|

|

|

|

|||||

|

|

|

Urban Outfitters, Inc. URBN reported impressive results in fourth-quarter fiscal 2026, wherein the top and bottom lines beat the Zacks Consensus Estimate. Also, both metrics improved from the prior-year quarter’s reported figure.

In the fiscal fourth quarter, the company generated broad-based momentum across its brand portfolio, driven by strong customer engagement and improved product execution. Management highlighted balanced strength across digital and store channels, with healthy traffic trends and solid regular-price selling supporting overall performance. The company continued to benefit from disciplined inventory management, lower promotional intensity and operational efficiencies in logistics and fulfillment.

Management emphasized that operational focus, creative execution and tariff-mitigation efforts supported the company’s performance during the holiday season, positioning URBN with solid momentum entering fiscal 2027.

Urban Outfitters, Inc. price-consensus-eps-surprise-chart | Urban Outfitters, Inc. Quote

This lifestyle specialty retailer delivered earnings per share of $1.43, surpassing the Zacks Consensus Estimate of $1.24. Also, the bottom line increased 37.5% from the prior-year quarter.

Total net sales increased 10.1% year over year to $1,801.8 million, surpassing the consensus estimate of $1,787 million.

Total net sales in the Retail segment rose 7.7% year over year, with comparable net sales in this segment increasing 5.5%. The rise in comparable Retail sales was driven by mid-single-digit increases across both digital channel and brick-and-mortar store sales. Within the segment, comparable Retail segment net sales grew 9.6% at Urban Outfitters, 3.7% at Anthropologie and 5.2% at Free People. We estimated the Retail segment’s sales to increase 7.3% year over year.

In the Wholesale segment, net sales rose 9.1%, driven by a 10.2% increase in Free People Wholesale revenues, largely attributable to higher sales to specialty customers.

Nuuly, a women’s apparel subscription rental service, saw a significant 42.6% increase in net sales, primarily reflecting a 40.3% rally in average active subscribers compared with the same quarter last year. We estimated the Nuuly segment’s sales to rise 38.4% year over year.

Gross profit rose 13.6% from the prior-year quarter to $599.2 million. Also, the gross margin expanded 101 basis points (bps) to 33.3%, which beat our estimate of 32.6%. The gross margin improvement was driven by improved Retail segment markdowns, reflecting reduced markdown activity at Urban Outfitters and Free People. The improvement also benefited from leverage in store occupancy costs resulting from higher comparable Retail segment net sales, as well as leverage in delivery expenses due to fewer packages shipped per order. These gains were partially offset by deleverage in initial merchandise costs.

The rise in gross profit was driven by increased net sales and margin expansion. During the year, the company recorded $2 million in store impairment charges.

The Retail segment’s gross profit rose 12% year over year to $540.3 million, with the segmental gross margin expanding 136 basis points to 34.5%. Wholesale segment gross profit increased 6% to $20.4 million, though its gross margin contracted 75 basis points to 27.3%. Subscription segment gross profit grew 46% to $38.5 million, with the gross margin improving 51 basis points to 24%.

Selling, general and administrative (SG&A) expenses rose 9.5% year over year to $440.5 million. This increase was mainly due to higher marketing investments to support customer growth, and increased sales in the Retail and Subscription segments, along with higher store payroll expenses to support net sales growth in the Retail segment stores. Our model estimated SG&A expenses to increase 9.3% year over year in the fiscal fourth quarter.

As a percentage of net sales, SG&A leveraged 14 bps to 24.5% in the quarter under review, which lagged our estimate of 24.6%. This increase was primarily driven by leverage in store payroll costs resulting from net sales growth at Retail segment stores.

URBN recorded an operating income of $158.7 million, up 26.6% from $125.3 million in the prior-year quarter. As a rate of sales, the operating margin increased 115 basis points year over year at 8.8%, primarily driven by gross margin improvement.

In the fiscal fourth quarter, this Zacks Rank #4 (Sell) company opened 42 retail locations, which included five Urban Outfitters stores, nine Anthropologie stores and 28 Free People stores (including 17 FP Movement stores). Also, it closed one Anthropologie store, three Free People stores and 8 Urban Outfitters stores.

As of Jan. 31, 2026, URBN operated 253 Urban Outfitters stores across the United States, Canada and Europe, along with associated websites. The company also operated 254 Anthropologie Group stores in these regions, supported by catalogs and websites. Additionally, there were 268 Free People stores, including 88 FP Movement stores, in the United States, Canada and Europe, accompanied by catalogs and websites. URBN further operated nine Menus & Venues restaurants, seven Urban Outfitters franchisee-owned stores, and two Anthropologie Group franchisee-owned stores.

In fiscal 2027, the company plans to open 57 stores and close 14 stores. Net new store growth is primarily driven by the expansion in FP Movement, Free People and Anthropologie locations. Specifically, the company expects to open 21 FP Movement stores, 13 Free People stores, 14 Anthropologie stores and 8 Urban Outfitters stores during fiscal 2027.

As of Jan. 31, 2026, URBN had cash and cash equivalents of $369.2 million, and total shareholders’ equity of $2.82 billion. Including marketable securities, total liquidity exceeded $1.1 billion, with no borrowings under its $350 million asset-backed credit facility.

Total inventory increased 12.8% year over year to $700.9 million. Retail segment inventory increased 13.4%, while comparable Retail segment inventory rose 5.3%. Wholesale segment inventory increased 8.5%. Inventory growth was primarily aligned with higher sales and the timing of receipts.

For fiscal 2026, the company generated $575.2 million in cash from operating activities, and capital expenditure totaled $260.2 million. The company repurchased and retired 3.3 million shares for approximately $154 million in fiscal 2026. As of Jan. 31, 2026, 14.6 million common shares remained authorized for repurchase under the program.

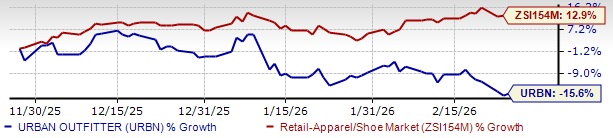

URBN Stock Past 3-Month Performance

For the first quarter of fiscal 2027, Urban Outfitters expects to deliver positive high-single-digit total company sales growth. This outlook is supported by anticipated mid-single-digit comparable sales growth in the Retail segment.

Brand-wise, within Retail, comparable sales are projected to rise in the high-single digit at Urban Outfitters, mid-single digit at Free People and low-single digit at Anthropologie. The Subscription segment, led by Nuuly, is expected to deliver mid-double-digit revenue growth in the quarter. The Wholesale segment is projected to post mid-teen revenue growth in the fiscal first quarter.

On the margin front, fiscal first-quarter gross profit margin is expected to decline 25-50 basis points year over year. This outlook excludes a non-recurring gain recorded in the first quarter of fiscal 2026, which positively impacted last year’s gross margin by approximately $5 million, or 36 basis points. The anticipated year-over-year decline is primarily due to lower IMU, driven by higher tariff costs.

Selling, general and administrative expenses are expected to grow several percentage points faster than sales in the fiscal first quarter. The increase is primarily related to the timing of marketing investments at Nuuly and Anthropologie, along with increased technology investments. Management noted that the gap between SG&A growth and sales growth will likely be more pronounced in the first half of the year compared with the second half.

For fiscal 2027, Urban Outfitters expects high-single-digit total company sales growth. This outlook is driven by projected mid-single-digit comparable sales growth in the Retail segment, mid-double-digit revenue growth in the Subscription segment and mid-single-digit revenue growth in the Wholesale segment.

The gross margin for fiscal 2027 is expected to expand 25 basis points from the prior year, with the second half reflecting a benefit to IMU. This outlook reflects the tariffs in place prior to the Supreme Court ruling overturning the IEEPA tariffs this past Friday.

SG&A expenses are expected to grow faster than sales for the full year. The increase in SG&A dollars is primarily related to strategic technology investments to support Nuuly’s continued expansion and to accelerate the internal product lifecycle through the implementation of Agentic AI tools. These investments are expected to drive long-term benefits, including improved speed to market, enhanced decision-making closer to customer demand, higher sales and lower markdowns.

Inventory is expected to increase at the same rate as sales or slower in fiscal 2027. Capital expenditure for fiscal 2027 is planned at $385 million. Approximately 40% of spending will be allocated toward retail store expansion and support, 40% toward logistics investments to expand capacity and automation in both the Subscription and Retail segments, and the remaining 20% will be spent on technology investments and home office expansion.

Shares of this company have lost 15.6% in the past three months against the industry’s 12.9% growth.

We have highlighted three better-ranked stocks, namely, Deckers Outdoor Corporation DECK, American Eagle Outfitters Inc. AEO and Boot Barn Holdings, Inc. BOOT.

Deckers is a leading designer, producer and brand manager of innovative, niche footwear and accessories. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Deckers’ current fiscal-year earnings and sales indicates growth of 8.5% and 8.9%, respectively, from the year-ago actuals. DECK delivered a trailing four-quarter average earnings surprise of 36.9%.

American Eagle is a specialty retailer of casual apparel, accessories and footwear. It currently sports a Zacks Rank of 1.

The Zacks Consensus Estimate for AEO’s current fiscal-year earnings and sales implies a decline of 20.7% and growth of 2.6%, respectively, from the year-ago actuals. American Eagle delivered a trailing four-quarter average earnings surprise of 35.1%.

Boot Barn operates as a lifestyle retail chain devoted to western and work-related footwear, apparel and accessories. It currently has a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Boot Barn’s fiscal 2026 earnings and sales implies growth of 26% and 17.6%, respectively, from the year-ago actuals. BOOT delivered a trailing four-quarter average earnings surprise of 4.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite