|

|

|

|

|||||

|

|

|

Let’s dig into the relative performance of Surgery Partners (NASDAQ:SGRY) and its peers as we unravel the now-completed Q4 outpatient & specialty care earnings season.

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

The 7 outpatient & specialty care stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 5.8% on average since the latest earnings results.

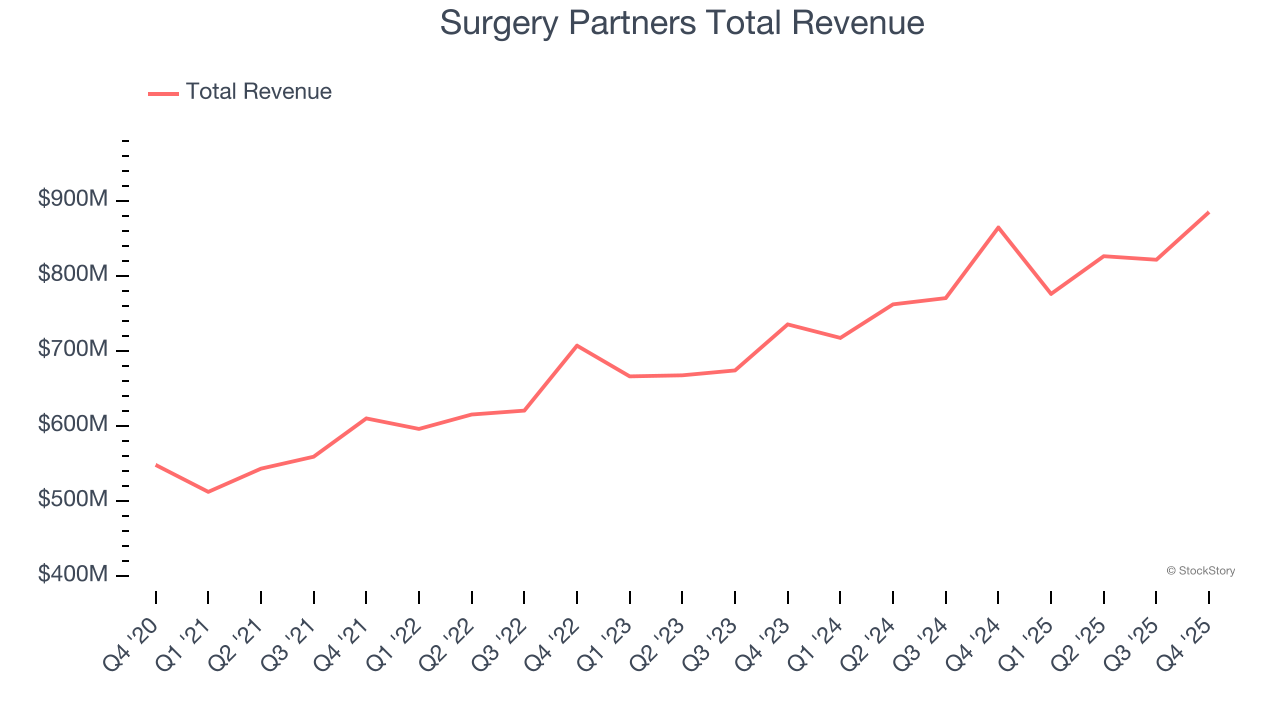

With more than 180 locations across 33 states serving as alternatives to traditional hospital settings, Surgery Partners (NASDAQ:SGRY) operates a national network of outpatient surgical facilities including ambulatory surgery centers and short-stay surgical hospitals.

Surgery Partners reported revenues of $885 million, up 2.4% year on year. This print exceeded analysts’ expectations by 1.9%. Despite the top-line beat, it was still a softer quarter for the company with full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

Eric Evans, Chief Executive Officer, stated, “In 2025, Surgery Partners continued to be guided by an unwavering commitment to high-value and high-quality patient care, with strong performance to start the year giving way to significant and unanticipated headwinds that culminated in fourth quarter results that did not meet our expectations. Despite these challenging headwinds, demand for our services remains strong, and we remain optimistic on the structural tailwinds underpinning long-term ASC market growth. As we progress through 2026, we are proactively strengthening our performance by tightening execution and doubling down on our shift into higher-acuity procedures. We believe the company is well-positioned to capture momentum in the market through multiple initiatives including continued organic growth, strategic M&A and effective portfolio optimization.”

Surgery Partners delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 15.9% since reporting and currently trades at $13.35.

Read our full report on Surgery Partners here, it’s free.

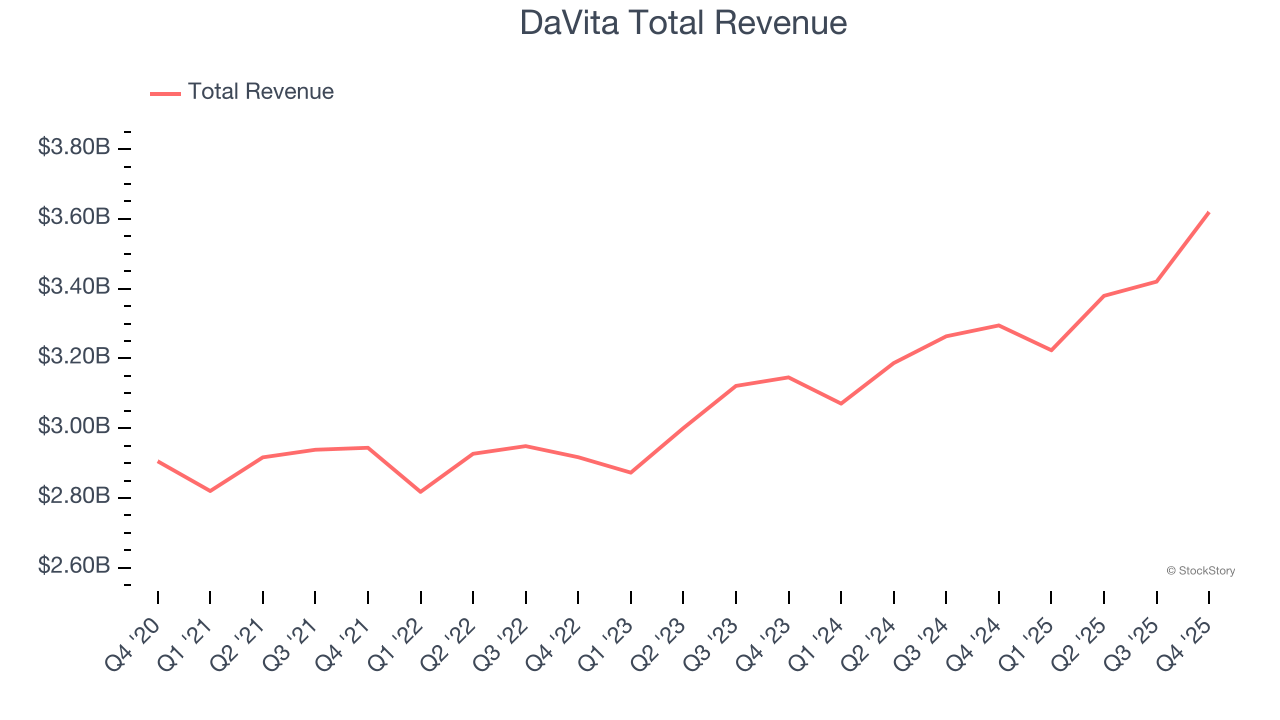

With over 2,600 dialysis centers across the United States and a presence in 13 countries, DaVita (NYSE:DVA) operates a network of dialysis centers providing treatment and care for patients with chronic kidney disease and end-stage kidney disease.

DaVita reported revenues of $3.62 billion, up 9.9% year on year, outperforming analysts’ expectations by 3.2%. The business had a very strong quarter with an impressive beat of analysts’ full-year EPS guidance estimates and a solid beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 35.5% since reporting. It currently trades at $150.65.

Is now the time to buy DaVita? Access our full analysis of the earnings results here, it’s free.

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE:SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

Select Medical reported revenues of $1.40 billion, up 6.4% year on year, exceeding analysts’ expectations by 2.3%. Still, it was a slower quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates and a significant miss of analysts’ EPS estimates.

Interestingly, the stock is up 1.1% since the results and currently trades at $16.25.

Read our full analysis of Select Medical’s results here.

With a network of 161 specialized facilities across 37 states and Puerto Rico, Encompass Health (NYSE:EHC) operates inpatient rehabilitation hospitals that help patients recover from strokes, hip fractures, and other debilitating conditions.

Encompass Health reported revenues of $1.54 billion, up 9.9% year on year. This number was in line with analysts’ expectations. Zooming out, it was a satisfactory quarter as it also logged a solid beat of analysts’ full-year EPS guidance estimates but full-year revenue guidance meeting analysts’ expectations.

Encompass Health had the weakest performance against analyst estimates among its peers. The stock is up 7.3% since reporting and currently trades at $106.82.

Read our full, actionable report on Encompass Health here, it’s free.

With a nationwide footprint spanning 671 clinics across 42 states, U.S. Physical Therapy (NYSE:USPH) operates a network of outpatient physical therapy clinics and provides industrial injury prevention services to employers across the United States.

U.S. Physical Therapy reported revenues of $202.7 million, up 12.3% year on year. This print surpassed analysts’ expectations by 1.7%. More broadly, it was a satisfactory quarter as it also recorded a decent beat of analysts’ revenue estimates but EPS in line with analysts’ estimates.

The stock is flat since reporting and currently trades at $81.08.

Read our full, actionable report on U.S. Physical Therapy here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Jul-24 | |

| Jun-24 | |

| Jun-11 | |

| May-05 | |

| May-05 | |

| Apr-17 | |

| Mar-12 | |

| Mar-10 | |

| Mar-09 | |

| Mar-08 | |

| Mar-04 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite