|

|

|

|

|||||

|

|

|

Altria Group, Inc. MO and Philip Morris International Inc. PM are two of the most prominent names in the global tobacco industry, a sector driven by cigarette and nicotine product sales amid shifting consumer preferences. Altria, with a market capitalization of approximately $116.6 billion, is anchored by its iconic Marlboro franchise and a strong U.S.-focused portfolio that also includes smokeless and reduced-risk offerings. Its strategy balances legacy combustible products with expanding smoke-free categories such as nicotine pouches and e-vapor devices.

In comparison, Philip Morris commands a larger market value of around $291.9 billion, reflecting its broad international footprint and leadership in next-generation products. PM’s growth is supported by premium combustible brands abroad alongside an expanding reduced-risk portfolio, IQOS heated tobacco, ZYN oral nicotine and VEEV e-vapor, which positions it at the forefront of the industry’s shift toward smoke-free alternatives. Both companies are investing heavily in innovation to offset declining cigarette volumes, but which has the edge in growth, resilience and risk management?

Altria’s investment appeal remains anchored in its resilient cash-flow generation and consistent shareholder returns, underpinned by the enduring strength of the U.S. tobacco franchise. In 2025, the company delivered steady adjusted earnings per share (EPS) growth of 4.4% while returning roughly $8 billion to its shareholders through dividends and share repurchases. The company’s pricing power, disciplined cost management and structured capital allocation continue to reinforce its standing as a dependable income-oriented name within the consumer staples sector.

Despite persistent secular cigarette volume declines, Altria continues to demonstrate strong pricing execution and operational discipline. The smokeable products segment generated more than $11 billion in adjusted operating income in 2025, with margins expanding to 63.4%, supported by robust net price realization. The ability to offset volume pressure through pricing actions and productivity initiatives remains central to earnings stability and long-term dividend sustainability.

Altria is advancing its smoke-free portfolio, particularly in modern oral nicotine. The on! brand posted shipment volume growth of 10.9% in 2025, and FDA authorization alongside the planned national rollout of on! PLUS enhances the company’s competitive positioning in the fast-growing nicotine pouch category. Management continues to emphasize regulatory progress, product innovation and measured investment in oral nicotine as part of its broader effort to diversify beyond combustibles.

Still, the transition is unfolding against meaningful structural and regulatory headwinds. Domestic cigarette volumes declined approximately 9.5% in 2025, highlighting ongoing secular pressure within the combustible category. Over the long term, the investment thesis increasingly hinges on whether growth in oral nicotine and other smoke-free products can scale sufficiently to offset combustible volume erosion and sustain earnings momentum.

Philip Morris reinforced its growth profile in 2025 with accelerating earnings, expanding margins and continued smoke-free momentum. The company delivered adjusted EPS of $7.54, representing 14.8% growth, while net revenues exceeded $40 billion for the year. Strong pricing, favorable product mix and operating leverage supported organic operating income growth of 10.6%, highlighting the scalability of its global platform.

Smoke-free products remain the central growth engine. In 2025, smoke-free shipment volumes increased 12.8%, driving 15% net revenue growth and 20.3% rise in gross profit. Smoke-free products accounted for 41.5% of total net revenues and nearly 43% of gross profit for 2025. IQOS heated tobacco units continued to gain traction with solid double-digit shipment growth, reinforcing the brand’s dominant position in the global heated tobacco category. Meanwhile, ZYN nicotine pouches continued to scale rapidly, enhancing the smoke-free portfolio’s growth mix and long-term earnings potential.

Although combustible cigarette shipments declined 1.5% for the year, pricing actions helped lift combustible net revenues by 2.5% and gross profit by 5.2%. This pricing resilience, combined with productivity initiatives and a favorable smoke-free mix, supported broader profitability gains, with total adjusted operating margins expanding to 40.4% for the company. The balance between combustible cash generation and rapid smoke-free scaling continues to underpin earnings durability during the transition.

Looking ahead, management projects 2026 adjusted EPS growth of 11.1% to 13.1%, or 7.5% to 9.5% excluding favorable currency impacts, indicating continued confidence in the company’s operating momentum. With smoke-free products projected to sustain strong shipment momentum, Philip Morris appears well positioned to maintain above-industry earnings growth while accelerating its transition toward a predominantly smoke-free portfolio.

The Zacks Consensus Estimate for Altria’s 2026 EPS has moved down a cent over the last 30 days to $5.57, implying a year-over-year increase of 2.8%.

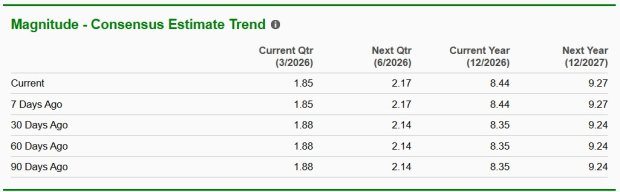

In comparison, the consensus estimate for Philip Morris has risen 9 cents to $8.44 during the same period, indicating 11.9% growth for 2026.

Over the past year, Altria’s shares have climbed 26.1%, outperforming Philip Morris, which gained 21.7% over the same period. However, both stocks trailed the industry, which advanced 33.8%. Currently, MO trades at $69.47, about 1.1% below its 52-week high. PM, at $187.50, sits roughly 2% below its peak.

Altria is trading at a forward 12-month price-to-earnings (P/E) ratio of 12.4, modestly above its one-year median of 10.93. In comparison, Philip Morris trades at a forward P/E of 21.82, also above its one-year median of 20.71.

Among the leading tobacco firms, Philip Morris stands out as the stronger growth story. Its accelerated shift toward smoke-free products, global scale and disciplined cost execution are driving sustained earnings and margin expansion. In contrast, Altria remains more reliant on its U.S. combustible franchise, where pricing power supports profitability, but growth is constrained by structural volume declines. For investors prioritizing long-term growth and industry transformation, PM appears better positioned, while Altria remains a compelling choice for stability and consistent income.

PM currently has a Zacks Rank #2 (Buy), while MO carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite