|

|

|

|

|||||

|

|

|

MP Materials MP and USA Rare Earth, Inc. USAR are U.S.-based companies in the rare-earth metals and magnets space. Rare earths are crucial to the production of high-performance magnets used in EVs, defense and high-tech applications. With China dominating the global supply so far, the United States is accelerating efforts to build domestic rare earth capabilities. Both companies are expected to play key roles in driving this strategic shift.

Las Vegas, NV-based MP Materials, with a market capitalization of $10.6 billion, is currently the only fully integrated rare earth producer in the United States. It has capabilities covering the entire supply chain, from mining and processing to advanced metallization and magnet manufacturing. Stillwater, OK-based USA Rare Earth, valued at around $4.4 billion, is currently building a sintered neo magnet manufacturing facility, expected to start commercial production in the first quarter of 2026.

For investors seeking long-term exposure to the rare earth theme, the key question is which stock offers a stronger opportunity, MP or USAR. Below is a breakdown of their fundamentals, growth catalysts and key headwinds.

The company owns and operates the Mountain Pass Rare Earth Mine and Processing Facility, the only large-scale rare earth mining and processing site in North America.

2025 was a pivotal year for MP Materials, highlighted by a long-term agreement to supply U.S.-made recycled rare earth magnets to Apple and a public-private partnership with the U.S. Department of War to accelerate a fully integrated domestic magnet supply chain. Backed by government incentives, the company will construct the second domestic magnet manufacturing facility (the 10X Facility) in Northlake, TX, which will lift U.S. magnet capacity to 10,000 metric tons and serve defense and commercial markets. MP also expects to extend the lifespan of Mountain Pass through further exploration and enhanced processing.

The company was awarded a $200 million incentive package, anchored by the Texas Semiconductor Innovation Fund (“TSIF”) grant, for the new facility.

MP Materials has doubled its NdPr (Neodymium-Praseodymium) oxide production at Mountain Pass to a record 2,599 MTs in 2025. The company also produced a record 50,692 MTs of REO in concentrate, a 12% increase year over year. It also produced its first magnets on commercial-scale equipment at the Independence facility.

The company also signed a significant long-term NdPr offtake agreement with a new customer, one of America's leading technology and industrial companies. It has direct strategic agreements with four of the world's leading manufacturers across automotive, consumer electronics and physical AI.

MP Material’s revenues increased 10% year over year to $224.4 million in 2025 on higher NdPr oxide and metal revenues as well as revenues from the sales of magnetic precursor products, with no comparable revenues in the prior year. The increase was partially offset by lower rare earth concentrate revenues, reflecting the company’s decision to cease sales to China starting in July 2025.

Adjusted earnings per share in 2025 were a loss of 24 cents, an improvement from the loss of 44 cents in 2024. This was driven by the NdPr price floor protection agreement with the DoW (the “Price Protection Agreement” or “PPA”) for NdPr products, which commenced on Oct. 1, 2025, as well as the commencement of magnetic precursor product sales. This was somewhat offset by higher legal costs, as well as increased advanced projects and development expenses, which included transaction costs associated with the DoW agreements and securing financing.

The company ended 2025 with $1.83 billion in cash and a lower debt-to-capital ratio of 0.33, and expects $500–$600 million in capex in 2026 to fund expansion, recycling and heavy rare earth separation initiatives. In 2026, the company expects to break ground on a 10X magnetics facility in Northlake, ramp magnet production for General Motors and deliver continued growth in NdPr output.

USA Rare Earth is building a fully integrated rare earth and permanent magnet supply chain across the United States, the United Kingdom and Europe. In a major strategic move, the company acquired LCM, a UK-based manufacturer of specialized rare earth metals and both cast and strip cast alloys. LCM is the only proven ex-China producer of both light and heavy rare earth permanent magnet metals and alloys at scale. Combined with the development of magnet manufacturing capacity in Stillwater, OK, USAR operates across the entire value chain from heavy rare earth processing to metal-making, alloy production and neodymium magnet manufacturing.

The Stillwater magnet facility is on track to complete commissioning in the first quarter of 2026. Recently, LCM established a strategic partnership with Solvay, a multinational chemical company, to supply rare earth metals to Permag, a leader in high-precision magnets and magnetic assemblies. This partnership will ensure a secure supply of Samarium for the European market and Permag's global customer base. LCM signed a supply agreement with Solvay and Arnold Magnetic Technologies Corp., a subsidiary of Compass Diversified, for the production of advanced permanent magnets.

Per the company’s preliminary results, USA Rare Earth had cash and cash equivalents of more than of $350 million as of Dec. 31, 2025. The company anticipates both operating expenses and operating loss in the range of $56-$62 million, and capital expenditures in the range of $37-$43 million for 2025.

In January, USA Rare Earth entered into a non-binding Letter of Intent (the LOI) with the U.S. Department of Commerce and announced collaboration with the U.S. Department of Energy (DOE). The Department of Commerce’s CHIPS Program has provided an LOI entailing $277 million in proposed federal funding and a $1.3 billion senior secured loan under the CHIPS Act, a total of $1.6 billion.

USAR recently raised $1.5 billion in private sector investment and intends to use the proceeds to accelerate the build-out of its mine-to-magnet value chain as well as for working capital and general corporate purposes.

The LOI remains subject to due diligence and final approvals. It underscores the strategic importance of USAR’s integrated platform in closing the domestic rare earth supply gap. This capital is expected to accelerate and de-risk USAR’s growth objectives. The company plans to extract 40,000 metric tons per day of feedstock from its Round Top deposit beginning in 2028. It plans to process a combined 8,000 metric tons per annum of third-party Mixed Rare Earth Carbonate (MREC) and heavy rare earth elements (HREEs) and critical mineral oxides and concentrates at Round Top. Leveraging LCM’s expertise, USAR intends to reshore 10,000 tons per annum of heavy rare earth element metal- and alloy-making and strip-casting capacity, capabilities that do not currently exist in the United States. USAR also wants to take NdFeB magnet-making capacity to 10,000 tons per annum by June 2029, more than double its previous plans. Backed by these, management forecasts annual revenues approaching $2.6 billion and EBITDA of $1.2 billion by 2030.

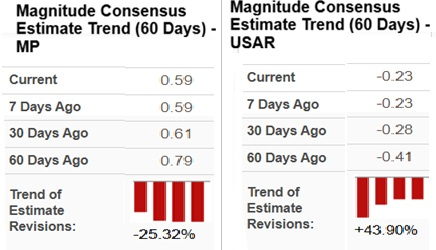

The Zacks Consensus Estimate for MP Materials’ fiscal 2026 earnings is pegged at 59 cents per share, indicating a turnaround from the loss of 24 cents reported in fiscal 2025.

The consensus estimate for USA Rare Earth’s fiscal 2026 earnings is at a loss of 23 cents per share, suggesting a narrower loss than the expected loss of 76 cents for fiscal 2025.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for earnings for MP Materials for 2026 has moved down over the past 90 days. The earnings estimates for 2026 for USAR have seen upward estimate revisions over the past 60 days.

In a year, MP Materials stock has soared 149.9% compared with USA Rare Earth’s 80.9% rise.

Both MP and USAR currently carry a Zacks Rank #3 (Hold), reflecting balanced risk-reward profiles and strong long-term positioning in a strategically vital sector. Each stands to benefit from accelerating U.S. efforts to localize rare earth mining and magnet production.

That said, MP appears to have the near-term edge. It is already generating revenues from scaled operations, has an established asset in Mountain Pass secured high-profile commercial and government partnerships, and maintains a strong balance sheet to fund expansion. Importantly, it has a clearer path to profitability in 2026 as magnet production ramps and downstream integration deepens.

USAR’s vertically integrated mine-to-magnet vision is ambitious and well-funded, especially following its PIPE raise and proposed CHIPS-related support. However, much of its value proposition depends on projects that are still under development, including Round Top and the full ramp-up of magnet capacity. Execution risk and ongoing losses remain key overhangs.

Overall, MP stock appears to be the better choice.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 7 hours | |

| 8 hours | |

| Jul-16 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 |

Democratic Lawmakers Probe Lutnick's Possible Ties to Cantor Fitzgerald Deal

USAR -8.11%

The Wall Street Journal

|

| Jul-06 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite