|

|

|

|

|||||

|

|

|

Biopharmaceutical company Gilead Sciences (NASDAQ:GILD) missed Wall Street’s revenue expectations in Q1 CY2025, with sales flat year on year at $6.67 billion. The company’s full-year revenue guidance of $28.4 billion at the midpoint came in 1.1% below analysts’ estimates. Its non-GAAP profit of $1.81 per share was 2.1% above analysts’ consensus estimates.

Is now the time to buy Gilead Sciences? Find out by accessing our full research report, it’s free.

From its groundbreaking work in developing the first single-tablet regimens for HIV treatment, Gilead Sciences (NASDAQ:GILD) develops and markets innovative medicines for life-threatening diseases including HIV, viral hepatitis, COVID-19, and cancer.

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

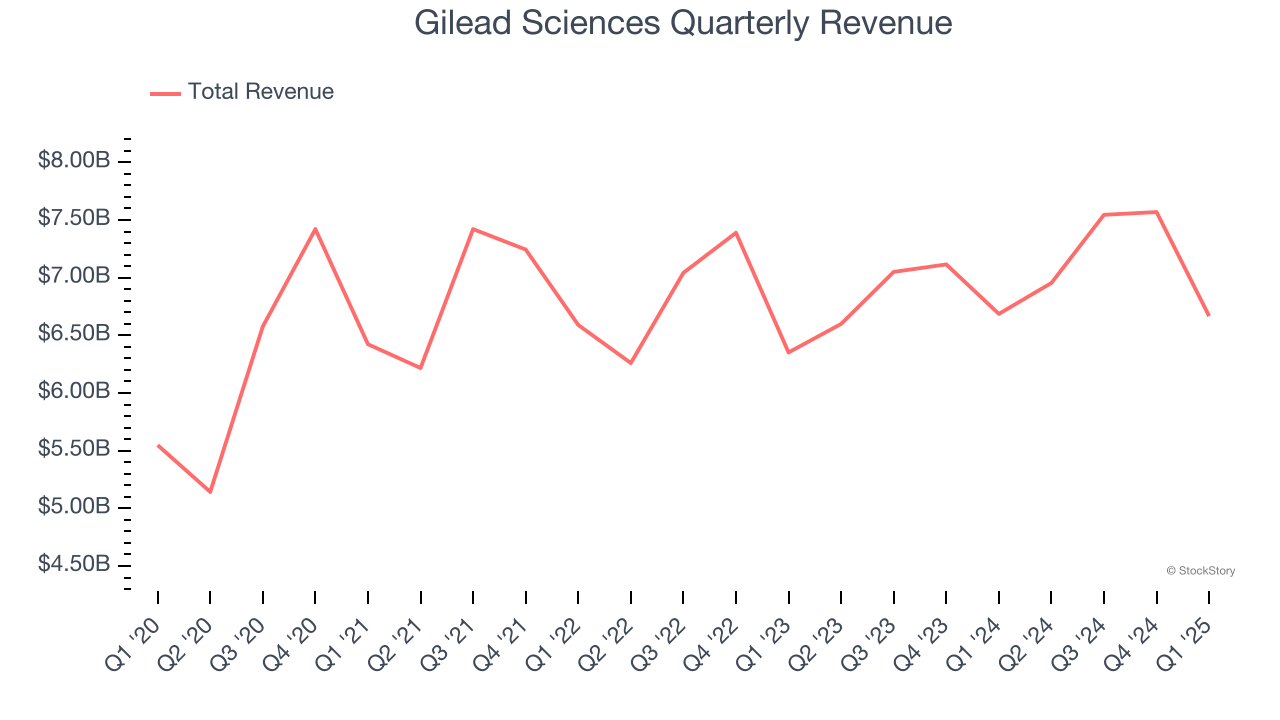

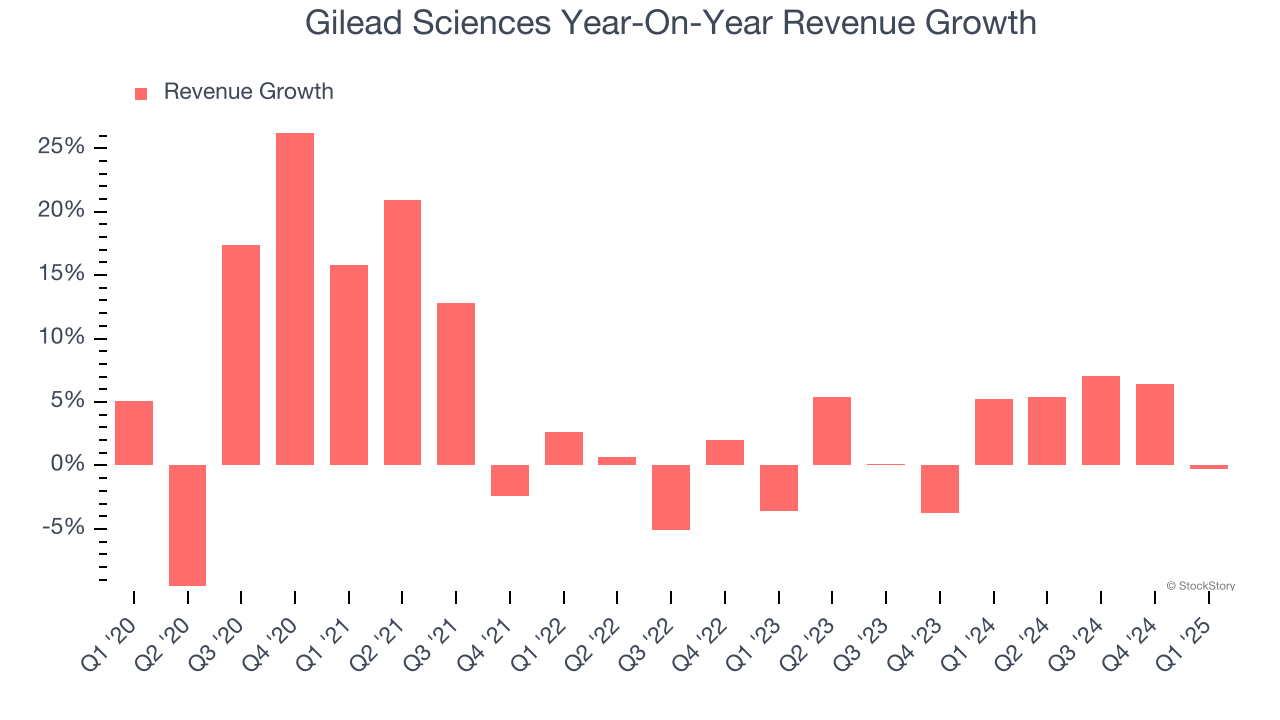

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Gilead Sciences’s 4.8% annualized revenue growth over the last five years was mediocre. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Gilead Sciences’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its most important segment, HIV. Over the last two years, Gilead Sciences’s HIV revenue averaged 1.3% year-on-year growth. This segment has lagged the company’s overall sales.

This quarter, Gilead Sciences missed Wall Street’s estimates and reported a rather uninspiring 0.3% year-on-year revenue decline, generating $6.67 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

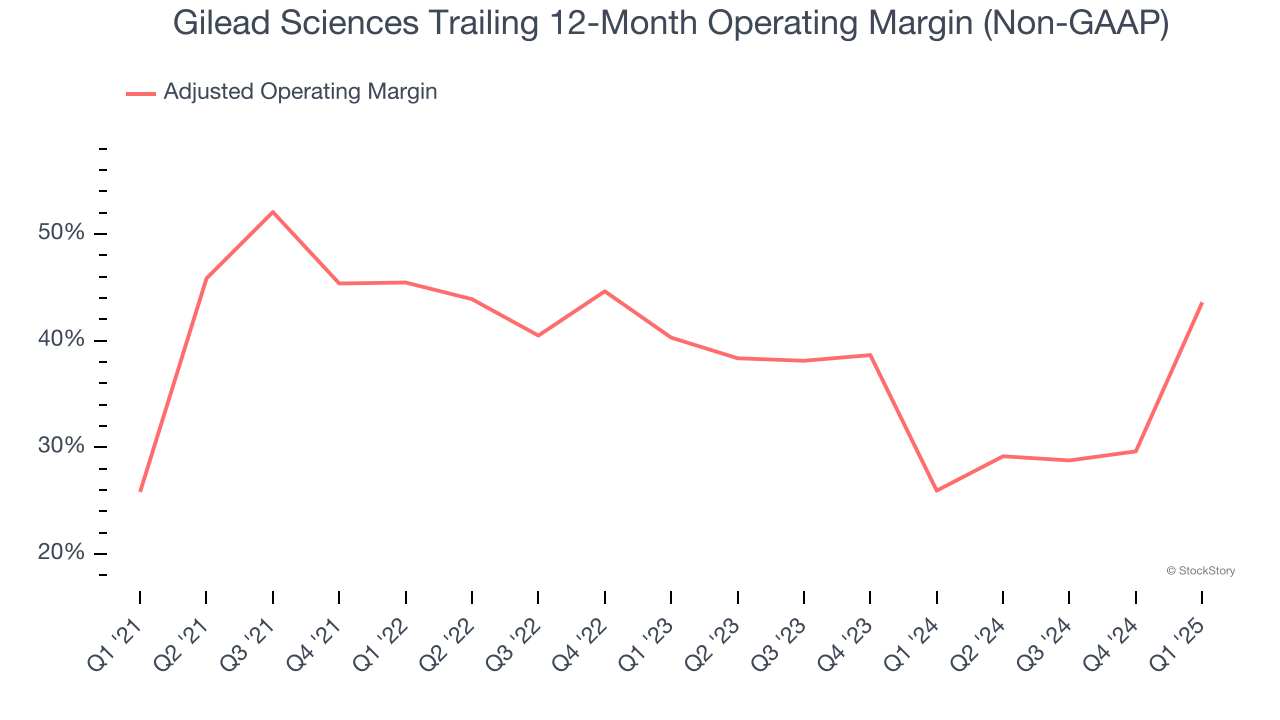

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Gilead Sciences has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 36.4%.

Analyzing the trend in its profitability, Gilead Sciences’s adjusted operating margin rose by 17.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 3.3 percentage points on a two-year basis.

In Q1, Gilead Sciences generated an adjusted operating profit margin of 43.4%, up 60.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

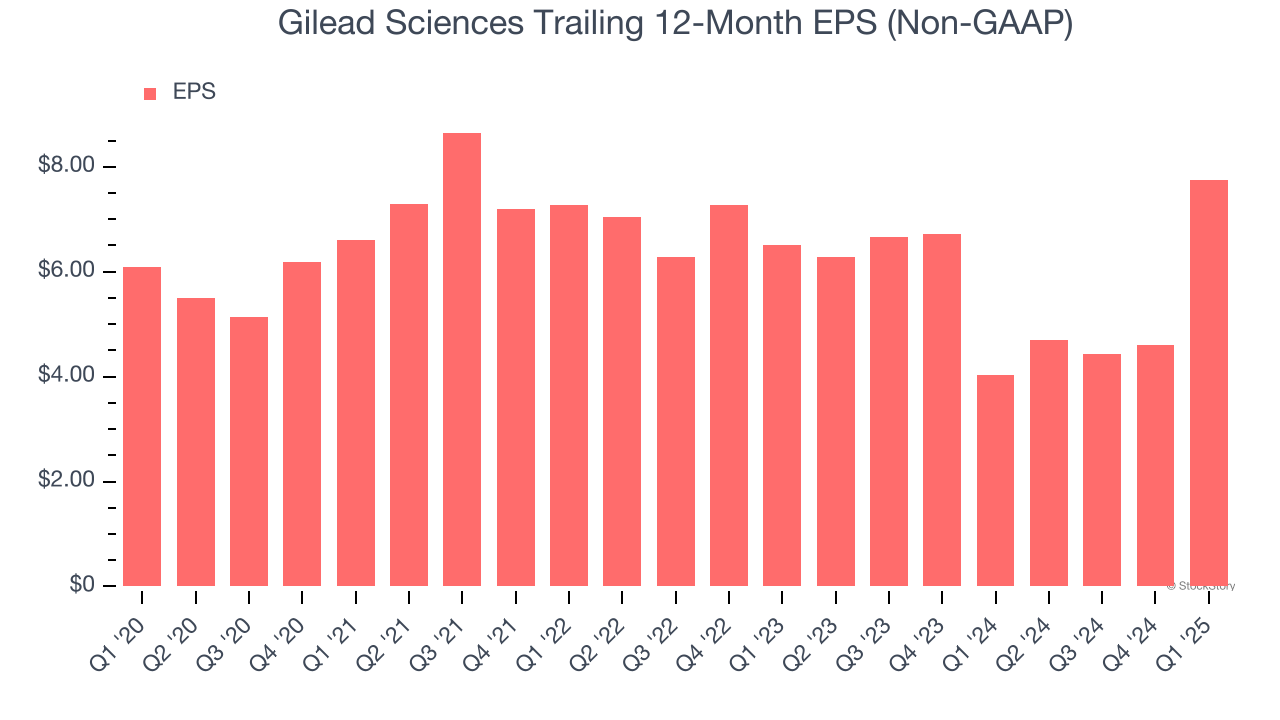

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Gilead Sciences’s unimpressive 4.9% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

In Q1, Gilead Sciences reported EPS at $1.81, up from negative $1.32 in the same quarter last year. This print beat analysts’ estimates by 2.1%. Over the next 12 months, Wall Street expects Gilead Sciences’s full-year EPS of $7.74 to grow 5.9%.

Revenue missed, but EPS beat. Looking ahead, the company's full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this was a mixed quarter with guidance likely weighing on shares. The stock traded down 3.3% to $102.52 immediately after reporting.

Gilead Sciences didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-11 | |

| Feb-11 |

Gilead Bounds Higher As Analysts Debate The Future Of Its Potential HIV Blockbuster

GILD +5.82%

Investor's Business Daily

|

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite