|

|

|

|

|||||

|

|

|

Over the past six months, Qorvo’s shares (currently trading at $82.50) have posted a disappointing 10.2% loss, well below the S&P 500’s 7.2% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Qorvo, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Despite the more favorable entry price, we're cautious about Qorvo. Here are three reasons we avoid QRVO and a stock we'd rather own.

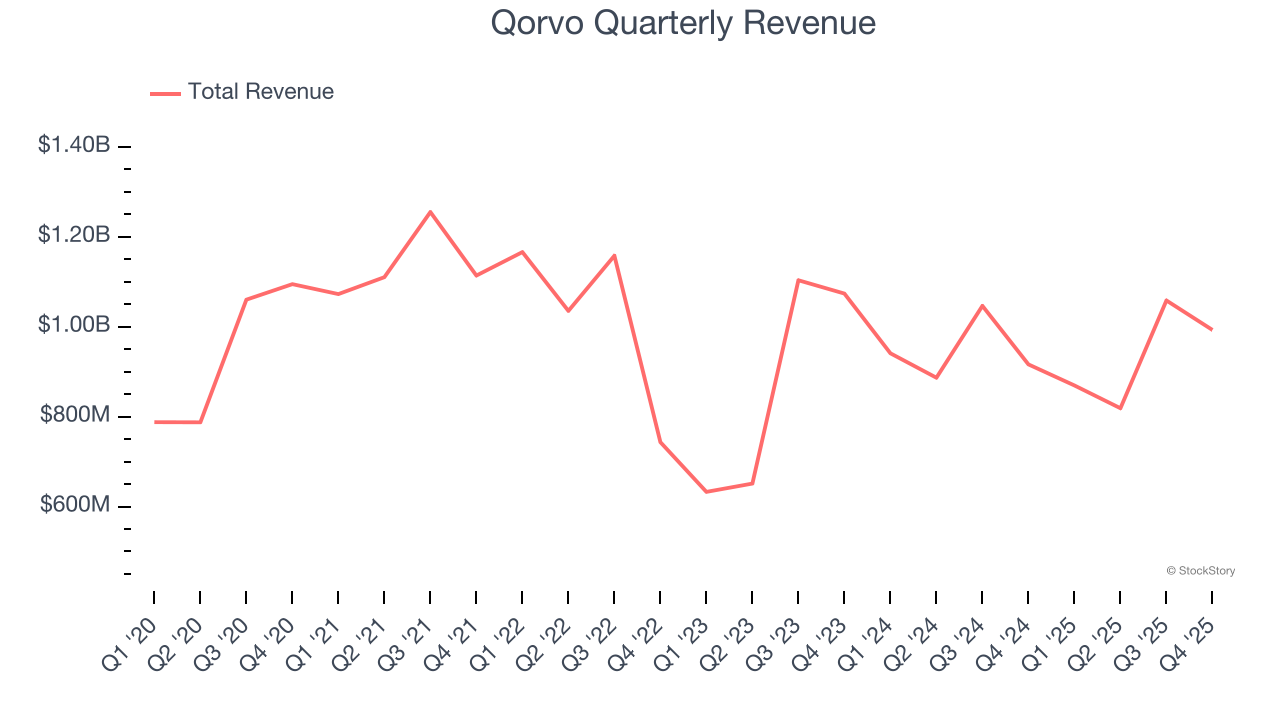

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Qorvo struggled to consistently increase demand as its $3.74 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Qorvo’s revenue to drop by 10%, a decrease from its flat result for the past five years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

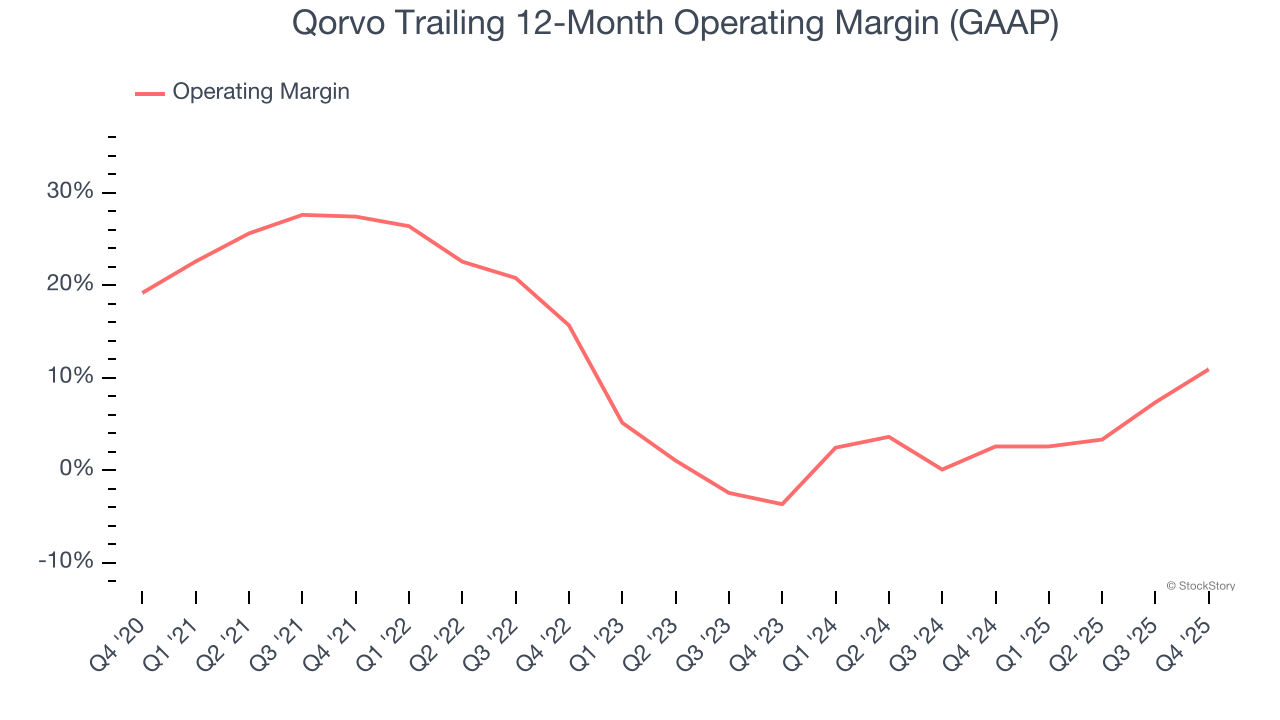

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Looking at the trend in its profitability, Qorvo’s operating margin decreased by 16.5 percentage points over the last five years. Qorvo’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was 10.9%.

Qorvo falls short of our quality standards. After the recent drawdown, the stock trades at 13.5× forward P/E (or $82.50 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. Let us point you toward our favorite semiconductor picks and shovels play.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-07 | |

| Jul-07 | |

| Jun-05 | |

| May-06 | |

| May-05 | |

| May-05 | |

| May-04 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-20 | |

| Apr-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite