|

|

|

|

|||||

|

|

|

Skyworks Solutions has gotten torched over the last six months - since September 2025, its stock price has dropped 20.3% to $58.60 per share. This might have investors contemplating their next move.

Is now the time to buy Skyworks Solutions, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Despite the more favorable entry price, we don't have much confidence in Skyworks Solutions. Here are three reasons why SWKS doesn't excite us and a stock we'd rather own.

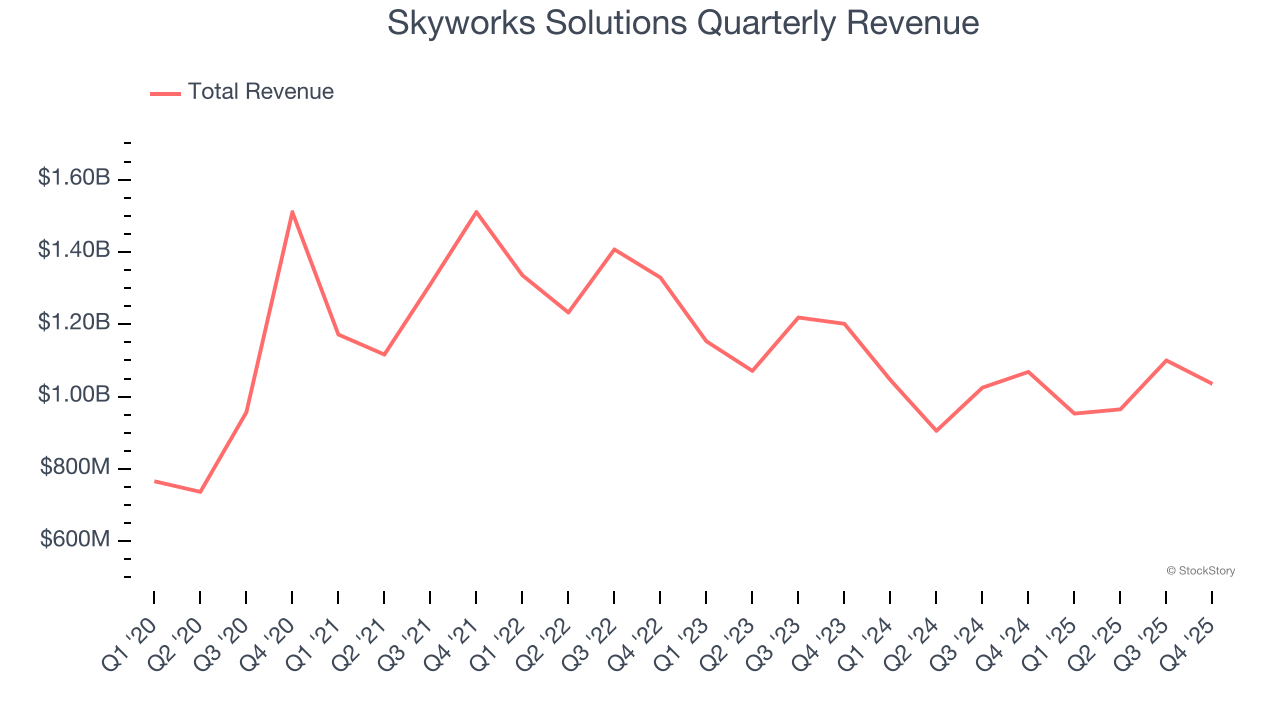

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Skyworks Solutions struggled to consistently increase demand as its $4.05 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Skyworks Solutions’s revenue to drop by 8.1%, a decrease from its flat result for the past five years. This projection is underwhelming and suggests its products and services will face some demand challenges.

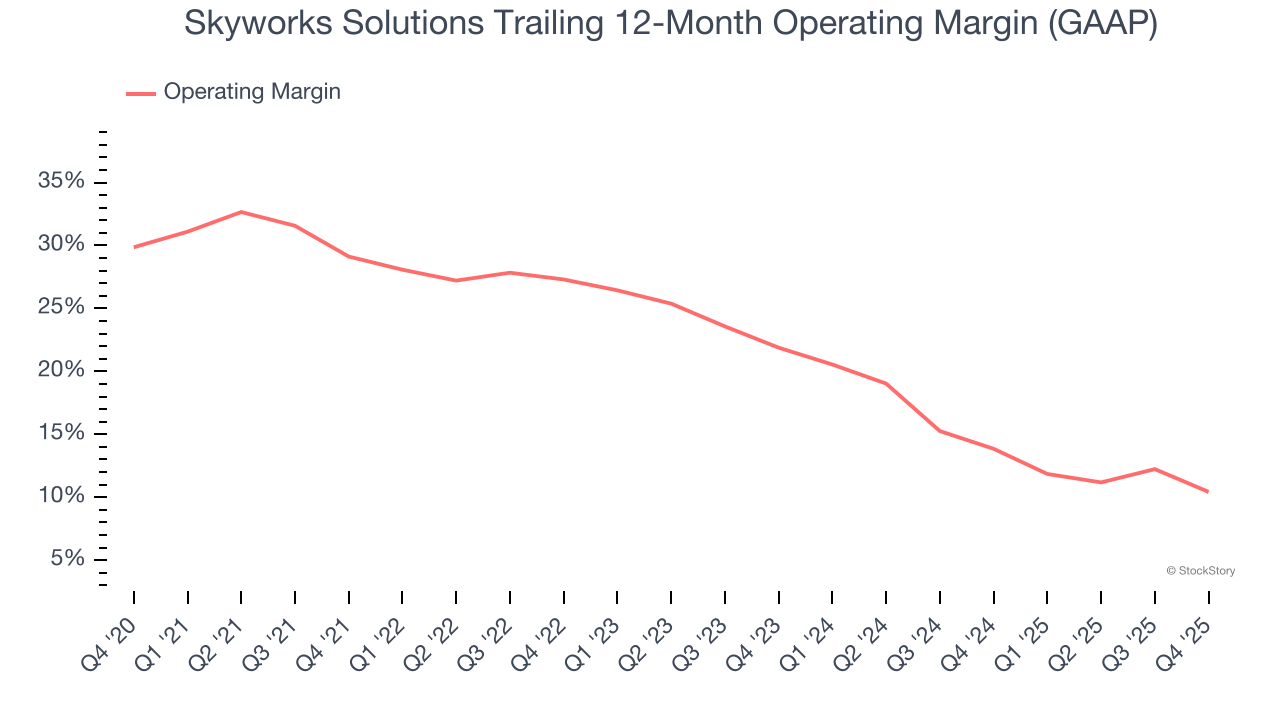

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Looking at the trend in its profitability, Skyworks Solutions’s operating margin decreased by 18.7 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Skyworks Solutions become more profitable in the future. Its operating margin for the trailing 12 months was 10.4%.

Skyworks Solutions doesn’t pass our quality test. After the recent drawdown, the stock trades at 13.2× forward P/E (or $58.60 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-15 | |

| Jul-14 | |

| Jun-29 | |

| Jun-16 | |

| Jun-11 | |

| Jun-10 | |

| Jun-09 | |

| Jun-05 | |

| Jun-02 | |

| May-27 | |

| May-22 | |

| May-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite