|

|

|

|

|||||

|

|

|

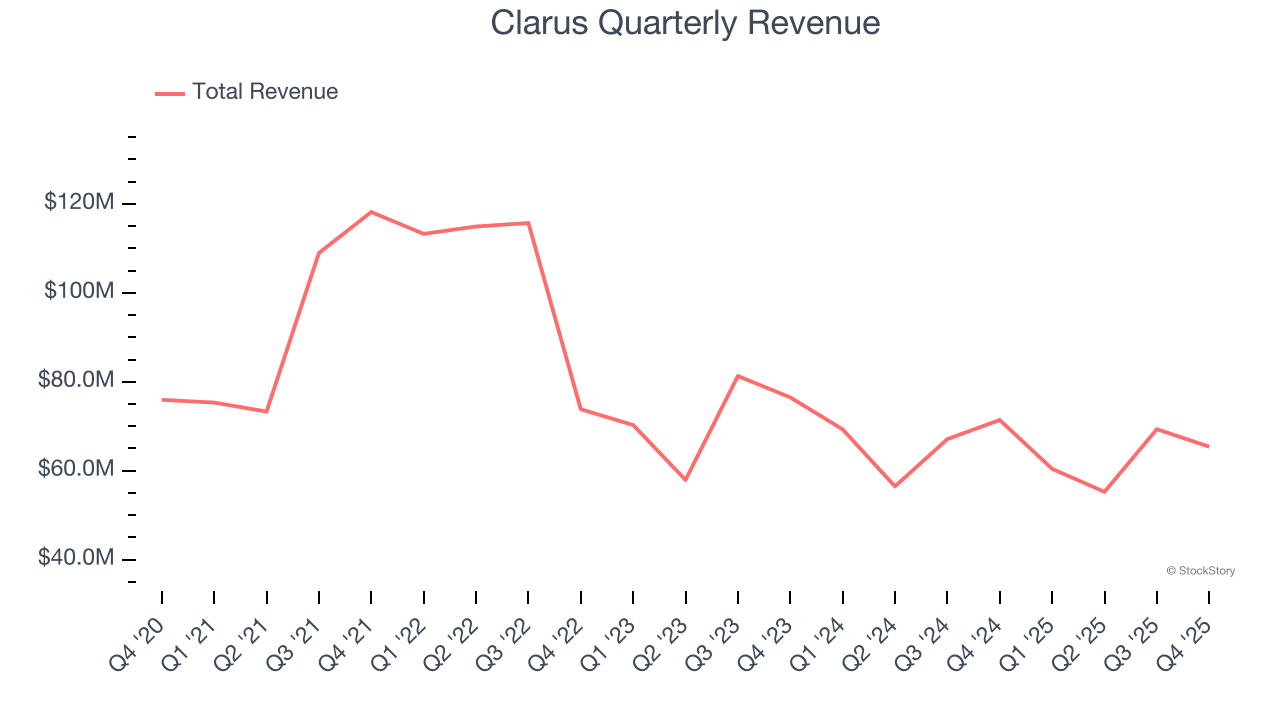

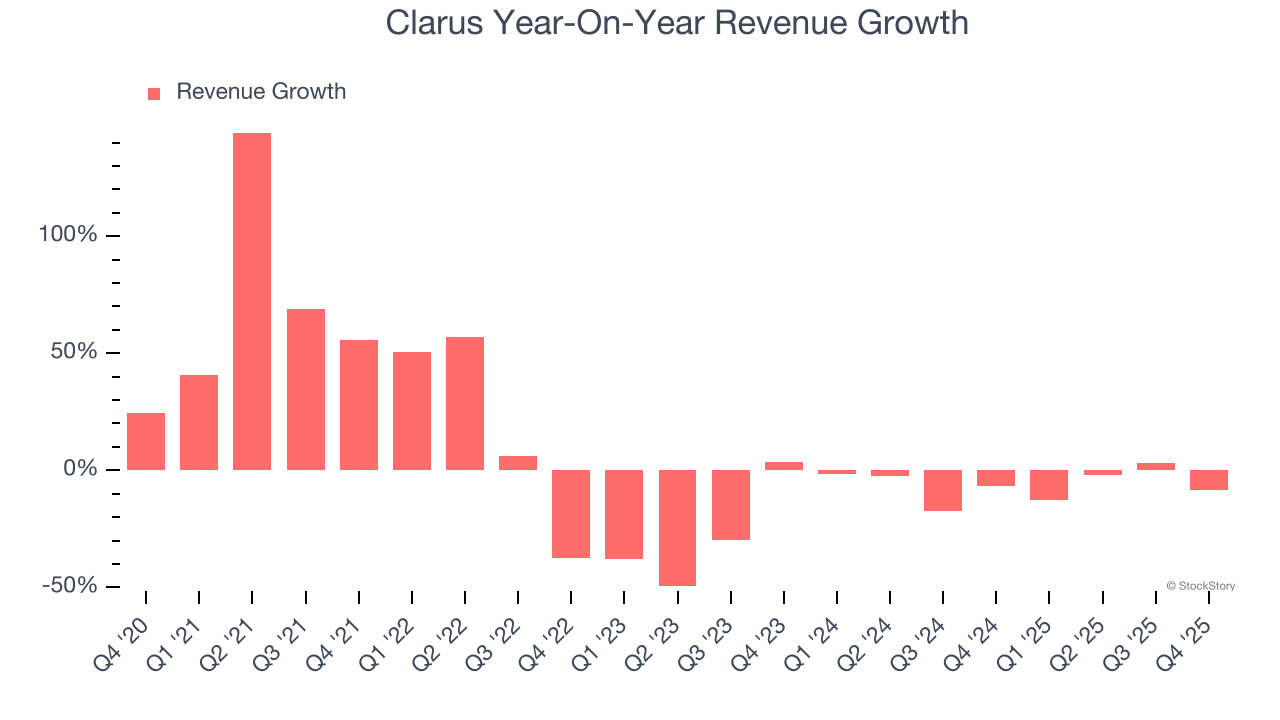

Outdoor lifestyle and equipment company Clarus (NASDAQ:CLAR) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 8.4% year on year to $65.41 million. The company’s full-year revenue guidance of $260 million at the midpoint came in 1.1% below analysts’ estimates. Its non-GAAP profit of $0.09 per share was 38.5% above analysts’ consensus estimates.

Is now the time to buy Clarus? Find out by accessing our full research report, it’s free.

Management Commentary“We took decisive actions in 2025 to sharpen our focus and position Clarus for category-specific growth and greater profitability,” said Warren Kanders, Executive Chairman.

Initially a financial services business, Clarus (NASDAQ:CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Clarus’s 2.3% annualized revenue growth over the last five years was weak. This was below our standards and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Clarus’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.4% annually.

This quarter, Clarus missed Wall Street’s estimates and reported a rather uninspiring 8.4% year-on-year revenue decline, generating $65.41 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

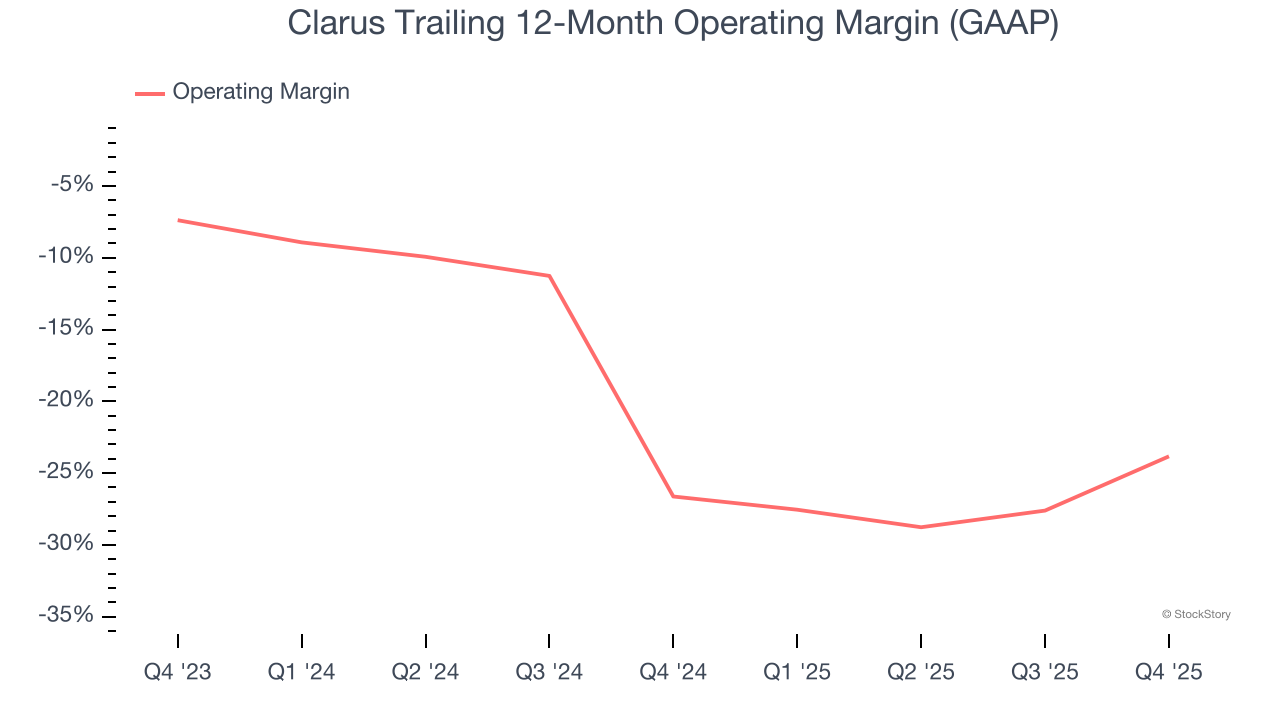

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Clarus’s operating margin has risen over the last 12 months, but it still averaged negative 25.3% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q4, Clarus generated a negative 59.6% operating margin. The company's consistent lack of profits raise a flag.

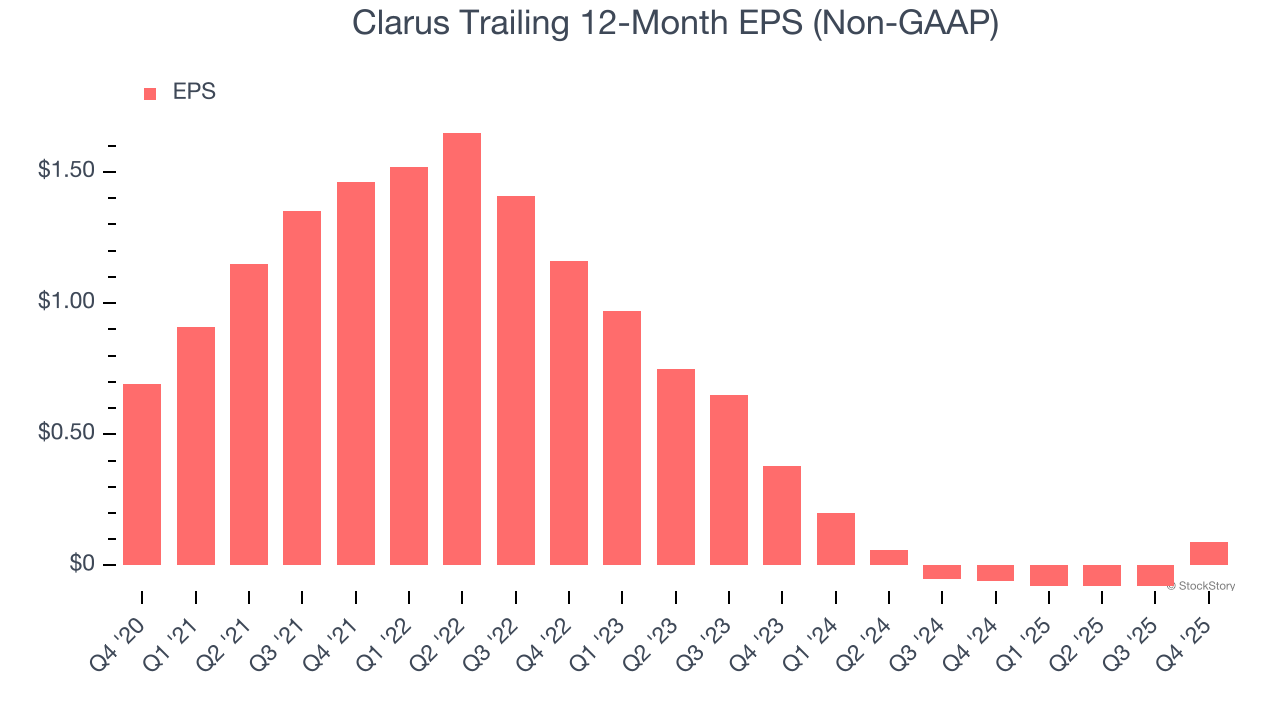

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Clarus, its EPS declined by 33.5% annually over the last five years while its revenue grew by 2.3%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Clarus reported adjusted EPS of $0.09, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Clarus’s full-year EPS of $0.09 to grow 92.6%.

It was good to see Clarus beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.8% to $3.01 immediately following the results.

Clarus’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| May-07 | |

| May-06 | |

| Apr-23 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 | |

| Feb-26 | |

| Feb-05 | |

| Feb-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite