|

|

|

|

|||||

|

|

|

Over the last six months, Acuity Brands’s shares have sunk to $274.61, producing a disappointing 16.9% loss - a stark contrast to the S&P 500’s 3.1% gain. This might have investors contemplating their next move.

Given the weaker price action, is now an opportune time to buy AYI? Find out in our full research report, it’s free.

One of the pioneers of smart lights, Acuity (NYSE:AYI) designs and manufactures light fixtures and building management systems used in various industries.

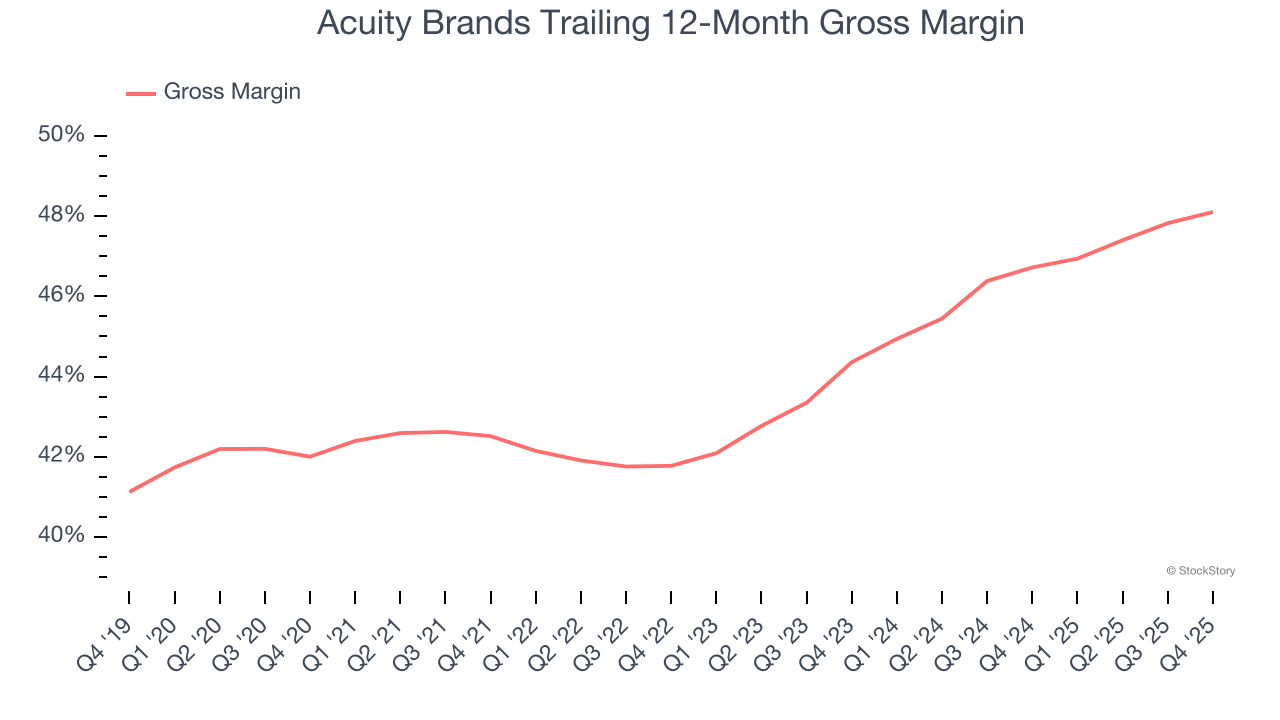

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Acuity Brands has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 44.8% gross margin over the last five years. That means Acuity Brands only paid its suppliers $55.19 for every $100 in revenue.

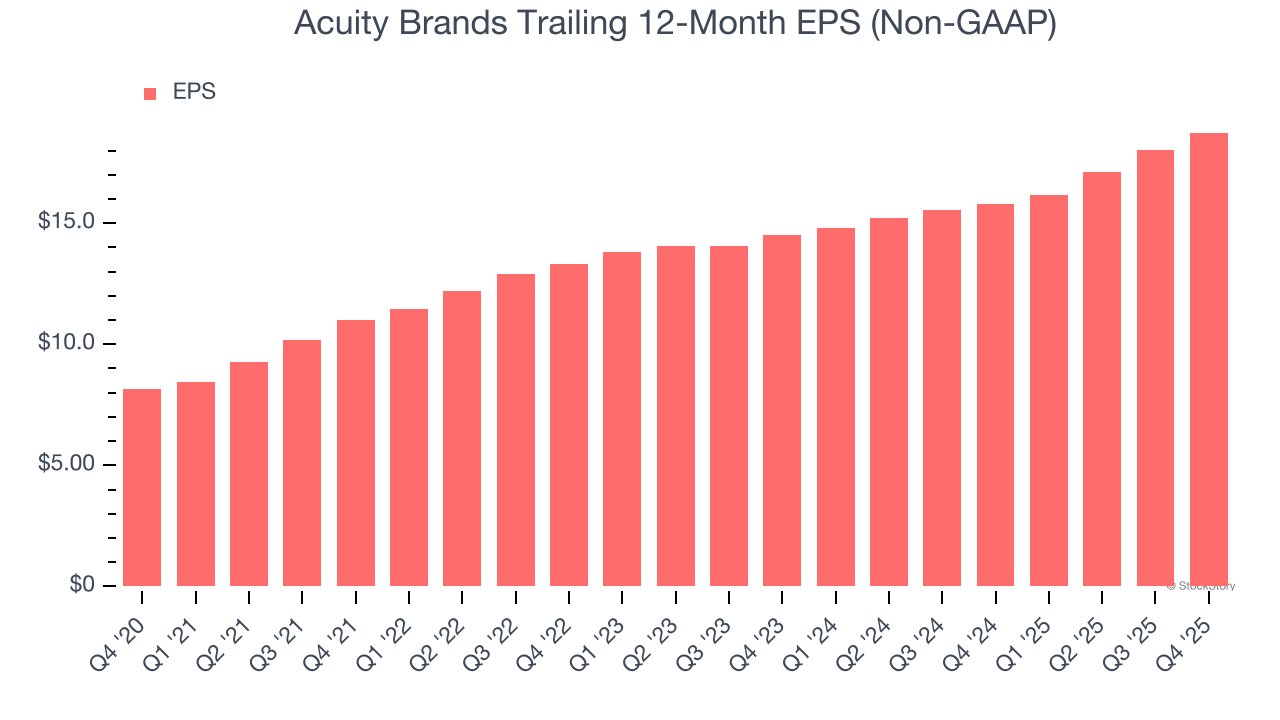

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Acuity Brands’s EPS grew at 18.1% compounded annual growth rate over the last five years, higher than its 6.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

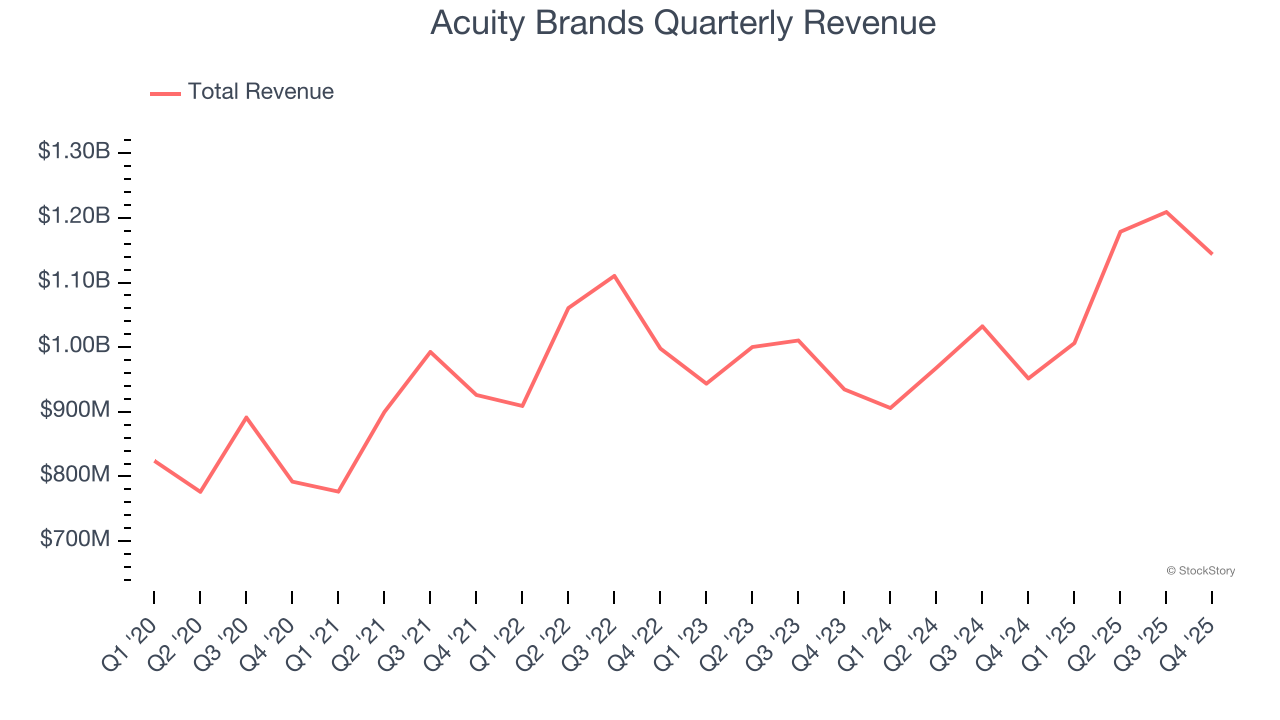

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Acuity Brands grew its sales at a mediocre 6.7% compounded annual growth rate. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Acuity Brands.

Acuity Brands’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 13.7× forward P/E (or $274.61 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| 1 hour | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| May-28 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Mar-26 | |

| Mar-10 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite