|

|

|

|

|||||

|

|

|

Meta Platforms META and Alphabet GOOGL are behemoths of the digital advertising market, generating billions of dollars in revenues. In 2025, Meta Platforms’ advertising revenues increased 22% from 2024 to $196.8 billion, driven by a 12% increase in ad impressions and a 9% increase in average ad price. Meanwhile, Alphabet reported Google Advertising revenues of $294.7 billion, up 11.4% year over year, driven by 13.4% growth in Search revenues and 11.7% growth in YouTube ad revenues.

Both companies are vociferously infusing AI across their platforms to keep users as well as advertisers engaged, thereby driving top-line growth. However, META or GOOGL, which has an edge now? Let’s find out.

Meta Platforms’ focus on integrating AI into its platforms — Facebook, WhatsApp, Instagram, Messenger and Threads — is driving user engagement to boost ad revenues. AI is heavily dependent on data, of which META has a trove, driven by its more than 3.58 billion daily users, including 2 billion daily actives each on Facebook and WhatsApp. Time spent across platforms is expected to benefit from Meta Platforms’ continuous ranking optimizations.

AI recommendations that deliver higher quality and more relevant content are expected to drive engagement. The company expects to advance the capabilities of META’s underlying media generation models and ship new features to further enhance the product experience in 2026. Focus on expanding personalization on Meta AI is expected to help the company understand user interests and preferences, as well as identify the most relevant content across the META platform.

Meta Platforms’ ad business is benefiting from an improved AI ranking system. The company has started testing Meta AI business assistant with advertisers, which helps with tasks like campaign optimization and account support. META has a strong pipeline of ad supply opportunities on both Threads and WhatsApp Status over the long term. Ads are now running globally in Feed on Threads, and META plans to optimize the ad formats and performance before increasing supply. The company has extended its Andromeda ads retrieval engine so it can now run on NVIDIA, AMD and MTIA.

Meta Platforms is spending heavily on AI research, models and infrastructure. The company now expects 2026 capital spending between $115 billion and $135 billion. However, aggressive spending with 2026 operating expenses expected between $162-$169 billion is expected to hurt earnings-generating ability and squeeze free cash flow in the near term. This, along with stiff competition in the ad market, is a headwind for META.

Alphabet continues to dominate the Search business, driven by its AI endeavors that have been helping it to enhance user experience, provide better AI-focused features and consequently improve ad performance. Upgradation of AI Overviews to Gemini 3 is offering users a best-in-class AI response at the top of the search results page. GOOGL has made the transition from an AI overview to a conversation in AI Mode completely seamless. This is driving up user experience as well as engagement.

In the United States, Alphabet saw daily AI Mode queries per user double since launch, and AI Overviews continue to perform very well. Queries in AI Mode are three times longer than traditional searches. The company is also seeing sessions becoming more conversational, with a significant portion of queries in AI Mode now leading to a follow-up question.

Alphabet is investing in AI to drive significant improvements across all areas of marketing. The addition of Gemini models is improving query understanding, thereby driving better query matching, ranking and quality. These improvements are making search ads more effective. GOOGL is building more agentic actions into its advertiser tools, and businesses can now leverage Gemini in conversational experiences within Ads and Analytics Advisor, thereby generating new campaigns much faster and in a smoother way. Introduction of Direct Offers, a new Google Ads pilot, helps advertisers show exclusive offers for shoppers who are ready to buy directly in AI Mode.

AI initiatives get a further boost with GOOGL’s huge investment plan, $175-$185 billion, for 2026. Most of this spending is marked for building AI and cloud infrastructure, including data centers, chips and servers for Gemini and cloud growth. Alphabet is riding on a strong Google Cloud prospect, which accounted for 14.6% of GOOGL’s 2025 revenues. Google Cloud revenues jumped 35.8% over 2025’s reported figure to $58.71 billion. The top line benefited from growth in Google Cloud Platform across core products, AI Infrastructure and generative AI Solutions. Cloud backlog jumped 55% sequentially to $240 billion at the end of 2025. The AI push is expected to boost Google Cloud’s prospects in the near term.

The Zacks Consensus Estimate for META’s 2026 earnings is pegged at $29.24 per share, up by 7 cents over the past 30 days, indicating a 5.83% increase over fiscal 2024’s reported figure.

Meta Platforms, Inc. price-consensus-chart | Meta Platforms, Inc. Quote

The consensus mark for Alphabet’s 2026 earnings increased 4.6% to $11.60 per share over the past 30 days, suggesting 7.3% growth over 2025.

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

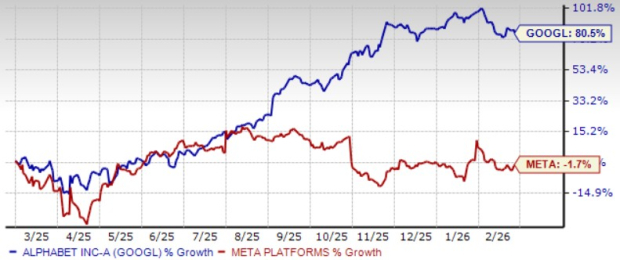

Meta Platforms’ shares have underperformed Alphabet in a year. While META shares have dropped 1.7%, Alphabet has appreciated 80.5%.

Both Meta Platforms and Alphabet are overvalued, as suggested by the Value Score of C and D, respectively.

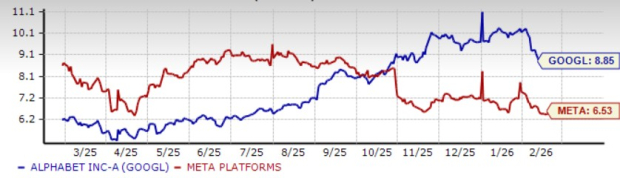

In terms of forward 12-month Price/Sales, Meta Platforms shares are trading at 6.53X, lower than Alphabet’s 8.85X.

Both Alphabet and Meta Platforms are well-poised to benefit from higher digital spending and the infusion of AI across their respective platforms. However, Alphabet’s diversification in terms of revenue generation (Google Cloud, subscriptions) beyond advertising gives GOOGL an edge over Meta Platforms, which generates roughly 98% of revenues from advertising.

Alphabet and Meta Platforms currently carry a Zacks Rank #3 (Hold) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 14 hours | |

| 14 hours |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

META

Investor's Business Daily

|

| 14 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

META GOOGL

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite