|

|

|

|

|||||

|

|

|

CommScope Holding Company, Inc. COMM and Corning Incorporated GLW are major players in the communication infrastructure industry. CommScope is a premier provider of infrastructure solutions, including wireless and fiber optic solutions, for the core, access and edge layers of communication networks. The company has created a niche market for itself, helping customers scale network capacity, delivering better network response time and performance, and simplifying technology migration.

Corning’s competitive strength lies in its focus on technological prowess. The company is a dominant player in the communication infrastructure space, boasting a major client base of telecom operators, data center operators and cloud providers. With its decades of expertise in material science and optical communication, Corning is aiming to exploit emerging opportunities in the generative AI domain.

With a strong focus on innovation, both CommScope and Corning are steadily advancing their portfolio strength to gain a firmer footing in the highly competitive communication infrastructure market. Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

With around 11,000 patents and patent applications, CommScope holds a dominant position in the industry. Its research and development initiatives are primarily focused on capitalizing high-growth opportunities like fiber optic connectivity for fiber-to-the-x and data centers, Wi-Fi 7 and 6GHz, DOCSIS 4.0, gigabit passive optical network, and metro cell and small cell wireless solutions. With operators moving toward converged or multi-use network structures, combining voice, video and data communications into a single network, CommScope is dedicated to developing solutions designed to support wireline and wireless network convergence, which will be essential for the success of 5G technology. The company recently joined forces with Altice Lab to combine expertise in passive optical networks and drive advancement in Fiber-To-The-Home networks.

To drive greater value to shareholders, the company undertook the CommScope NEXT program, which focuses mainly on three aspects: profitable growth, operational efficiency and portfolio optimization. Management is also taking the initiative to optimize COMM’s portfolio offerings in accordance with shifting market dynamics. The divestiture of the Outdoor Wireless Networks (“OWN”) segment and the Distributed Antenna Systems (DAS) business unit and Home Networks business will likely allow CommScope to increase its focus on core products and strengthen CommScope NEXT initiative.

However, CommScope faces fierce competition in each of its served markets. It has multiple competitors, some of which have substantially greater assets and financial resources. The company also faces competition from several small and medium-sized companies at a regional level. In the Connectivity and Cable Solutions segment, it faces competition from industry giants like Amphenol Corporation APH and Corning. The growing use of AI and machine learning applications is driving demand for Amphenol’s high-speed power and fiber optic interconnect solutions. The rising trade hostilities between the United States and China remain a concern.

There are several secular drivers for Corning’s fiber optic solutions business. Higher usage of mobile devices, proliferation of cloud services, AI applications, and video content are driving the requirements for efficient data transfer and networking systems. Corning’s comprehensive product offerings, comprising optical fiber, hardware, cables and connectors, enable it to create optical solutions to meet evolving customer needs. Specifically, growing adoption of innovative optical connectivity products for generative AI applications is a major growth driver for the Optical Communication segment.

The company recently introduced GlassWorks AI solutions, a comprehensive product suite tailored to support fiber densification with network planning, designing and deployment in AI-native data centers. The portfolio includes customized data center products that enable the expansion of data center capacity without substantial changes in infrastructure, ensuring cost efficiency. It empowers data center operators to accommodate the increasing density of GPU clusters with efficient optical connectivity infrastructure.

However, Corning is plagued by demand softness in some end markets. Its optical communication segment is exposed to the cyclical spending nature of the telecommunications enterprises. Competitive pressure in the communication infrastructure market puts pressure on profitability. Amphenol’s acquisition of CommScope’s OWN and DAS businesses will strengthen its footprint and intensify competition with Corning in fiber-based solutions for mobile networks. Rapid technological shifts in the ever-evolving telecommunication industry are driving research and development expenses and creating a margin squeeze.

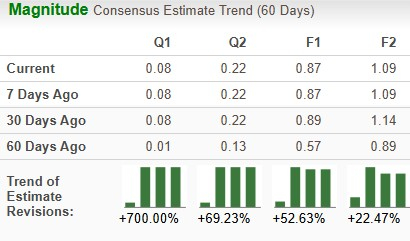

The Zacks Consensus Estimate for CommScope’s 2025 sales implies year-over-year growth of 3.75% while EPS is projected at 87 cents per share against a loss of 3 cents a year ago. The EPS estimates for 2025 have been trending northward over the past 60 days.

The Zacks Consensus Estimate for Corning’s 2025 sales imply year-over-year growth of 4.93%, while that of EPS is projected at $2.33 per share compared to $1.96 cents per share a year ago. The EPS estimates for 2025 have remained unchanged over the past 60 days.

Over the past year, CommScope has gained 303.9% compared with the industry’s growth of 34%. Corning has gained 40.2% over the same period.

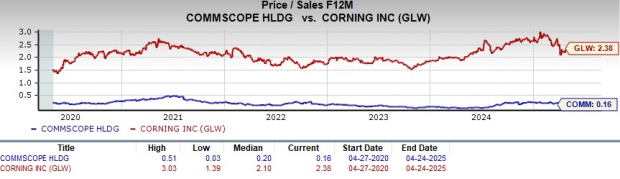

CommScope looks more attractive than Corning from a valuation standpoint. Going by the price/sales ratio, CommScope’s shares currently trade at 0.16 forward sales, significantly lower than Corning’s 2.38.

CommScope sports a Zacks Rank #1 (Strong Buy), while Corning has a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Both organizations are expecting to improve their revenues and profits in 2025. Although CommScope has been facing a bumpy road in recent years, its effort to strengthen its capital structure and optimize its portfolio to better address market trends is expected to give it a competitive edge in the upcoming quarters. Corning’s comprehensive portfolio offers better stability and resilience in a volatile market. However, with a superior Zacks Rank, better price performance, and attractive valuation metrics, CommScope appears to be a better investment option at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 5 hours | |

| 5 hours | |

| 9 hours | |

| Feb-17 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite