|

|

|

|

|||||

|

|

|

Both AppLovin Corporation APP and Arm Holdings ARM are technology-driven companies capitalizing on the AI revolution. AppLovin leverages advanced AI-powered advertising algorithms and app monetization platforms, while ARM underpins AI innovation through its cutting-edge chip architectures that power high-performance AI hardware. This positions both as innovation-centric opportunities aligned with the accelerating adoption of artificial intelligence across industries.

Their common focus on deploying AI to enhance efficiency, scalability and measurable business outcomes places them at the forefront of a transformative technological era, one in which artificial intelligence is increasingly becoming a core driver of competitive differentiation and sustainable long-term growth.

Artificial intelligence is not an add-on for AppLovin; it is core to its model. The company’s proprietary optimization engine, AXON, continuously analyzes campaign-level data to refine targeting and performance outcomes. Over time, this feedback loop enhances advertiser returns and reinforces platform stickiness.

Equally important is its MAX mediation platform, which connects publishers with multiple sources of advertising demand. As more participants join the ecosystem, outcomes improve across the network. This creates a reinforcing cycle: improved performance attracts more advertisers and developers, which, in turn, strengthens the data advantage.

The resulting moat is not simply technological; it is data-driven and ecosystem-based. Replicating years of behavioral insights and campaign intelligence is difficult, even for well-capitalized competitors.

APP’s recent financial performance underscores efficient execution: strong top-line acceleration paired with high operating efficiency. Revenues reached $1.7 billion, rising 66% year over year in the fourth quarter of 2025. Adjusted EBITDA grew 82% to $1.4 billion, translating to an 84% margin.

This dynamic signals a business that is not merely growing, but doing so with increasing efficiency. When revenue gains translate meaningfully into operating strength, it suggests structural advantages rather than temporary tailwinds. Investors typically reward such discipline, particularly in the ad-tech ecosystem, where margins are often pressured by competition and platform dependencies.

Arm Holdings has evolved far beyond its roots as a traditional chip designer. Today, it sits at the heart of energy-efficient AI computing, enabling intelligence to scale seamlessly from edge devices to cloud data centers. Its RISC-based architecture delivers superior performance per watt, a critical advantage as AI adoption accelerates under tight power constraints. ARM’s Neoverse V-Series CPUs are increasingly shaping modern AI infrastructure by supporting faster inference and more efficient machine-learning workloads without the excessive energy costs associated with legacy architectures.

A key differentiator is architectural consistency. A unified instruction set across mobile, cloud and edge environments allows developers to deploy AI applications with minimal friction, creating long-term strategic leverage. Partnerships, such as the one with Meta, underscore ARM’s growing relevance in data-center efficiency, while the addition of seasoned leadership from Amazon reflects a deeper push into advanced chipset innovation. Looking ahead, the planned AI chip division signals a shift toward becoming a strategic infrastructure provider rather than just a licensor, potentially strengthening Arm Holdings’ influence over AI performance economics and reinforcing its competitive moat.

Revenues crossing the billion-dollar mark again in the fourth quarter of 2025 are more than symbolic; it reinforces that Arm Holdings has reached a scale where growth is no longer purely cyclical or experimental. This expansion was driven by continued demand from advertisers and developers seeking better monetization outcomes, supported by ARM’s increasingly efficient ad delivery platform. What stands out is that this growth came off a much larger base compared to prior years, underscoring that Arm Holdings is sustaining momentum rather than decelerating as it scales.

While revenue growth remained robust, earnings growth reflected careful cost management and improved monetization efficiency. Arm Holdings continues to demonstrate that it can expand its platform without allowing expenses to erode profitability, an increasingly important signal for investors focused on quality growth.

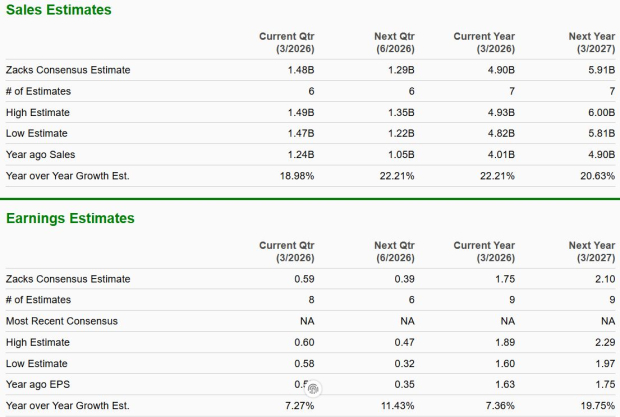

According to the Zacks Consensus Estimate, APP is poised to deliver a robust 38% year-over-year increase in sales, along with an impressive 55% surge in earnings per share for the current fiscal year, highlighting strong operations and accelerating profitability from its AI-driven advertising platform.

In contrast, ARM is expected to report a more modest 22% sales growth and a relatively muted 7% increase in EPS, suggesting a steadier growth trajectory as it continues to scale its licensing model and invest in AI-enabled chip innovation. While both companies are benefiting from secular tech tailwinds, APP's significantly higher earnings momentum may reflect greater short-term operational efficiency and demand capture in the evolving digital advertising landscape.

Arm Holdings trades at a forward 12-month P/E of 62X, well below its median of 144.44X, signaling a relative valuation discount. However, it still carries a steep premium, reflecting lofty expectations tied to its AI and IoT potential. In contrast, AppLovin’s forward P/E of 24X is below its median of 39X, suggesting a more grounded valuation. Given APP’s stronger earnings growth outlook and operational momentum, its current valuation appears more attractive. Investors may find better near-term upside in APP, especially as its AI-driven ad tech model continues to convert growth into profitability more effectively.

In weighing both opportunities, AppLovin appears to offer the more compelling near-term profile. Its AI capabilities are deeply embedded within its operating model, translating innovation directly into scalable execution and improving profitability. The company’s platform-driven ecosystem, data advantages and operational discipline position it to sustain momentum while navigating competitive pressures effectively. While ARM remains strategically important in the broader AI infrastructure landscape, its growth trajectory appears steadier and more valuation-sensitive at this stage. Considering current fundamentals and ranking signals, APP stands out as the more balanced and actionable choice for investors seeking AI exposure right now.

APP currently carries a Zacks Rank #3 (Hold), while ARM has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 13 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

AppLovin Stock Plunges To 52-Week Low After Earnings. Here's What Wall Street Is Saying.

APP -19.66%

Investor's Business Daily

|

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite