies like Agilysys, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Agilysys’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 61.7% gross margin over the last year. That means Agilysys paid its providers a lot of money ($38.33 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Agilysys has seen gross margins improve by 1.1 percentage points over the last 2 year, which is slightly better than average for software.

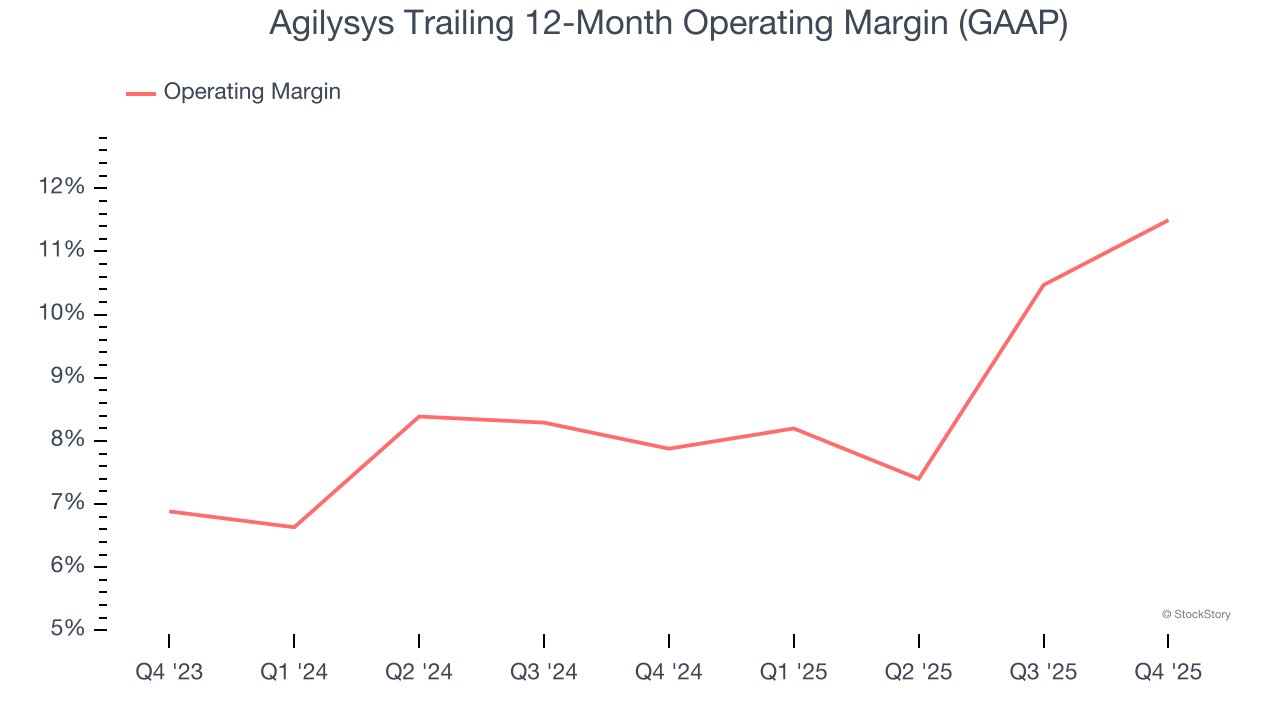

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Looking at the trend in its profitability, Agilysys’s operating margin rose by 3.6 percentage points over the last two years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 11.5%.

Agilysys isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 5.8× forward price-to-sales (or $71.97 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-31 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jun-30 | |

| Jun-11 | |

| Jun-03 | |

| Jun-03 | |

| Jun-02 | |

| Jun-01 | |

| May-27 | |

| May-19 | |

| May-19 | |

| May-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite