|

|

|

|

|||||

|

|

|

TFS Financial has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 5.7% to $14.40 per share while the index has gained 5.7%.

Is now the time to buy TFS Financial, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We don't have much confidence in TFS Financial. Here are three reasons you should be careful with TFSL and a stock we'd rather own.

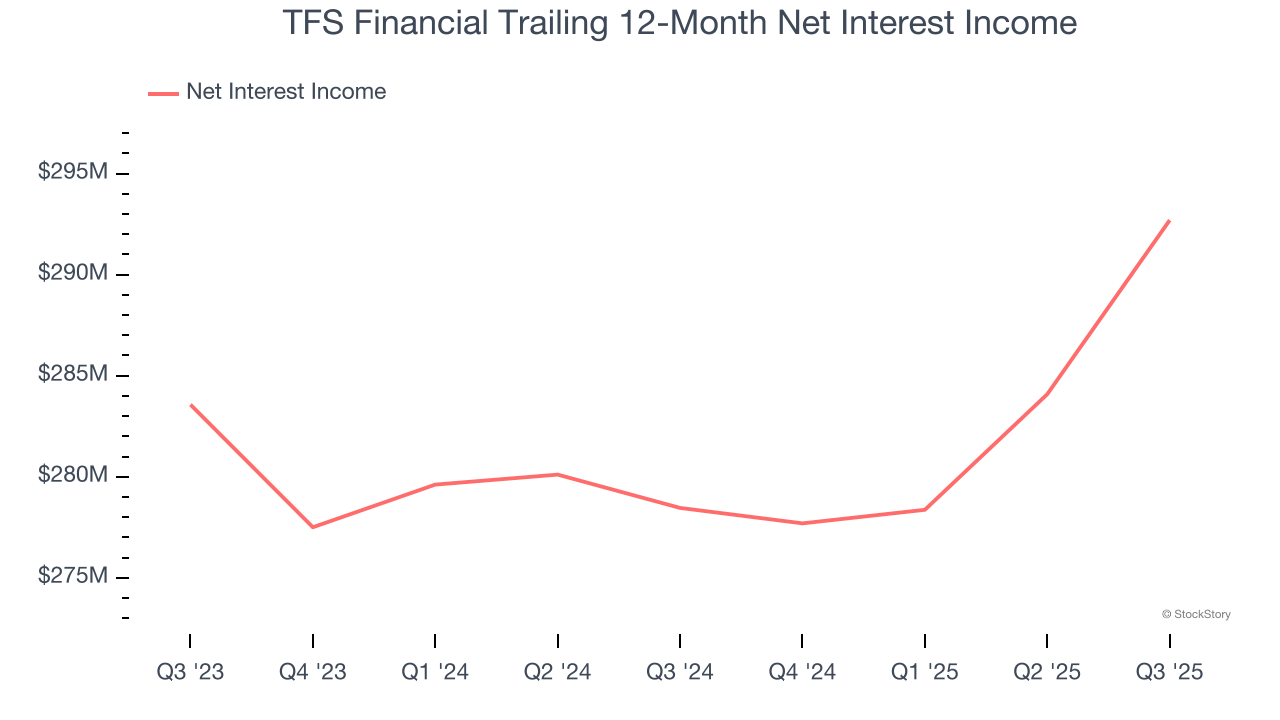

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

TFS Financial’s net interest income has grown at a 3.9% annualized rate over the last five years, much worse than the broader banking industry. This was driven by its loan growth as its net interest margin, which represents how much a bank earns in relation to its outstanding loan book, declined throughout that period.

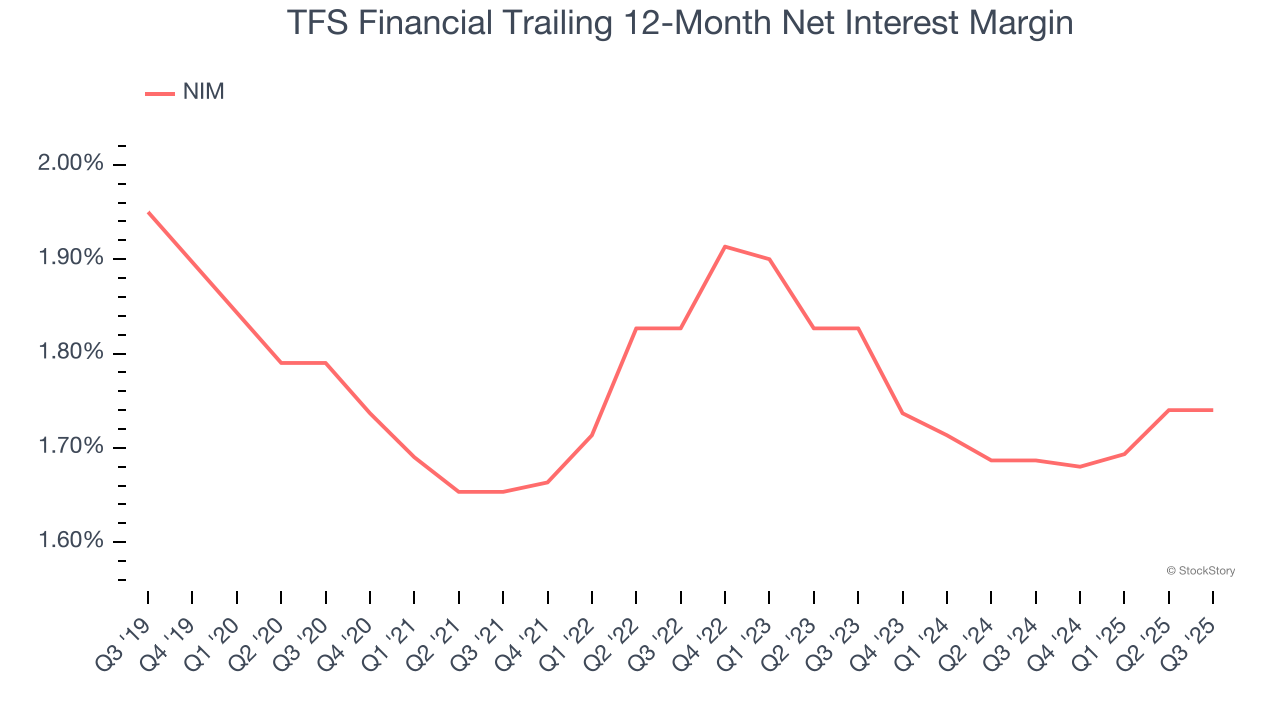

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, we can see that TFS Financial’s net interest margin averaged a poor 1.7%. This metric is well below other banks, signaling its loans aren’t very profitable.

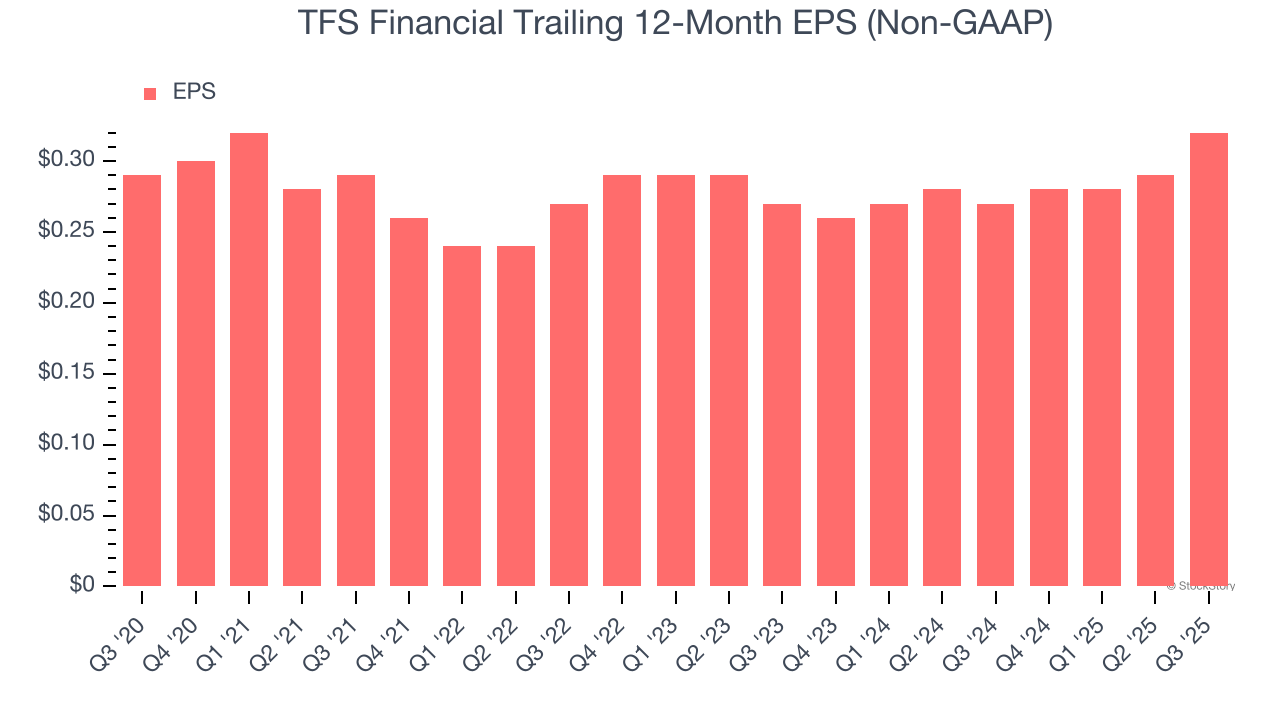

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

TFS Financial’s weak 2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

We cheer for all companies supporting the economy, but in the case of TFS Financial, we’ll be cheering from the sidelines. That said, the stock currently trades at 2.1× forward P/B (or $14.40 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-30 | |

| Jul-30 | |

| Jun-22 | |

| May-28 | |

| May-26 | |

| Apr-30 | |

| Apr-30 | |

| Apr-02 | |

| Mar-25 | |

| Mar-10 | |

| Mar-03 | |

| Feb-26 | |

| Feb-18 | |

| Feb-10 | |

| Jan-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite