|

|

|

|

|||||

|

|

|

Over the past six months, Warby Parker’s shares (currently trading at $24.80) have posted a disappointing 8.2% loss, well below the S&P 500’s 3.1% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for WRBY? Find out in our full research report, it’s free.

Founded in 2010, Warby Parker (NYSE:WRBY) designs, manufactures, and sells eyewear, including prescription glasses, sunglasses, and contact lenses, through its e-commerce platform and physical retail locations.

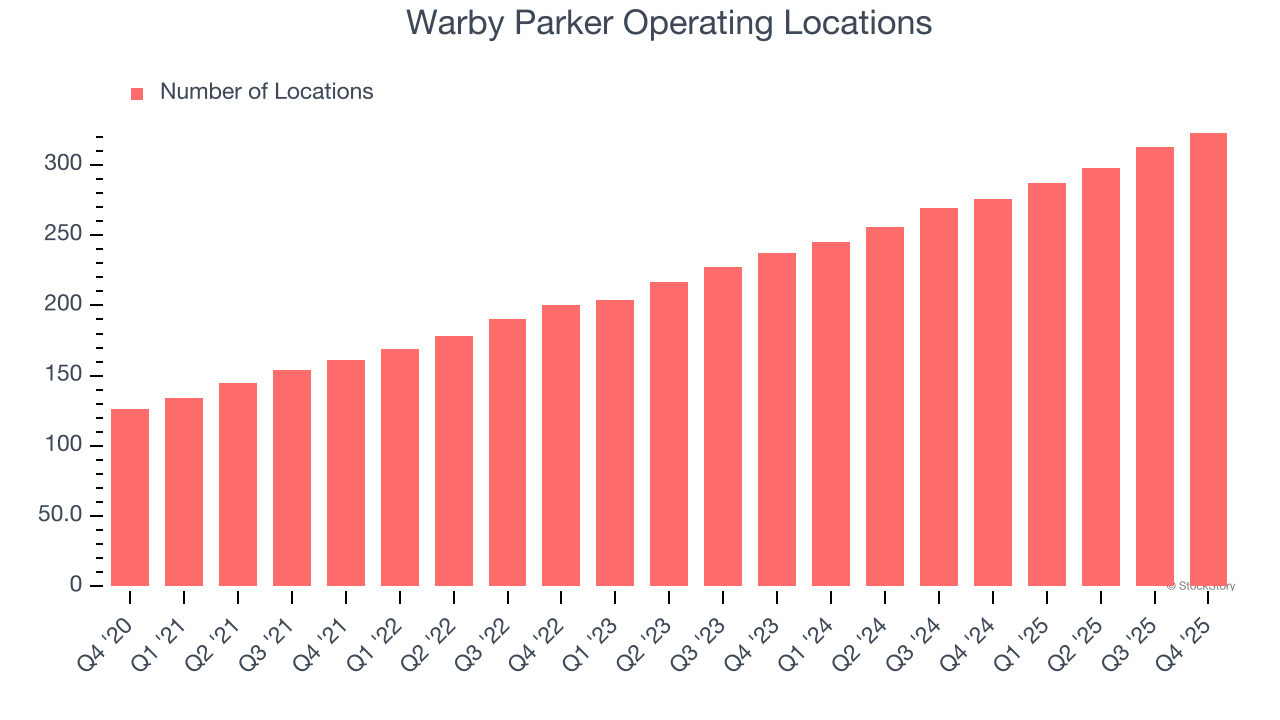

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Warby Parker sported 323 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 17.5% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Warby Parker’s revenue to rise by 12.5%, close to This projection is eye-popping and suggests the market is baking in success for its products.

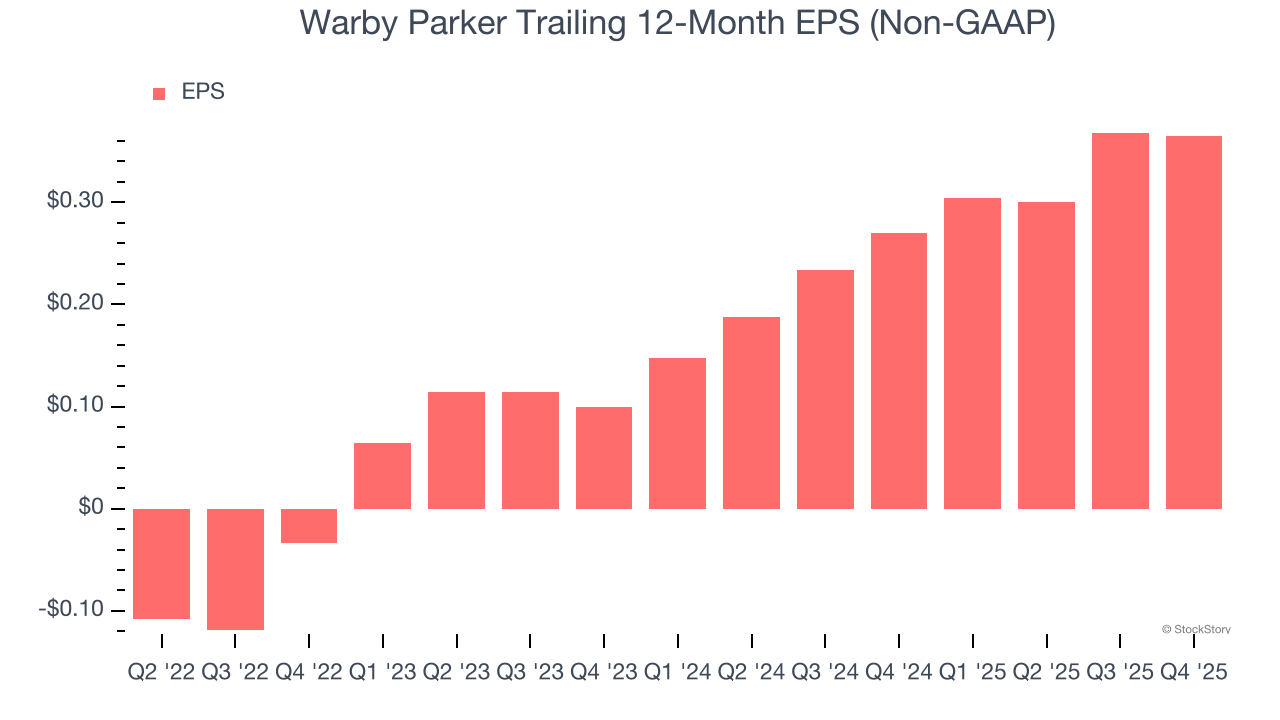

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Warby Parker’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

These are just a few reasons Warby Parker is a high-quality business worth owning. After the recent drawdown, the stock trades at 51.1× forward P/E (or $24.80 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Jul-16 | |

| Jun-29 | |

| Jun-23 |

Meta unveils cheaper AI smart glasses, but the competition is heating up

WRBY -5.00%

Yahoo Finance Video

|

| Jun-05 | |

| May-28 | |

| May-20 | |

| May-19 | |

| May-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite