|

|

|

|

|||||

|

|

|

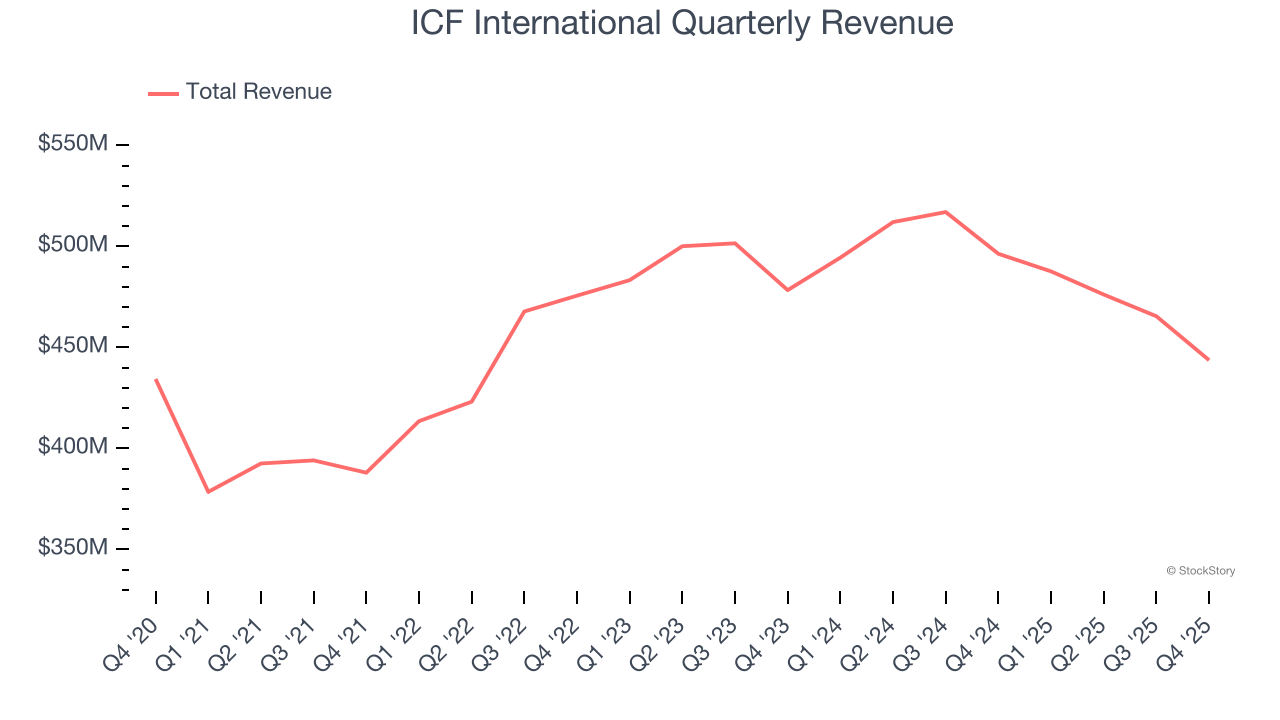

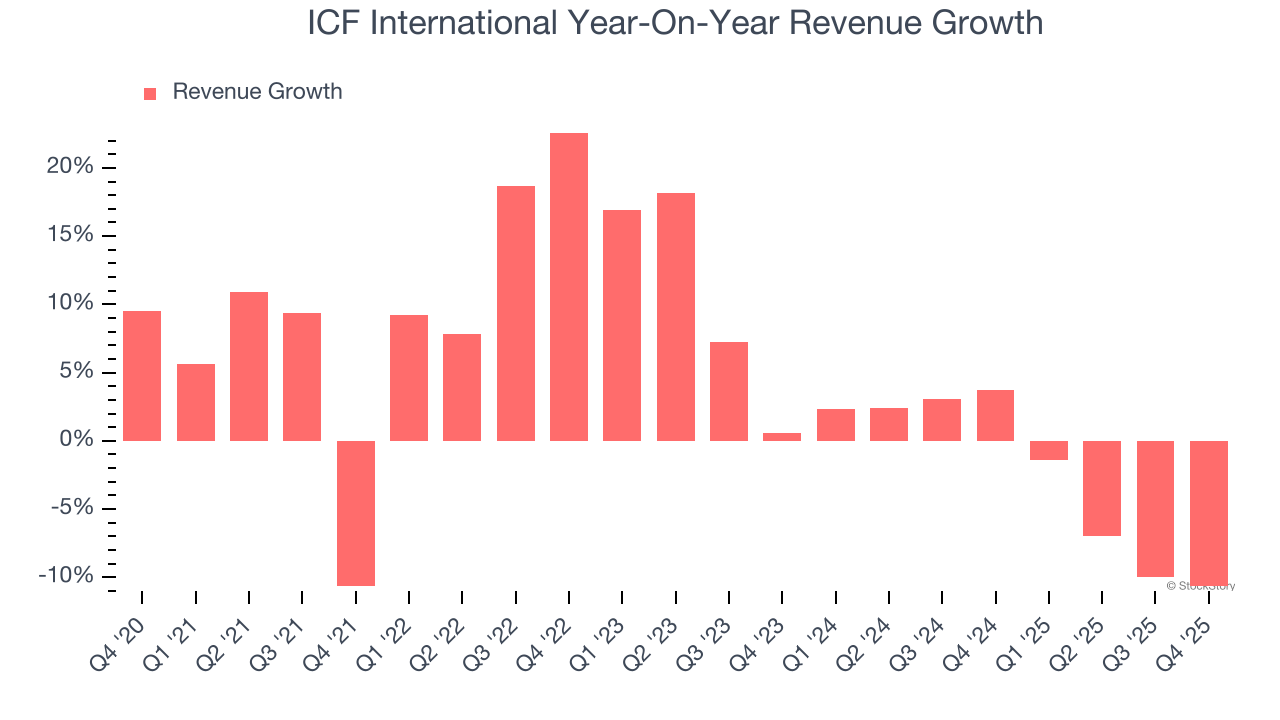

Professional consulting firm ICF International (NASDAQ:ICFI) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 10.6% year on year to $443.7 million. The company expects the full year’s revenue to be around $1.93 billion, close to analysts’ estimates. Its non-GAAP profit of $1.47 per share was 1.5% below analysts’ consensus estimates.

Is now the time to buy ICF International? Find out by accessing our full research report, it’s free.

Commenting on the results, John Wasson, chair and chief executive officer, said, "Our fourth quarter results were in line with our guidance and capped a year of resilient performance given the challenging federal business environment. Revenues from commercial, state and local and international government clients increased 16% and accounted for 62% of fourth quarter revenues. This performance served to offset a large portion of the year-on-year reduction in federal government revenues, which was amplified by the direct and indirect impacts of the six-week federal government shutdown.

Operating at the intersection of policy, technology, and implementation for over five decades, ICF International (NASDAQ:ICFI) provides professional consulting services and technology solutions to government agencies and commercial clients across energy, health, environment, and security sectors.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.87 billion in revenue over the past 12 months, ICF International is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, ICF International’s 4.4% annualized revenue growth over the last five years was mediocre. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. ICF International’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.3% annually.

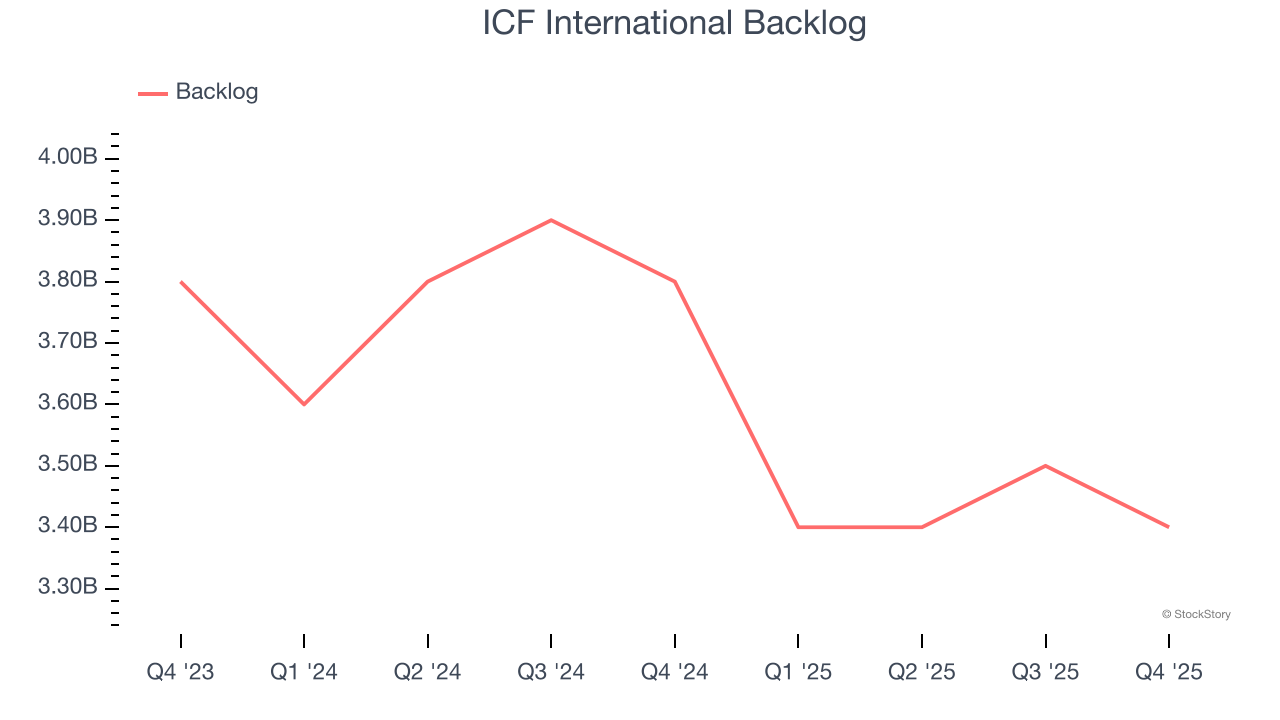

ICF International also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. ICF International’s backlog reached $3.4 billion in the latest quarter and averaged 7.4% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, ICF International’s revenue fell by 10.6% year on year to $443.7 million but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

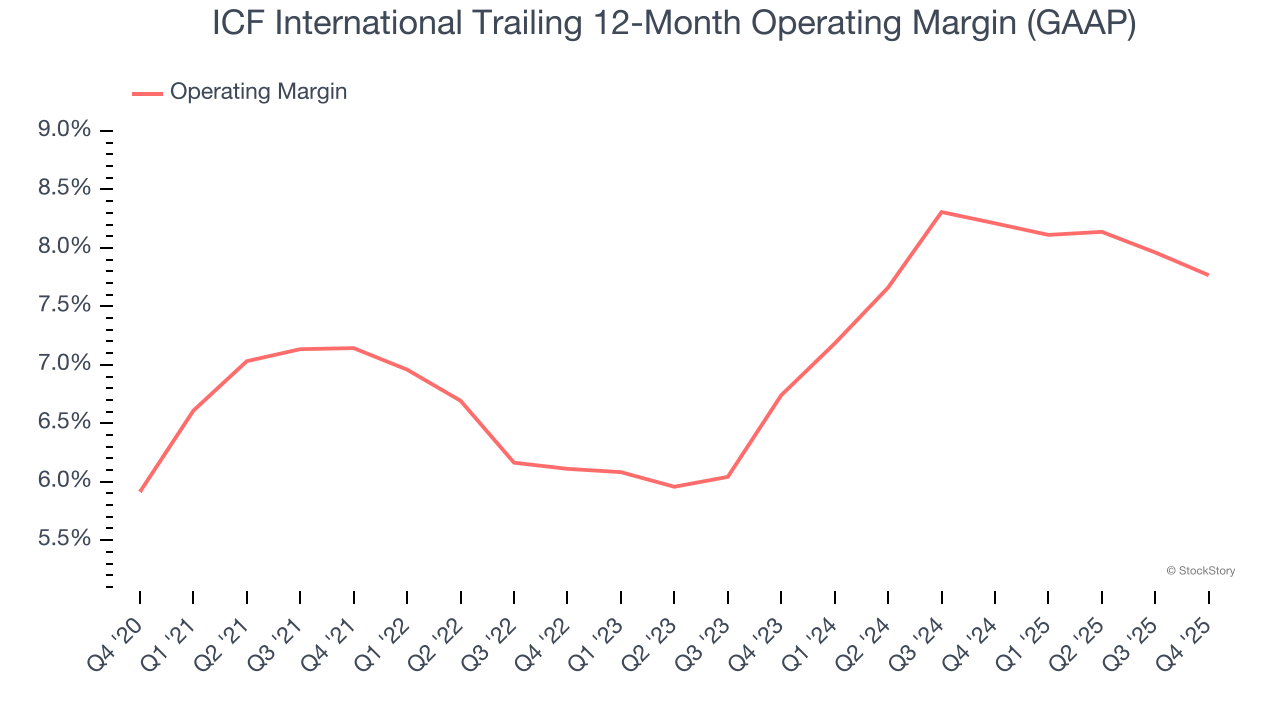

ICF International’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 7.2% over the last five years. This profitability was paltry for a business services business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, ICF International’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, ICF International generated an operating margin profit margin of 6.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

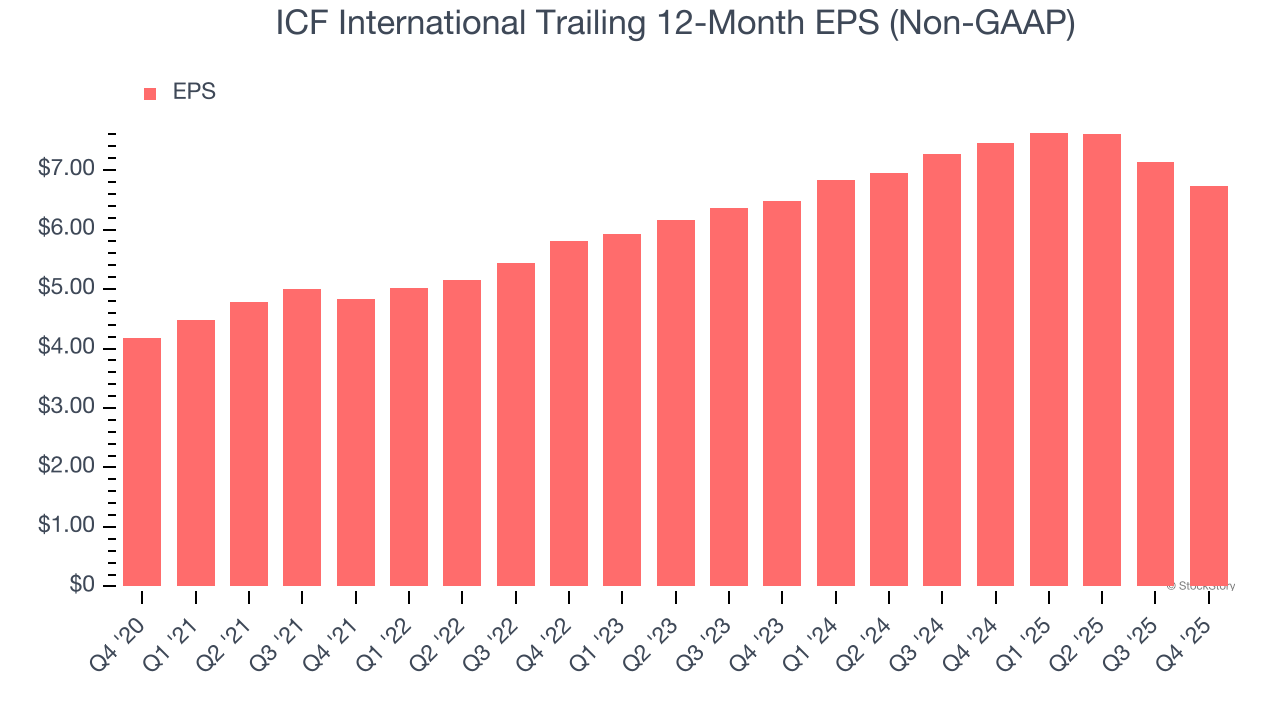

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ICF International’s EPS grew at a solid 10% compounded annual growth rate over the last five years, higher than its 4.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ICF International, its two-year annual EPS growth of 2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, ICF International reported adjusted EPS of $1.47, down from $1.87 in the same quarter last year. This print slightly missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects ICF International’s full-year EPS of $6.74 to grow 5.6%.

It was good to see ICF International narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS slightly missed. Overall, this was a softer quarter. The stock remained flat at $79.58 immediately after reporting.

Is ICF International an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-21 | |

| Jun-30 | |

| Jun-25 | |

| Jun-24 | |

| May-20 | |

| May-07 | |

| May-07 | |

| May-07 | |

| Apr-08 | |

| Mar-26 | |

| Mar-05 | |

| Mar-05 | |

| Mar-01 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite